Congress is back from recess, Pumpkin Spice lattes are back on the menu, and housing finance reform is back at the top of news headlines in Washington this fall. In September, the Trump Administration released plans to reform the nation’s housing finance system. USMI issued a statement applauding the initiative and calling for Congress to address the GSEs’ underlying structural challenges and promote a coordinated federal housing policy. The Senate Banking Committee also held a hearing on the matter to learn more about the Administration’s Plans. The same week that the Administration released its Plans, the Fifth Circuit ruled in favor of GSE shareholders in their lawsuit against the U.S. Treasury, as the court allowed the shareholders to reinstate claims alleging that FHFA is unconstitutionally structured. While the fate of the legal challenges is still unclear, what is clear is that FHFA is moving ahead on many of its plans to review and make changes to the current programs and activities of the GSEs. Last week, FHFA announced an increase to the caps on the amount of multifamily loans the GSEs can purchase next year, and just this week FHFA announced an end to the GSEs’ pilots to offer lines of credits to non-bank servicers that pledge agency mortgage servicing rights (MSRs) as collateral. Additionally, the CFPB closed its comment period on its Advance Notice of Proposed Rulemaking (ANPR) this week on the “Qualified Mortgage Definition under the Truth in Lending Act.” USMI submitted comments outlining several recommendations to the Bureau to balance prudent underwriting with consumers’ access to mortgage finance credit. Lastly, the House Financial Services Committee held a markup on several housing related bills, including legislation to reauthorize the HUD to implement credit scoring pilots in the underwriting process for FHA insured mortgages.

- The Trump Administration’s Housing Finance Reform Plans. On September 6, the U.S. Treasury Department and the U.S. Department of Housing and Urban Development (HUD) released their comprehensive Housing Reform Plan and Housing Finance Reform Plan to end the federal conservatorships of the government sponsored enterprises (GSEs), which have lasted more than 11 years. USMI released a statement that applauds Treasury and HUD for their comprehensive plans and calls for Congress to address the underlying structural challenges of the GSEs. USMI wrote, “the Administration’s proposals to reduce taxpayer risk exposure and address the areas of misaligned incentives of the GSEs while increasing transparency and market discipline could be the catalyst to break the legislative logjam and enable policymakers to enact comprehensive reforms.” USMI also appreciates that Treasury and HUD identified specific areas where the Administration can focus its efforts to put the housing finance system on a more sustainable path. Many of the actions proposed by the Administration’s Plans align with USMI’s principles for Administrative Reform, including increasing transparency in the housing finance system and expanding the role of private capital ahead of taxpayer risk.

- Senate Banking Committee Hearing. After the release of the Administration’s Plans, the U.S. Senate Committee on Banking, Housing, and Urban Affairs held a hearing on September 10 titled “Housing Finance Reform: Next Steps,” in which HUD Secretary Ben Carson, Treasury Secretary Steve Mnuchin, and Federal Housing Finance Agency (FHFA) Director, Mark Calabria, delivered their testimonies and answered questions from committee members.

All three Administration officials reiterated the need for Congress to provide input on reform, inviting the Legislative Branch to take a leadership role. Treasury Secretary Mnuchin said, “[p]ending legislation, Treasury will continue to support FHFA’s administrative actions to enhance the regulation of the GSEs, promote private sector competition, and satisfy the preconditions set forth in the plan for ending the GSEs’ conservatorships.” FHFA Director Mark Calabria also noted that “[the GSEs] have expanded with the economy recently yet maintained risk and capital levels that ensure they will fail in a downturn. This pro-cyclical pattern harms low-income borrowers, making it easier to buy homes beyond their means when the economy is strong and harder to keep those homes when the economy is weak.”

Chairman Crapo (R-ID) said in his opening statement that “[m]any of the legislative recommendations in the Plans that were released are consistent with my outline to fix our housing finance system, including attracting private capital back into the market; protecting taxpayers against future bailouts; and promoting competition.” Ranking Member Brown (D-OH) summarized the foundational principles for reform around which housing stakeholders are coalescing and added that “[w]e need a housing system built on a mission to serve borrowers and renters, no matter who they are, what kind of work they do, or where they live. That means we need policies that focus on increasing service for underserved markets, like rural areas and manufactured homeowners, and borrowers who have been locked out of the housing market over decades of discrimination.” - Fifth Circuit rules on FHFA. On September 9, the Fifth Circuit ruled in favor of investors suing the U.S. Treasury Department, allowing them to proceed with previously dismissed claims alleging the FHFA exceeded its authority with “net worth sweep.” “Congress created FHFA amid a dire financial calamity, but expedience does not license omnipotence,” U.S. Circuit Judge Don R. Willett wrote for a nine-member majority. “The shareholders plausibly allege that the Third Amendment exceeded FHFA’s conservator powers by transferring Fannie and Freddie’s future value to a single shareholder, Treasury.” The case will now be discussed in a Texas federal court where it was originally filed in 2016. The court will decide whether the restored investor claims should go to trial or be resolved on summary judgement.

- FHFA increases GSEs multifamily lending caps and ends GSE MSR Pilot Program. On September 16, the FHFA increased caps on the amount of multifamily loans the GSEs can purchase next year. FHFA will now limit Fannie Mae and Freddie Mac to purchasing over $100 billion each -up from $35 billion each in the years 2018 and 2019- in multifamily-housing residential loans, between the fourth quarters of 2019 and 2020. FHFA also made other revisions to how the GSEs can conduct their multifamily businesses, now requiring that the two firms must have over one-third (37.5 percent) of their multifamily activities directed toward affordable housing. Furthermore, the new lending caps eliminate exclusions that allowed the GSEs to purchase loans in excess of the limits previously in place.

“Multifamily housing is a critical component of addressing our nation’s shortage of affordable housing,” said FHFA Director Mark Calabria. “These new multifamily caps eliminate loopholes, provide ample support for the market without crowding out private capital, and significantly increase affordable housing support over previous levels. The Enterprises should also manage under the caps to provide consistent, stable liquidity to the market throughout the entire five-quarter period.”

Earlier this week, FHFA announced an end to the GSEs’ pilot program to finance MSRs. It was reported on May 7, that Freddie Mac had provided lines of credit for several nonbank servicers. In making the announcement, Director Calabria noted “[t]he MSR market is already served by a wide assortment of highly competitive private sources of capital and financing. Going forward, the Enterprises should focus on activities that are core to the guaranty business, mitigate risk, and are essential to end the conservatorships.” - CFPB closes comment period on QM definition. On September 16, the Consumer Financial Protection Bureau (CFPB) closed its comment period on its ANPR on the “Qualified Mortgage (QM) Definition under the Truth in Lending Act,” in light of the pending expiration of the provision commonly referred to as the “GSE Patch” in January 2021. USMI applauded the CFPB’s initiative of undertaking an assessment of this critical rule. It submitted a comment letter offering specific recommendations for replacing the current “GSE Patch” to establish a single transparent and consistent QM definition in a way to balance access to mortgage finance credit and proper underwriting guardrails to ensure consumers’ ability-to-repay (ATR). USMI’s recommendations include:

- Maintaining the ATR and product restrictions as part of any updates to the QM definition to ensure discipline in the lending community and to protect consumers;

- Retaining specific underwriting guardrails such as a debt-to-income (DTI) threshold but notes that DTI should not be a stand alone factor for ATR. Further, the USMI comment letter demonstrates through data that the DTI threshold should be adjusted to better serve consumers;

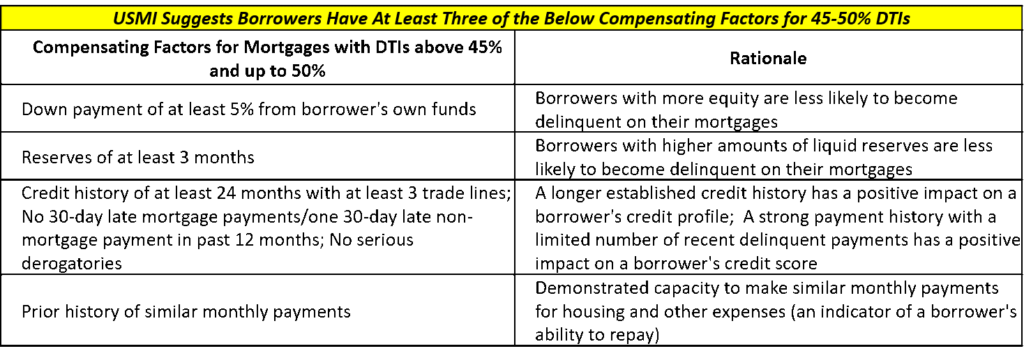

- Because DTI should not be a stand along measure of ATR, USMI recommends developing a single set of transparent compensating factors for loans with DTIs above 45 and up to 50 percent for defining QM across all markets, similar to how the GSEs, FHA, and VA use compensating factors in their respective markets today.

Importantly, nine Democratic U.S. Senators led by Senate Banking Ranking member Sherrod Brown sent a letter to the Bureau stating that as it considered amending the existing QM rule, the Bureau “must not undermine the elements of the rule that have made it effective: prohibitions on unsustainable product features and a verifiable demonstration at loan origination that the lender has evaluated the borrower’s ability to repay their loan.”

Other associations and entities such as the National Association of Hispanic Real Estate Professionals (NAHREP), National Association of Home Builders, Digital Federal Credit Union, National Association of Federally-Insured Credit Unions (NAFCU), CNB Bank, International Bancshares Corporation, Wisconsin Credit Union League, Highlands Residential Mortgage, among others, share similar views as USMI that setting transparent compensating factors will help expand credit availability for many potential homeowners who may otherwise be left behind.

- House Financial Services Committee Markup. On September 18-20, the U.S. House of Representatives Committee on Financial Services, held a markup hearing in which, along with several issues, they discussed H.R. 123, the “Alternative Data for Additional Credit FHA Pilot Program Reauthorization Act,” and reported the legislation favorably to the House with a 32-22 vote. This bill would reauthorize the HUD statutory authority to implement a pilot program to increase credit access for borrowers with thin or no credit files through the use of additional credit data in the underwriting for FHA-insured mortgages.