![]()

For Immediate Release

Media Contact: Dan Knight

202-777-3544

USMI Statement on FHA’s Annual Report to Congress

WASHINGTON — Today, the Federal Housing Administration (FHA) released its “Annual Report to Congress Regarding the Financial Status of the Mutual Mortgage Insurance Fund (MMIF) Fiscal Year 2016.” The following statement can be attributed to Lindsey Johnson, USMI President and Executive Director:

“Consistent with improvement in the overall mortgage credit market, we welcome the news that FHA’s single-family forward program and the home equity conversion mortgage (HECM) program are combined above the statutory required 2 percent capital ratio. Now that FHA’s single-family fund has climbed its way back, this moment presents an opportunity for the new Administration and lawmakers to consider a coordinated housing policy to ensure broad access to low downpayment lending while reducing the government’s footprint in housing and protecting taxpayers.

“FHA serves an important countercyclical role in the mortgage finance system. Following the financial crisis, FHA’s insured market share grew nearly 300 percent from its pre-crisis market and remains at elevated levels today — and it has taken nearly a decade for the MMIF to recover from serving this countercyclical role. Now that FHA is back to meeting the 2 percent ratio requirement, there is also an opportunity to focus on strengthening FHA’s capital standard, which is dramatically less than what is required of FHA’s private market counterparts, to make the agency more financially resilient going forward. Changes in market conditions, or changes in the very volatile HECM program, could easily push the FHA back into the red.

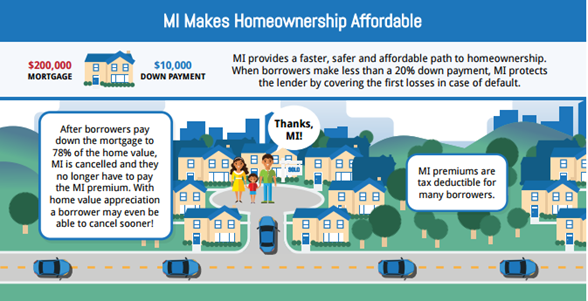

“Further, this is also the time to refocus the FHA back to its core mission. Fortunately, today there is a healthy low downpayment GSE mortgage market — backed by private mortgage insurance — available to borrowers so FHA no longer needs to play an oversized role in our housing market. Private mortgage insurers put their own capital at risk to mitigate mortgage credit risk, provided over $50 billion in credit risk protection since the financial crisis to the GSEs, and did not take any taxpayer bailout. And this market has been strengthened since the financial crisis as all MIs have all implemented significant new capital requirements, or the Private Mortgage Insurer Eligibility Requirements (PMIERs), which are stress-tested financial and capital requirements established by Fannie Mae, Freddie Mac and the Federal Housing Finance Agency, enhancing MI’s ability to assume mortgage credit risk in the future.

“The MI industry and FHA should serve complementary roles to promote broad and sustainable homeownership. To accomplish this, FHA needs to not only become more financially resilient, in line with the rest of the financial system, but also remain focused on its core mission of serving underserved communities. USMI stands ready to work with the new Administration and Congress to enhance a mortgage finance system that meets the needs of low downpayment borrowers while protecting taxpayers.”

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

{kind=link}