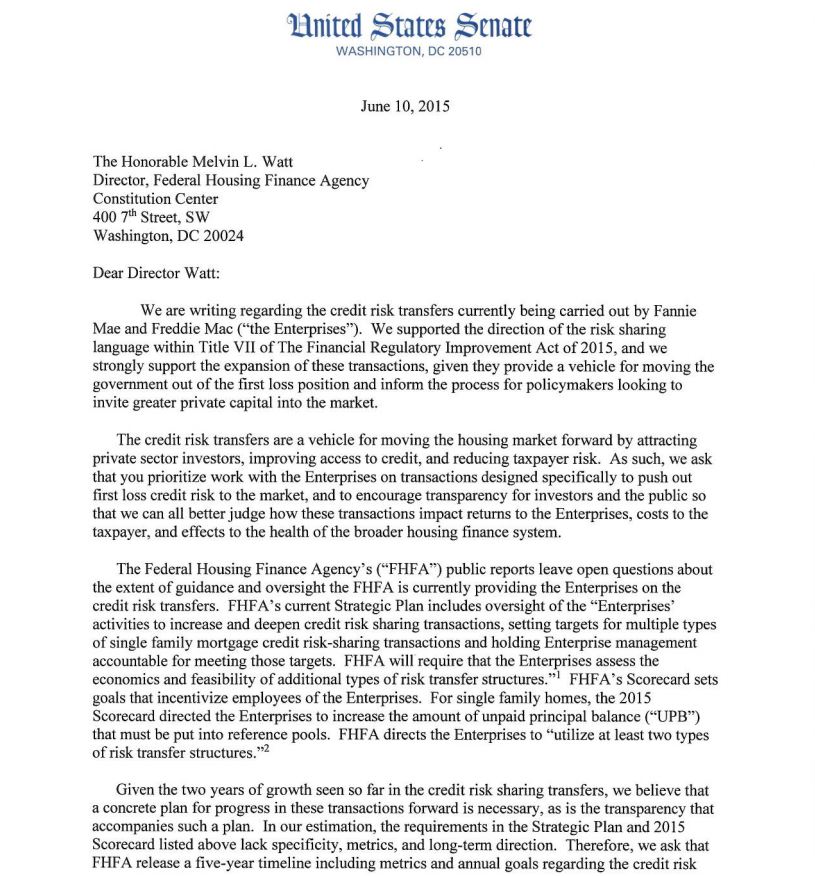

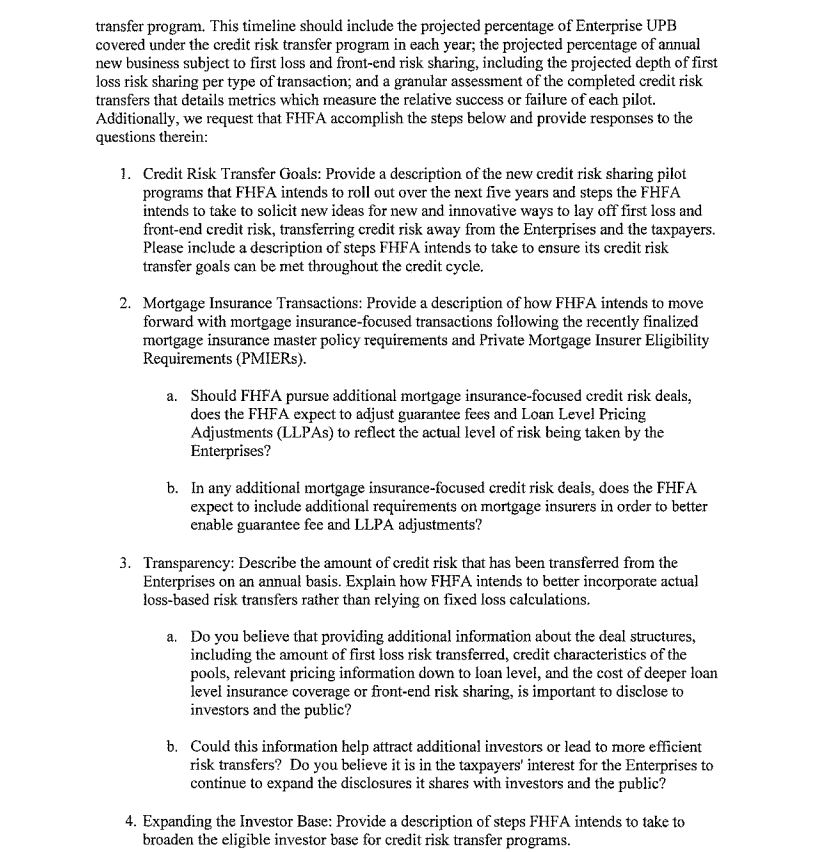

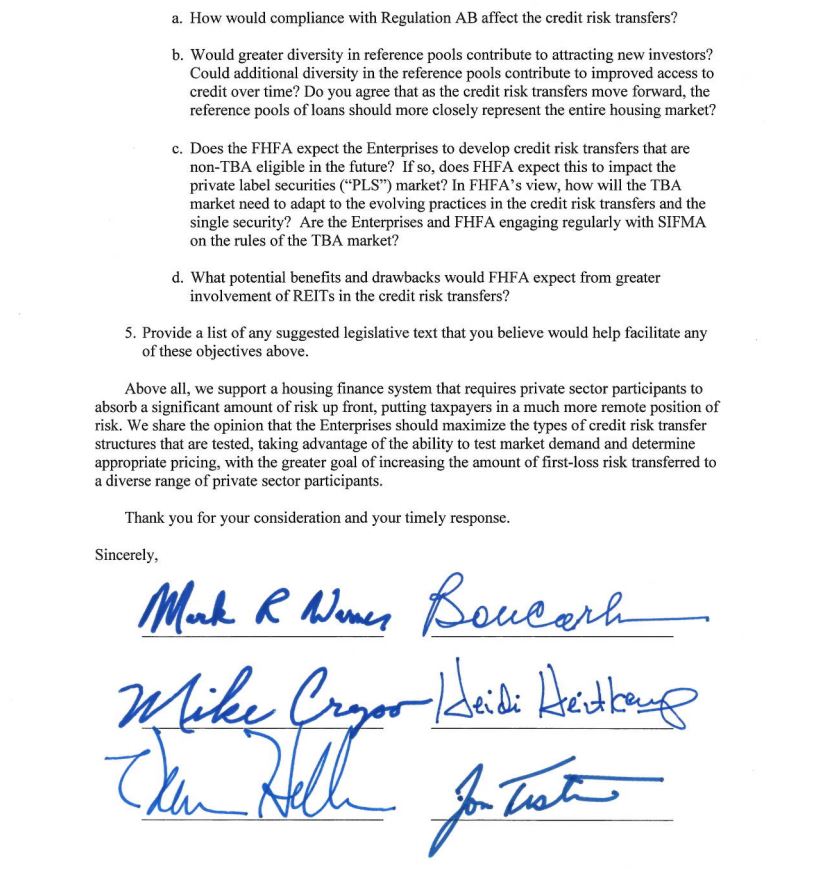

(June 10, 2015) A group of Senate Banking Committee members sent a letter today to FHFA urging them to expand and better define the development of the credit risk transfer programs at the GSEs.

The letter and press release can be found here.

(June 10, 2015) A group of Senate Banking Committee members sent a letter today to FHFA urging them to expand and better define the development of the credit risk transfer programs at the GSEs.

The letter and press release can be found here.

USMI delivered the following letter to members of the Senate Banking Committee last night:

The Honorable Richard Shelby

Chairman

U.S. Senate Committee on Banking, Housing, and Urban Affairs

534 Dirksen Senate Office Building

Washington, DC 20510

Dear Chairman Shelby:

U.S. Mortgage Insurers (“USMI”) welcomes the effort to make progress on increasing the reliance on private capital in housing finance as part of consideration by the Senate Banking Committee of the Financial Regulatory Improvement Act of 2015.

Specifically, USMI supports Section 706, which calls on the Government Sponsored Enterprises (“GSEs”) to engage in front-end risk sharing transactions. This directive would make greater use of private capital to “de-risk” the GSEs, lower the exposure and costs for the enterprises and taxpayers and should lower costs to borrowers. USMI supports this effort, and will continue to work with the Committee during the legislative process on clarifications to ensure the legislation has the intended effect of being “transaction neutral” to permit a variety of methods of up front risk sharing, with all risk sharing counterparties held to equivalent standards.

Promotion of greater up front risk sharing will help build a strong, stable housing finance system that provides access to sustainable and affordable mortgage credit while protecting taxpayers. We look forward to favorable action on this important effort.

Sincerely,

U.S. Mortgage Insurers

cc: The Honorable Sherrod Brown, Ranking Member

All members of the Senate Banking Committee

![]()

For Immediate Release

April 17, 2015

Media Contacts

Robert Schwartz 202-207-3665 (rschwartz@prismpublicaffairs.com)

Michael Timberlake 202-207-3637 (mtimberlake@prismpublicaffairs.com)

USMI Statement on Final Mortgage Insurer Eligibility Requirements (PMIERs)

Today, the Federal Housing Finance Administration (FHFA) published final revised Private Mortgage Insurer Eligibility Requirements (“PMIERs”), which set the requirements that private Mortgage Insurers (MIs) must meet to be eligible to insure loans acquired by Fannie Mae and Freddie Mac (the “GSEs”). The PMIERs include new risk-based financial requirements for MIs. USMI appreciates the efforts of FHFA and the GSEs to work with all interested parties to finalize the updates to the PMIERs.

USMI member companies are united in support of this important effort, and are committed to fully comply with PMIERs. Finalizing the PMIERs is an important milestone for the MI industry. Lenders, investors and other mortgage market participants can now have even more confidence in the value and financial strength of MI. USMI member companies encourage FHFA to apply these standards to all providers of credit enhancement to the GSEs to ensure our housing system remains strong and stable.

With PMIERs finalized, the industry is positioned to be in the forefront of efforts to meet the important goal of putting more private capital at risk ahead of taxpayers, including by providing upfront risk sharing and deeper MI coverage for the GSEs. USMI member companies stand ready to work with the GSEs, lenders and regulators on improving access to credit and homeownership for consumers.

The MI industry has recapitalized, attracted new entrants, and finalized new master policies that provide greater clarity and transparency regarding when and how MIs pay claims. Since the GSEs entered conservatorship, MI has covered over $44 billion in claims to the GSEs alone, resulting in a substantial savings to taxpayers.

USMI members are also continuing to work closely with the National Association of Insurance Commissioners’ Mortgage Guaranty Insurance Working Group as it updates the Mortgage Guaranty Insurance Model Act (“Model Act”) to update state regulation of MI. USMI members are committed to sound prudential regulation and requirements that work in a complementary manner to enable a stable and well-functioning housing finance market.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

![]()

For Immediate Release

March 31, 2015

Media Contacts

Robert Schwartz 202-207-3665 (rschwartz@prismpublicaffairs.com)

Michael Timberlake 202-207-3637 (mtimberlake@prismpublicaffairs.com)

USMI Responds to Basel Committee Credit Risk Proposal

U.S. Mortgage Insurers (USMI) submitted a response to the Basel Committee on Banking Supervision’s proposal, Revisions to the Standardised Approach for credit risk, which would, among other things, revise the calculation of banks’ risk weights for exposures secured by residential real estate under the Standardized Approach for calculating credit risk under the Basel capital framework.

USMI raised two primary areas of concern with the proposal: it does not appear to recognize the risk-reducing effect of private mortgage insurance in the calculation of residential mortgage risk weights, nor does it appear to recognize the risk-increasing effect of simultaneous second lien mortgages on primary residential mortgage exposures.

To address these concerns, USMI urged the Basel Committee to recognize the risk-reducing effect of mortgage insurance in the calculation of residential mortgage risk weights, pointing out several key benefits of mortgage insurance:

Additionally, USMI urged the Committee to use a combined loan-to-value ratio that gives effect to simultaneous second liens for residential mortgage risk weighting, rather than the first lien loan-to-value ratio. As written, the proposal ignores the significant risks inherent in loans with junior second liens originated at the same time on the same residence as the primary mortgage, also known as “simultaneous seconds” readily observed during the financial crisis.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

The recent decision by the Federal Housing Administration (FHA) to lower annual mortgage insurance premiums has renewed the debate about the complementary roles of private Mortgage Insurance (MI) and the FHA government mortgage insurance program.

Below are links to background materials on this topic and excerpts from a related hearing before the House Financial Services Committee Housing and Insurance Subcommittee, which included testimony by Rohit Gupta, President and CEO of Genworth Mortgage Insurance and Chair of U.S. Mortgage Insurers (USMI) and other housing finance experts.

![]()

For Immediate Release

February 26, 2015

Media Contacts

Robert Schwartz 202-207-3665 (rschwartz@prismpublicaffairs.com)

Michael Timberlake 202-207-3637 (mtimberlake@prismpublicaffairs.com)

USMI Testifies on the Roles of Private MI and FHA, the Need to Strike the Right Balance for Taxpayers

Rohit Gupta, President and CEO of Genworth Mortgage Insurance and Chair of U.S. Mortgage Insurers (USMI), testified before the House Financial Services Committee Housing and Insurance Subcommittee today on behalf of the private Mortgage Insurance (MI) industry. The hearing, “The Future of Housing in America: Oversight of the Federal Housing Administration, Part II” followed a February 11 hearing featuring Housing and Urban Development Secretary Julian Castro on the condition of the Federal Housing Administration (FHA) Mutual Mortgage Insurance Fund (MMIF).

Gupta’s testimony focused on the recent decision to lower annual mortgage insurance premiums at FHA, which has generated much debate on the relative roles of government and private capital in supporting homeownership while also protecting taxpayers. Potential homeowners without the ability to make a 20 percent down payment currently have two options for the mortgage insurance necessary to obtain a mortgage: either from the government-backed FHA program, or from private mortgage insurance (MI). Gupta pointed out that while these options may sound similar, from a public policy perspective, they are quite different, especially when it comes to the impact on taxpayers.

Key differences are:

“FHA and private MIs can and should serve as complementary forces that enable the FHA to remain focused on its fundamental mission of serving underserved markets,” said Gupta. “But for this model to work properly, it is critically important that the FHA not stray too far afield from that mission.”

“The recent decision to lower annual mortgage insurance premiums at FHA…has two immediate consequences: (1) it slows the trajectory of FHA attaining the 2% minimum capital requirement; and, (2) it limits the…return of private capital to support U.S. housing finance,” Gupta continued.

A copy of Gupta’s testimony submitted to the Committee is available here which includes a sideby-side comparison of the protections for taxpayers from MI vs. FHA.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

![]()

For Immediate Release

February 24, 2015

Media Contacts

Robert Schwartz 202-207-3665 (rschwartz@prismpublicaffairs.com)

Michael Timberlake 202-207-3637 (mtimberlake@prismpublicaffairs.com)

USMI Announces Executive Leadership Changes

USMI announced today changes in the trade association’s executive leadership. USMI Co-Chair Adolfo Marzol, Executive Vice President of Essent Guaranty, will be retiring at the end of March. Rohit Gupta, President and CEO of Genworth Mortgage Insurance, who served as Co-Chair with Marzol since the formation of USMI, will become the Chair of USMI.

“Adolfo was an essential figure in the formation and launch of USMI last year,” said Gupta. “He brought a tremendous wealth of experience and expertise to the industry and his many contributions will certainly extend beyond his tenure.”

“I am honored to have been part of forming USMI,” said Marzol. “This is a critical time for mortgage finance, and I am gratified at the growing understanding of the vital role MI plays to protect taxpayers, increase access for borrowers, and work with lenders of all sizes. I’m confident that the MI industry is well-positioned for the future under the leadership of USMI.”

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

![]()

For Immediate Release

January 8, 2015

Media Contacts

Robert Schwartz 202-207-3665 (rschwartz@prismpublicaffairs.com)

Michael Timberlake 202-207-3637 (mtimberlake@prismpublicaffairs.com)

USMI Statement on FHA Fee Reduction Announcement

“Last November, FHA released updated information on the status of the FHA insurance fund. While progress was made in restoring the financial health of the fund, it fell well short of its 2% capital ratio mandate. In light of that report, USMI urged policy makers to proceed cautiously and to carefully assess the impact of any potential FHA premium reductions on its solvency as well as its stated objective of returning the FHA to a smaller and more traditional share of the mortgage market.

USMI member companies urge Congress, FHA, and regulators to work together to further expand sustainable access to credit while increasing reliance on private capital. Mortgage insurers putting their own capital at risk should be preferred to government risk taking, consistent with the principles put forward by the Administration for housing reform. The MI industry has the capacity and capability to further reduce taxpayer risk and lower costs for many home buyers while expanding access to mortgage credit.”

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

![]()

For Immediate Release

December 17, 2014

Media Contacts

Robert Schwartz 202-207-3665 (rschwartz@prismpublicaffairs.com)

Michael Timberlake 202-207-3637 (mtimberlake@prismpublicaffairs.com)

USMI Commends Passage of Homeowner Tax Relief

“USMI commends passage by Congress last night of a one year extension of vital homeowner tax relief. We are especially pleased that the legislation includes the tax-deductible treatment of mortgage insurance premiums for low and moderate income borrowers. We look forward to working with Congress towards permanent enactment of this important tax relief for homeowners.”

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

USMI Co-Chairs Rohit Gupta and Adolfo Marzol had their op-ed published in The Hill last week on December 3.