USMI releases details on the developments and growth of private mortgage insurance credit risk transfer

WASHINGTON — U.S. Mortgage Insurers (USMI) today announced that private mortgage insurance (MI) companies transferred nearly $34 billion in risk on nearly $1.3 trillion of insurance-in-force from 2015 to 2019. USMI released details on the developments and growth of the MI credit risk transfer (MI CRT) market, which outlines the types of structures being used by the industry to transfer risk to reduce volatility and exposure of mortgage credit risk within the mortgage finance system, including to the government sponsored-enterprises (GSEs), and therefore taxpayers. It also finds that active adoption of CRT by private mortgage insurers has transformed the industry to help better insulate it from the cyclical mortgage market and enhanced their ability to be more stable, long-term managers and distributors of risk.

“Through innovative new MI CRT structures, the industry is taking additional steps to enhance MI resiliency and the risk protection provided to the conventional mortgage market. MI CRT demonstrates that MI companies are sophisticated experts in pricing and actively managing mortgage credit risk,” said Lindsey Johnson, President of USMI. “Private MI plays a critical function in the housing finance system by serving as the first layer of protection against mortgage defaults. MI is also one of the only sources of private capital that has been available through all market cycles. After the financial crisis, the MI industry improved its safety and soundness through enhanced capital and operational standards, which in turn made us more resilient to withstand severe economic stress.”

USMI examined the two main MI CRT structures: Reinsurance and Capital Markets. It found that mortgage insurers have executed 18 reinsurance deals since 2015, transferring over $25 billion of risk on over $530 billion of insurance-in-force. As for the Capital Markets structure, the industry introduced MI Insurance Linked Note (ILN) programs beginning in 2015. Since then, mortgage insurers have issued 19 ILN deals, transferring $7.8 billion of risk on over $730 billion ofinsurance-in-force.

“While the MI industry has distributed credit risk for decades, these innovative CRT structures adopted by the industry in 2015 have transformed it from a ‘buy-and-hold’ into an ‘aggregate-manage-and-distribute’ model,” said Johnson. “The financial risk management approach of private MI companies has become much more countercyclical and significantly benefits the housing finance system.”

Because private mortgage insurers typically hold a portion of the first loss there is an alignment of incentives that ensures quality underwriting continues to be done by the industry, which reduces investors’ risk exposure, and ensures quality control on risk for investors and within the broader financial system. The investor base in these transactions continues to grow exponentially as the frequency of transactions increases, and the MI CRT investors to date represent trillions of dollars of private capital under management that provides a stable, deep pool of liquidity for the market.

“The MI CRT structures underscore the resilient nature and benefits of MI and the private capital it supplies to the housing market, safeguarding taxpayers against mortgage defaults, and ensuring that the private MI industry will continue to play a vital role in the mortgage finance system,” added Johnson.

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership.

Congress is back from recess, Pumpkin Spice lattes are back on the menu, and housing finance reform is back at the top of news headlines in Washington this fall. In September, the Trump Administration released plans to reform the nation’s housing finance system. USMI issued a statement applauding the initiative and calling for Congress to address the GSEs’ underlying structural challenges and promote a coordinated federal housing policy. The Senate Banking Committee also held a hearing on the matter to learn more about the Administration’s Plans. The same week that the Administration released its Plans, the Fifth Circuit ruled in favor of GSE shareholders in their lawsuit against the U.S. Treasury, as the court allowed the shareholders to reinstate claims alleging that FHFA is unconstitutionally structured. While the fate of the legal challenges is still unclear, what is clear is that FHFA is moving ahead on many of its plans to review and make changes to the current programs and activities of the GSEs. Last week, FHFA announced an increase to the caps on the amount of multifamily loans the GSEs can purchase next year, and just this week FHFA announced an end to the GSEs’ pilots to offer lines of credits to non-bank servicers that pledge agency mortgage servicing rights (MSRs) as collateral. Additionally, the CFPB closed its comment period on its Advance Notice of Proposed Rulemaking (ANPR) this week on the “Qualified Mortgage Definition under the Truth in Lending Act.” USMI submitted comments outlining several recommendations to the Bureau to balance prudent underwriting with consumers’ access to mortgage finance credit. Lastly, the House Financial Services Committee held a markup on several housing related bills, including legislation to reauthorize the HUD to implement credit scoring pilots in the underwriting process for FHA insured mortgages.

The Trump Administration’s Housing Finance Reform Plans. On September 6, the U.S. Treasury Department and the U.S. Department of Housing and Urban Development (HUD) released their comprehensive Housing Reform Plan and Housing Finance Reform Plan to end the federal conservatorships of the government sponsored enterprises (GSEs), which have lasted more than 11 years. USMI released a statement that applauds Treasury and HUD for their comprehensive plans and calls for Congress to address the underlying structural challenges of the GSEs. USMI wrote, “the Administration’s proposals to reduce taxpayer risk exposure and address the areas of misaligned incentives of the GSEs while increasing transparency and market discipline could be the catalyst to break the legislative logjam and enable policymakers to enact comprehensive reforms.” USMI also appreciates that Treasury and HUD identified specific areas where the Administration can focus its efforts to put the housing finance system on a more sustainable path. Many of the actions proposed by the Administration’s Plans align with USMI’s principles for Administrative Reform, including increasing transparency in the housing finance system and expanding the role of private capital ahead of taxpayer risk.

Senate Banking Committee Hearing. After the release of the Administration’s Plans, the U.S. Senate Committee on Banking, Housing, and Urban Affairs held a hearing on September 10 titled “Housing Finance Reform: Next Steps,” in which HUD Secretary Ben Carson, Treasury Secretary Steve Mnuchin, and Federal Housing Finance Agency (FHFA) Director, Mark Calabria, delivered their testimonies and answered questions from committee members.

All three Administration officials reiterated the need for Congress to provide input on reform, inviting the Legislative Branch to take a leadership role. Treasury Secretary Mnuchin said, “[p]ending legislation, Treasury will continue to support FHFA’s administrative actions to enhance the regulation of the GSEs, promote private sector competition, and satisfy the preconditions set forth in the plan for ending the GSEs’ conservatorships.” FHFA Director Mark Calabria also noted that “[the GSEs] have expanded with the economy recently yet maintained risk and capital levels that ensure they will fail in a downturn. This pro-cyclical pattern harms low-income borrowers, making it easier to buy homes beyond their means when the economy is strong and harder to keep those homes when the economy is weak.”

Chairman Crapo (R-ID) said in his opening statement that “[m]any of the legislative recommendations in the Plans that were released are consistent with my outline to fix our housing finance system, including attracting private capital back into the market; protecting taxpayers against future bailouts; and promoting competition.” Ranking Member Brown (D-OH) summarized the foundational principles for reform around which housing stakeholders are coalescing and added that “[w]e need a housing system built on a mission to serve borrowers and renters, no matter who they are, what kind of work they do, or where they live. That means we need policies that focus on increasing service for underserved markets, like rural areas and manufactured homeowners, and borrowers who have been locked out of the housing market over decades of discrimination.”

Fifth Circuit rules on FHFA. On September 9, the Fifth Circuit ruled in favor of investors suing the U.S. Treasury Department, allowing them to proceed with previously dismissed claims alleging the FHFA exceeded its authority with “net worth sweep.” “Congress created FHFA amid a dire financial calamity, but expedience does not license omnipotence,” U.S. Circuit Judge Don R. Willett wrote for a nine-member majority. “The shareholders plausibly allege that the Third Amendment exceeded FHFA’s conservator powers by transferring Fannie and Freddie’s future value to a single shareholder, Treasury.” The case will now be discussed in a Texas federal court where it was originally filed in 2016. The court will decide whether the restored investor claims should go to trial or be resolved on summary judgement.

FHFA increases GSEs multifamily lending caps and ends GSE MSR Pilot Program. On September 16, the FHFA increased caps on the amount of multifamily loans the GSEs can purchase next year. FHFA will now limit Fannie Mae and Freddie Mac to purchasing over $100 billion each -up from $35 billion each in the years 2018 and 2019- in multifamily-housing residential loans, between the fourth quarters of 2019 and 2020. FHFA also made other revisions to how the GSEs can conduct their multifamily businesses, now requiring that the two firms must have over one-third (37.5 percent) of their multifamily activities directed toward affordable housing. Furthermore, the new lending caps eliminate exclusions that allowed the GSEs to purchase loans in excess of the limits previously in place.

“Multifamily housing is a critical component of addressing our nation’s shortage of affordable housing,” said FHFA Director Mark Calabria. “These new multifamily caps eliminate loopholes, provide ample support for the market without crowding out private capital, and significantly increase affordable housing support over previous levels. The Enterprises should also manage under the caps to provide consistent, stable liquidity to the market throughout the entire five-quarter period.”

Earlier this week, FHFA announced an end to the GSEs’ pilot program to finance MSRs. It was reported on May 7, that Freddie Mac had provided lines of credit for several nonbank servicers. In making the announcement, Director Calabria noted “[t]he MSR market is already served by a wide assortment of highly competitive private sources of capital and financing. Going forward, the Enterprises should focus on activities that are core to the guaranty business, mitigate risk, and are essential to end the conservatorships.”

CFPB closes comment period on QM definition. On September 16, the Consumer Financial Protection Bureau (CFPB) closed its comment period on its ANPR on the “Qualified Mortgage (QM) Definition under the Truth in Lending Act,” in light of the pending expiration of the provision commonly referred to as the “GSE Patch” in January 2021. USMI applauded the CFPB’s initiative of undertaking an assessment of this critical rule. It submitted a comment letter offering specific recommendations for replacing the current “GSE Patch” to establish a single transparent and consistent QM definition in a way to balance access to mortgage finance credit and proper underwriting guardrails to ensure consumers’ ability-to-repay (ATR). USMI’s recommendations include:

Maintaining the ATR and product restrictions as part of any updates to the QM definition to ensure discipline in the lending community and to protect consumers;

Retaining specific underwriting guardrails such as a debt-to-income (DTI) threshold but notes that DTI should not be a stand alone factor for ATR. Further, the USMI comment letter demonstrates through data that the DTI threshold should be adjusted to better serve consumers;

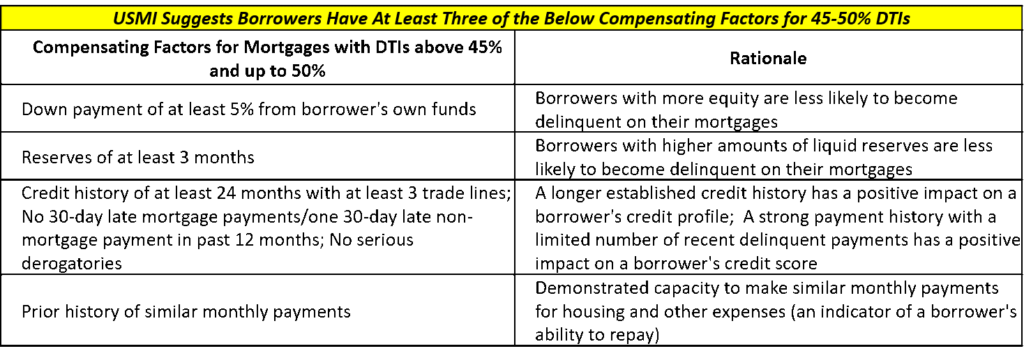

Because DTI should not be a stand along measure of ATR, USMI recommends developing a single set of transparent compensating factors for loans with DTIs above 45 and up to 50 percent for defining QM across all markets, similar to how the GSEs, FHA, and VA use compensating factors in their respective markets today.

Importantly, nine Democratic U.S. Senators led by Senate Banking Ranking member Sherrod Brown sent a letter to the Bureau stating that as it considered amending the existing QM rule, the Bureau “must not undermine the elements of the rule that have made it effective: prohibitions on unsustainable product features and a verifiable demonstration at loan origination that the lender has evaluated the borrower’s ability to repay their loan.”

House Financial Services Committee Markup. On September 18-20, the U.S. House of Representatives Committee on Financial Services, held a markup hearing in which, along with several issues, they discussed H.R. 123, the “Alternative Data for Additional Credit FHA Pilot Program Reauthorization Act,” and reported the legislation favorably to the House with a 32-22 vote. This bill would reauthorize the HUD statutory authority to implement a pilot program to increase credit access for borrowers with thin or no credit files through the use of additional credit data in the underwriting for FHA-insured mortgages.

As the August recess begins, there have been several notable developments in housing finance. Last Thursday, the Consumer Financial Protection Bureau (CFPB) released its Advanced Notice of Proposed Rulemaking on the “Qualified Mortgage (QM) Definition under the Truth in Lending Act” which seeks to revise the QM definition as the GSE Patch nears expiration. Moody’s Investor Service released a proposed update to its residential mortgage-backed security (RMBS) rating methodology which would affect the rating for bonds associated with the GSEs’ CRT transactions and non-agency RMBS. Importantly, the new standard recognizes the loss reducing benefits of private mortgage insurance (MI). The Urban Institute published an article highlighting private MI and the benefits of reducing the severity of losses for those holding mortgage credit risk.

Also, on the regulatory front, as many financial institutions look to implement the Financial Accounting Standards Board’s (FASB) Current Expected Credit Loss (CECL) accounting standard, FASB has announced proposed changes, including delaying the implementation deadline for private companies as well as small public companies. USMI released an update on the treatment of loan level credit enhancement provided under the CECL standard, providing information to lenders of all sizes on how they might mitigate loss reserve requirements under the new standard. Housing finance reform continues to gain attention in recent weeks with Federal Housing Finance Agency (FHFA) Director Mark Calabria recently giving an update on the timing of the release of the Administration’s plans to reform the housing finance system. Lastly, there have been a number of studies and reports in recent weeks that continue to cite consumers’ misperception that they need a large down payment to qualify for homeownership. USMI published a new column that highlights low down payment mortgage options available to help home-ready borrowers attain sustainable homeownership sooner.

CFPB’s ANPR on Qualified Mortgages. On July 25, the CFPB released an Advanced Notice of Proposed Rulemaking on the “Qualified Mortgage Definition under the Truth in Lending Act.” The CFPB is considering whether to revise the QM definition in light of the pending expiration of the Temporary GSE QM loan category provision, commonly referred to as the “GSE Patch,” in January 2021. The same statutory product restrictions exist for loans under the Patch as for other QM loans, however these loans are not subject to the 43 percent debt-to-income (DTI) limit—a significant exception that has supported a substantial portion of the overall housing market. As takers of first-loss mortgage credit risk with more than six decades of expertise and experience underwriting and actively managing that risk, USMI members understand the need to balance prudent underwriting using a clear and transparent standard to ensure sustainable lending with the need to maintain access to affordable mortgage finance credit for home-ready borrowers. Following the release of the ANPR, USMI published a blog with observations and recommendations for replacing the GSE Patch.

Moody’s releases proposed update to RMBS ratings. Moody’s recently released a proposed update to its RMBS rating methodology which would affect the rating for bonds associated with the GSEs’ CRT transactions and non-agency RMBS. Importantly, the new standard gives more credit to deals with private MI. USMI submitted a letter on July 29 to Moody’s in response to request for comment by Moody’s on the new standard, which among other things commends Moody’s for many of the necessary updates provided in the proposed standard and asks for additional transparency around details about the benefits of MI, the proposed rejection rates, and Moody’s methodology for determining maximum insurance payout and allocation based on an insurer’s rating.

Urban Institute publishes article on risk reducing benefits of PMI. Urban Institute released a paper entitled, “Private Mortgage Insurance Reduces the Severity of Losses for Those Holding Risk,” that focuses on Moody’s recent proposed updates to its RMBS rating methodology, which will affect the ratings of bonds for the GSEs’ CRT deals and non-agency RMBS, and would give more credit to deals with MI. In the report, Urban notes, “given the increased focus on the topic, understanding the historical behavior of GSE loans with mortgage insurance is important. Examining Fannie Mae loans from 1999 through the first quarter of 2018, we conclude that PMI reduces the loss severity of loans with high loan-to-value (LTV) ratios by 19 to 24 percentage points—a very substantial reduction. So, it is important to recognize PMI’s contribution when developing measures assessing loan-level risk, giving proper “credit” in sizing capital requirements or assessing subordination levels for securitizations.”

Current Expected Credit Loss (CECL) accounting standard. Over the last couple of weeks, FASB has announced several proposed changes for the CECL accounting standard, including delaying the implementation deadline for private companies as well as small public companies (those with a market capitalization below $250 million and annual revenue of less than $100 million). If that proposal is enacted, the standard for those companies would not take effect until January 2023. CECL is a fundamental shift in how loss reserves are accounted for and incurred. Instead of waiting until losses are probable, institutions will forecast losses and establish reserves at the time of origination. The final rule was announced on June 16, 2016 and will impact any financial institution that holds loans on its balance sheet at amortized cost, such as banks, credit unions, and real estate investment trusts (REITs). Public companies filing with the Securities and Exchange Commission (SEC) will need to adopt CECL for fiscal years beginning after December 15, 2019, including interim periods within those fiscal years.

As noted by the Government Accountability Office (GAO), “CECL is considered by some to be the most significant accounting change in the banking industry in 40 years.” Banking regulators – the Federal Deposit Insurance Corporation (FDIC), Federal Reserve, and Office of the Comptroller of the Currency (OCC) – jointly issued a final rule on CECL’s implementation and have proposed changing the allowance for home and lease losses as a new defined term.

Ahead of the implementation, and as lenders look to prepare as the implementation deadline approaches, USMI published a fact sheet on their website to provide information to lenders about the potential impact CECL may have on their books of business and how loan level credit enhancement, such as private MI, can help offset loss reserve requirements.

FHFA Director gives update on the Administration’s GSE plan. In March President Trump signed an Executive Order that directed federal agencies, most notably the Treasury Department and the Department of Housing and Urban Development, to provide both administrative and legislative solutions for modernizing the housing finance system and ending the conservatorships of the GSEs. Recently in an interview with Reuters, FHFA Director Mark Calabria said that he now expects the Administration will release reports developed by the Departments of Treasury and of Housing and Urban Development that outline the Administration’s plan for releasing Fannie Mae and Freddie Mac from conservatorship to be published at the end of August or early September

Last fall, USMI released a white paper highlighting several areas of alignment around administrative reform that can be implemented in lieu of comprehensive legislative action by Congress. The specific recommendations proposed by USMI include reducing the duopolistic market power of the GSEs, increasing transparency, expanding private capital and reducing taxpayer risk, and promoting a strong regulator that establishes uniform standards and uses transparent processes to assess the GSEs activities and products.

USMI publishes new column on low down payment options. Earlier this month, USMI published a new column, “Buy a home without breaking the bank.” The column highlights the several solutions available to financial obstacles that may arise when buying a home, such as the 20 percent down payment. According to a recent report, 49 percent of non-homeowners stated that not having enough money for a down payment and closing costs was a major obstacle to purchasing a home. But data shows many aspiring homebuyers can afford to buy a home with less than 20 percent. Another survey found that among first-time homebuyers who obtained a mortgage, approximately 80 percent had down payments of less than 20 percent. The article links readers to LowDownPaymentFacts.com where consumers can learn about the number of different low down payment mortgage options available to them and how to become “home-ready.”

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

The Consumer Financial Protection Bureau (CFPB) just released an Advanced Notice of Proposed Rulemaking on the “Qualified Mortgage Definition under the Truth in Lending Act.” The CFPB is considering whether to revise the Qualified Mortgage (QM) definition in light of the pending expiration of the provision commonly referred to as the GSE Patch (or Temporary GSE QM loan category) in January 2021. The same statutory product restrictions exist for loans under the Patch as for other QM loans, however these loans are not subject to the 43 percent debt-to-income (DTI) limit—a significant exception that has supported a substantial portion of the overall housing market. Considering a robust market has developed under the GSE Patch, any changes could substantially impact consumers’ access to mortgage finance as well as determine the level of risk within the mortgage finance system, which has implications for homeowners, financial institutions, and taxpayers.

As takers of first-loss mortgage credit risk with more than six decades of expertise and experience underwriting and actively managing that risk, USMI members understand the need to balance prudent underwriting with the need to ensure there is a clear and transparent standard that maintains access to affordable and sustainable mortgage finance credit for home-ready borrowers. As different stakeholders contemplate what to do next with the Patch, USMI offers a few observations and recommendations for replacing the QM Patch.

Observations

DTI is not the best or most predictive factor in assessing consumers’ ability-to-repay. Pre-financial crisis, one of the most egregious lending practices was making loans to individuals without a reasonable consideration of their financial ability-to-repay (ATR) the loan. As policymakers and regulators aimed to ensure consumers had at least some reasonable ATR their mortgages going forward, the 43 percent DTI cap was established as part of the CFPB’s QM rule. While DTI is not necessarily the most predictive measure, historical data (especially for 2004-2007 cohorts of loans) demonstrates that higher DTIs are correlated to higher defaults (and predictive of a consumer’s ATR).[i] Yet, DTI is only one measure.

USMI and others have identified more predictive borrower characteristics, most notably that reserves in a bank account are more indicative of an individual’s ATR than many other factors. According to a recent report by JPMorgan Chase Institute,[ii] when a borrower has three months of reserves (funds to cover mortgage payments) in the bank, these borrowers were five times less likely to default on their mortgage as those who had insufficient cash in the bank to cover one mortgage payment. According to the JPMorgan Chase Institute report, homeowners who had less than one month’s mortgage payment in savings made up 20 percent of the people in their survey but made up 54 percent of the people in the survey who defaulted on their loans.

While DTI is one factor for assessing ATR, by simply limiting the market to a hard 43 percent limit, many home-ready borrowers will be cut out of the market. In fact, roughly 30 percent of the GSEs’ market today is above the 43 percent DTI limit. CoreLogic estimates that the total loan origination volume for 2018 for loans that were above the 43 percent limit was roughly $260 billion out of a $1.6 trillion market in 2018[iii] (though this number could be higher because some banks have chosen to hold loans in their portfolio that are above the 43 percent DTI limit).

The need for transparency and input on compensating factors. Since the implementation of the QM Rule and the GSE Patch, the market has seen that many good quality loans have been above the 43 percent DTI limit. For loans with higher DTI under the Patch, the market has adapted and relied on compensating factors to adjust for and mitigate the additional risk. These compensating factors are done as part of the GSEs’ automated underwriting systems (AUSs). The current AUSs and the compensating factors used within them are not transparent to stakeholders or the public. However, as mortgage insurers and others analyze GSE loans with higher DTIs, we can begin to back-in to what the compensating factors are and when they come into play for higher DTI GSE loans.

Recommendations

ATR and product restrictions should remain as part of any updates to the QM rule. USMI believes the requirements for assessing a borrower’s ATR that require the lender to underwrite the consumer using credit, income and asset documentation should remain as critical components to any enhancements to the rule. It is also essential that the QM statutory product restrictions remain intact to maintain discipline in the lending community as well as to protect consumers.

A single, transparent underwriting standard for defining QM criteria should be established. USMI recommends a list of transparent mitigating underwriting criteria (compensating factors) for loans with DTIs between 45 and 50 percent for defining QM (in addition to the existing statutorily defined product features and ATR underwriting criteria) be established. While USMI has developed a list of proposed criteria (see below), the list of criteria could ultimately be set by a non-profit membership organization or standard-setting body.

A transparent and easy-to-understand and use set of underwriting criteria can be programmed to allow for manual underwriting or automatic underwriting engines. Further, any private market participant could publish or code these criteria in their investor requirements. For the GSEs, it would remain in the purview of the Federal Housing Finance Agency (FHFA) Director to determine whether the GSEs could guarantee high DTI loans. If not, the loans would simply receive an “Approve/Ineligible” or “Accept/Ineligible” AUS decision. This approach would level the playing field between market participants, allow for continued innovation around documentation, verification, and other underwriting standards, and force the GSEs’ AUSs to become more transparent.

Proposed Set of Compensating Factors

Importantly, USMI believes that there should be one industry standard with complete transparency into the credit decisioning factors used for underwriting mortgage credit risk and that input from industry should be allowed on updates to the underwriting criteria. Further, any changes related to maximum DTIs should be consistent across different lending channels (e.g., FHA and GSEs) to ensure there is not market arbitrage to achieve QM status.

Appendix Q needs to be addressed. All proposals to assess and define an ATR will have challenges or shortcomings. For any proposal that includes DTI, there is still the challenge of addressing the acknowledged limitations of Appendix Q, including to allow lenders to document and verify borrower income and assets utilizing new innovations in the industry. A possible permanent fix to address Appendix Q could be to allow for the GSEs’ guides to be maintained by a regulatory body outside of the GSEs and updated as necessary. Legislation is needed if Appendix Q is to allow for the use of guides or handbooks of the GSEs or other agencies.

APOR could remain the determinant for the Safe Harbor protection but should not be the replacement for DTI requirement and Underwriting Criteria. Further, to provide a more level playing field between the Federal Housing Administration (FHA) and the conventional market, the annual percentage rate (APR) cap of Average Prime Offer Rate (APOR) + 150 bps needs to be increased to account for GSE LLPAs and private mortgage insurance. Setting the cap for QM Safe Harbor protection at 200 bps over APOR + 200 bps will limit the shift of riskier, high-LTV business to FHA, preserve greater private capital participation in the pricing of risk, and promote better taxpayer protection.

Buying a home is one of life’s biggest financial milestones, but people often think it’s out of reach because of the costs involved, including the myth that you have to put 20% down. The fact is, you don’t necessarily need to deplete all of your savings to qualify for a mortgage and you can purchase a home sooner than many people believe.

You aren’t alone in thinking you can’t afford a home right now. According to a recent report, 49% of non-homeowners stated that not having enough money for a down payment and closing costs was a major obstacle to purchasing a home. But when you look at the data, many aspiring homebuyers can afford to buy a home with less than 20%. In fact, another recent survey found that among first-time homebuyers who obtained a mortgage, approximately 80% had down payments of less than 20%.

There are several low down payment mortgage options available to you, such as conventional loans with private mortgage insurance (MI) or government-backed loans like those insured by the Federal Housing Administration (FHA).

For example, a qualified borrower can get a conventional loan with private MI for as little as 3% down. If he or she waited to save for a 20% down payment, it could take up to 20 years to save that amount, plus closing costs, for a $262,250 house — the national median sales price in 2018 according to the National Association of REALTORS®. That wait time is trimmed down to seven years when buying a home with a 5% down, where the loan is sustainably backed by private MI. Purchasing a home with less down using private MI can also help ensure you continue to have prudent savings, and can free up funds that you can use for other important home purchases – such as renovations, appliances, and furniture.

There are other mortgage options available to you as well, such as government-backed FHA loans that allow you to put down as little as 3.5%. However, unlike private MI, which can be canceled once you reach 20% equity in your home, the mortgage insurance premiums attached to FHA loans typically can’t be canceled and remain throughout the life of the loan.

It’s important to know what home loan option is best for you, and you should speak with a mortgage lender to help inform your decision. The bottom line, however, is that there are affordable low down payment home loan options out there, which could mean the difference between getting into your home sooner, allowing you to build wealth through home equity, or waiting for years while renting. By taking advantage of home loans backed by private MI, you can spend less time worrying about a down payment and more time enjoying your new home.

Getting into your new home with private MI and keeping more of your hard-earned money in the bank can be a very smart way to invest in your future. Check out www.LowDownPaymentFacts.com to learn more.

Washington is buzzing with activity on the housing finance front, both in market developments and policy discussions as FHFA Director Calabria continues to outline his plans for Fannie Mae and Freddie Mac (“the GSEs”).

Also, June is National Homeownership Month! On June 5, USMI released a new report on how private mortgage insurance (MI) helps borrowers get into homes sooner. Brad Shuster, USMI Chairman and Executive Chairman of the Board of NMI Holdings, Inc., penned an op-ed in The Hill highlighting some key points from the report. In addition, the Federal Housing Finance Agency (FHFA) finalized their Single Security Initiative to create a common single-family securities program for the GSEs after the launch of the Uniform Mortgage-Backed Security (UMBS). Fannie Mae published the results of a nationally representative survey that revealed most consumers overestimate the requirements to get a mortgage. Lastly, the Senate confirmed two key positions for the U.S. Department of Housing and Urban Development (HUD) and the Senate Banking Committee scheduled a hearing entitled “Should Fannie Mae and Freddie Mac be Designated as Systemically Important Financial Institutions (SIFIs)?”

USMI releases state-by-state report on role of private MI. USMI released its second annual report on the role of private MI facilitating low down payment lending in all 50 states and the District of Columbia. The report found more than 30 million homeowners have been served by MI since 1957, including more than one million people in 2018 alone, and breaks down on a state-by-state basis, low down payment mortgage lending with private MI. It also provides an analysis of how long it would take those borrowers to save for a 20 percent versus a five percent down payment. The report finds that the top five states for the number of borrowers helped by private MI in 2018 were Texas, Florida, California, Illinois, and Ohio. The complete report on MI in the U.S. is available here.

Brad Shuster, USMI Chairman and Executive Chairman of the Board of NMI Holdings, Inc, penned an op-ed in The Hill. Shuster celebrated National Homeownership Month with an op-ed in The Hill that highlights the national conversation about how to best reform the U.S. housing finance system to sustain and grow homeownership in a safe and affordable way. Importantly, Shuster highlights the very important role that private MI plays in ensuring home-ready borrowers have access to sustainable low-down payment lending. Mr. Shuster notes that the recently released USMI state-by-state report, “showcases how private MI helps hard-working, home-ready families access the conventional mortgage market, even when they don’t have a large down payment.”

Shuster also notes the importance for policymakers to understand the “long, time-tested role MI has played as they seek to create a more robust housing finance system. Private MI serves as protection against mortgage credit risk if a borrower defaults on their mortgage.”

FHFA sends Annual Report to Congress and Director Calabria calls for legislative reforms. Last week, FHFA sent its Annual Report to Congress, which included Director Calabria’s legislative recommendations for housing finance reform. In the FHFA 2018 Report to Congress, FHFA reported on a number of activities executed over the last year by the GSEs. While the report was drafted (and likely finalized) prior to Director Calabria’s confirmation (FHFA is required to submit the report each year before June 15), the Director wrote an opening letter to Chairman Mike Crapo (R-ID) and Ranking Member Sherrod Brown (D-OH) to reiterate his priorities for the GSEs. Director Calabria underscored the need for reform, stressing that taxpayers remain exposed to undue mortgage credit risk and to urge Congress to enact legislation.

In the letter, Director Calabria outlined specific recommendations for legislative reforms, including a request for Congress to give him authority to grant new charters to increase competition against the GSEs’ “duopoly” suggesting, “[t]o promote competition, Congress should authorize additional competitors and provide FHFA chartering authority similar to that of the Office of the Comptroller of the Currency.” He also called for Congress to grant FHFA additional authority to provide oversight of counterparties and suggested that FHFA should have greater discretion over the GSEs’ regulatory capital. While Director Calabria has noted in public speeches that only Congress has the authority to provide for an explicit government guaranty, he did not specifically call for Congress to establish an explicit government guaranty in his letter.

The GSEs complete their Single Security Initiative and launch UMBS. Earlier this month, Fannie Mae and Freddie Mac officially moved to issue the Uniform Mortgage-Backed Security (UMBS). According to HousingWire, the UMBS is a common security through which the GSEs will finance qualifying fixed-rate mortgage loans backed by one- to four-unit single-family properties. Previously, the GSEs only issued securities through their own programs/platforms, which meant an inevitable disparity and inconsistencies existed between the two. Fannie Mae’s program has historically been far more liquid than Freddie Mac’s, which created an imbalance between their trading volumes. Under the new initiative, FHFA will require Freddie Mac to remit homeowners’ mortgage payments to investors in 55 days rather than 45, which is consistent with Fannie Mae’s guidelines.

Following the launch, Renee Schultz, Senior Vice President of Capital Markets at Fannie Mae, released a statement calling the launch “a major milestone that marks the successful implementation of the Single Security Initiative.” FHFA Deputy Director Robert Fishman stated, “[b]y addressing structural issues and trading disparities, the UMBS will benefit taxpayers and the nation’s housing finance system.”

Fannie Mae consumer survey finds knowledge gap to obtain a mortgage. On June 5, Fannie Mae published the results of a survey of 3,647 Americans which found that most consumers vastly overestimate the requirements to obtain a mortgage. “The lack of mortgage qualification understanding is pervasive, even among current homeowners, those who say they are actively planning to purchase a home in the next three years, and those who successfully answered questions testing general financial literacy,” the researchers wrote. For example, when asked how much money a borrower is required to put down, 40% said they didn’t know. Of those who did have an idea, they cited 10% as a required minimum.

Senate Banking Focuses on the GSEs as SIFIs. The Senate Banking Committee has scheduled a hearing entitled “Should Fannie Mae and Freddie Mac be Designated as Systemically Important Financial Institutions?” The hearing is timely given FHFA Director Calabria has repeatedly said “the path out of conservatorships that we will establish for Fannie and Freddie is not going to be calendar dependent. It will be driven, first and foremost, by their ability to raise capital.” It also comes as policymakers and stakeholders wait for FHFA action following the agency’s Notice of Proposed Rulemaking on the Enterprise Capital Framework that was released last summer and for which the comment period closed in November 2018. USMI submitted a comment letter, which can be found here.

Senate confirms HUD nominees. Finally, yesterday, the Senate voted to confirm two HUD nominees: Seth Appleton to be the Assistant Secretary for Policy Development and Research; and Robert Hunter Kurtz to the be the Assistant Secretary for Public and Indian Housing.

Texas, Florida, California, Illinois, and Ohio Round Out the Top Five States for Low Down Payment Mortgage Lending

WASHINGTON, June 5, 2019 — U.S. Mortgage Insurers (USMI), the association representing the nation’s leading private mortgage insurance (MI) companies, today released its annual report detailing low down payment insured mortgage lending in all 50 states and the District of Columbia. The report breaks down on a state-by-state basis low down payment mortgage lending with private MI, including the number of borrowers helped, the percentage of borrowers who were first-time homebuyers, average loan amounts, average FICO credit scores, and provides an analysis of how long it would take those borrowers to save for a 20 percent versus a five percent down payment.

“No, you do not need a 20 percent down payment to gain mortgage approval,” said Lindsey Johnson, President of USMI. “Our report underscores the critical role private MI plays in helping millions of first-time and middle-income homebuyers bridge the down payment gap across the United States. For over 60 years, private MI has helped provide Americans with affordable access to mortgage credit while also protecting taxpayers and the federal government from undue mortgage credit risk. Millions of borrowers have relied on private MI to responsibly purchase homes and MI will continue to facilitate the dream of homeownership going forward,” continued Johnson.

USMI finds that it could take 20 years for a household earning the national median income of $61,372 to save 20 percent (plus closing costs) for a $262,250 single-family home, the national median sales price. However, that wait time drops to seven years if the household purchases a home with a 5 percent down, where the loan is sustainably backed by private MI. This represents a 65 percent decrease in wait time at the national level, and USMI found the same percentage decrease at the state level.

Since 1957, MI has helped more than 30 million families qualify for a mortgage. In 2018 alone, MI helped more than one million borrowers purchase or refinance a mortgage, nearly 60 percent of which were first-time homebuyers, and more than 40 percent had annual incomes below $75,000. The average loan amount purchased or refinanced with MI was $244,715 and the average FICO score for these borrowers was 741, compared to a 733 score for all home loan borrowers. The below table shows the top five states in which MI was used by borrowers to purchase or refinance homes in 2018.

State

Number of Borrowers Helped with Private MI

First-Time Homebuyers

Texas

89,738

57 percent

Florida

77,565

56 percent

California

71,996

69 percent

Illinois

48,200

65 percent

Ohio

43,761

59 percent

In addition to the findings on how MI helps borrowers qualify for low down payment mortgages, the report also highlights the role MI plays in reducing the federal government’s, and therefore U.S. taxpayers’, exposure to mortgage credit risk. Private MI serves as credit protection against mortgage credit risk in the event a borrower defaults on his or her mortgage, meaning every dollar that an MI company covers when a borrower defaults on his or her mortgage is a dollar that the GSEs and taxpayers do not have to pay. In fact, since the 2008 financial crisis the MI industry has paid over $50 billion in claims – losses the government and taxpayers did not have to bear.

“The fact that private mortgage insurance has been helping Americans qualify for low down payment mortgages for more than six decades is a testament to the important access, stability, and credit protection the MI industry brings to the housing finance system,” added Johnson. “In recent years, the private MI industry has become even stronger with more robust underwriting standards, stronger capital requirements, and improved risk management. The industry is well-positioned to continue its important work, and we look forward to further helping grow American homeownership.”

The complete report on MI in the U.S. is available here, along with all 50 state fact sheets and data for the District of Columbia.

WASHINGTON — Lindsey Johnson, President of U.S. Mortgage Insurers (USMI), today issued the following statement on the U.S. Senate’s confirmation of Dr. Mark Calabria as the Federal Housing Finance Agency (FHFA) Director:

“USMI applauds the Senate’s confirmation of Director Mark Calabria to serve as the next FHFA Director. Fannie Mae and Freddie Mac (the ‘GSEs’), the 11 Federal Home Loan Banks, market participants, and American homebuyers will be well-served under Director Calabria’s leadership at this critical time in the housing finance system.

“Director Calabria’s deep understanding of the mortgage finance system will be invaluable in promoting a more robust housing market that provides borrowers with access to affordable low down payment mortgage credit while simultaneously protecting taxpayers from undue mortgage credit risk. Director Calabria has long been an advocate for greater taxpayer protection against mortgage credit risk, including the use of private mortgage insurance (MI) to shield taxpayers and the federal government from financial risk on low down payment lending. We are confident that Director Calabria will continue to recognize the importance of private MI in the housing finance system.

“We look forward to working closely with Director Calabria to ensure that homebuyers continue to have affordable and prudent options for low down payment mortgage finance credit while also protecting taxpayers. For more than 60 years, private mortgage insurers have played a leading role in promoting affordable and sustainable homeownership and we look forward to building upon this important mission in the future.”

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

It has been a busy week in Washington with renewed attention on housing finance reform in both Congress and the Administration. This week, the Senate Banking Committee (SBC) held two hearings on Chairman Mike Crapo’s (R-ID) Housing Reform Outline, where USMI President Lindsey Johnson appeared as an expert witness on the second day of hearings. Prior to testifying at the hearing, Johnson published a blog on the importance of private mortgage insurance (MI) to borrowers and taxpayers in any reformed housing finance system. On the other side of Capitol Hill, House Financial Services Committee (HFSC) Chairwoman Maxine Waters (D-CA) announced the Committee’s hearings for the first two weeks of April, several of which will address affordable housing. On Pennsylvania Avenue, President Donald Trump signed a memorandum initiating housing reform in the housing finance system. There were also developments at the Federal Housing Administration (FHA) and Fannie Mae and Freddie Mac (the GSEs). The FHA told lenders this month that it is tightening standards on government-backed mortgages due to concerns of increasingly risky loans, while the GSEs both appointed new chief executive officers.

USMI’s President testifies before the Senate Banking Committee. This week, the SBC held two hearings to discuss Chairman Crapo’s Housing Reform Outline. USMI President Lindsey Johnson testified before the committee on the second day of hearings, addressing the Chairman’s Outline and discussing the role private MI can play in a reformed housing finance system. USMI’s testimony specifically outlined the consistencies between Chairman Crapo’s Outline and USMI’s own principles, including ensuring access for creditworthy borrowers and all lenders, increasing transparency, and protecting taxpayers. Johnson also made several recommendations before the committee, chief among them that any proposal should rely on loan-level credit enhancement at origination done by entities that can manage mortgage credit risk through all market cycles.

During the hearing, Sen. Doug Jones (D-AL) brought up the issue of down payments and how Americans are in many cases unable to save enough to buy a home, and specifically asked what can be done about the problem and what are models out there for down payment assistance programs. Johnson answered Sen. Jones, saying, “We think that that is an enormous challenge; it’s specifically what our industry is focused on – is bridging that gap between an individual bringing 20 percent to the closing table and actually having access to the conventional market. And you think about the time that it takes for that individual to save that down payment, we’ve tracked that data and we’ve found that it takes two decades for a firefighter, a teacher in many areas to save that up. For minorities, we know that it’s even longer. So, we really have to make sure there are low down payment options available in the market.”

Following Johnson’s remarks, President Elect of the National Association of REALTORS® Vince Malta also noted the importance of MI, stating, “There are vehicles out there that can assist with lower down payment loans that are working very well in the marketplace, a combination of private capital through MI and sound underwriting standards. Those are the guides to homeownership.” The hearings demonstrated a near universal opposition to recapitalizing and releasing the GSEs, an action that Sen. Mark Warner (D-VA) characterized as “recreat[ing] the old status quo and it doesn’t make a lot of sense.” Further, there was broad support among the witnesses for restructuring the GSEs as highly regulated utility-like entities to increase transparency, limit the GSEs’ activities to secondary market functions, and ensure that certain protections—such as equitable pricing for lenders of all sizes and types—are maintained. The full list of witnesses and their testimonies can be found here.

USMI releases blog on importance of MI in the housing finance system. USMI President Lindsey Johnson published a blog this week ahead of the SBC hearings on Chairman Mike Crapo’s Housing Reform Outline that highlights the critical role private MI plays in housing finance reform, with particular emphasis on how private MI benefits homebuyers and protects taxpayers. The blog states that with the recent activity in the housing reform debate, now more than ever private MI will continue to play its invaluable role in providing access to credit and unparalleled taxpayer protection.

President Trump signs memorandum initiating reform of the housing finance system. On March 27, President Trump signed a memorandum calling for relevant agencies to develop a reform plan for the housing finance system. According to the memorandum, these reforms will seek to end the conservatorship of the GSEs and improve regulatory oversight over them, promote competition in the housing finance market, create a system that encourages sustainable homeownership, and protect taxpayers against bailouts. The Secretary of the Treasury Steven Mnuchin and Secretary of Housing and Urban Development Ben Carson will be tasked with addressing their respective issues and are expected to submit reform plans as soon as practicable. In the fall of 2018, USMI released Areas of Alignment for Administrative Reformthat highlighted a number of specific steps the Administration can and should take before allowing the GSEs to build capital and be released from conservatorship. A list of the 11 specific steps can be found here.

House Financial Services Committee Chairwoman releases early April hearing schedule. HFSC Chairwoman Waters published the Committee’s calendar of hearings for the first two week of April, three of which will focus on housing. One of the hearings, entitled “The Fair Housing Act: Reviewing Efforts to Eliminate Discrimination and Promote Opportunity in Housing,” will be with the full committee. The other hearings, one entitled “The Affordable Housing Crisis in Rural America: Assessing the Federal Response” and another entitled “The Community Reinvestment Act: Assessing the Law’s Impact on Discrimination and Redlining,” will be with the Subcommittee on Housing, Community Development and Insurance and Subcommittee on Consumer Protection and Financial Institutions, respectively.

FHA tightens underwriting standards on government-backed mortgages. In an about-face for a 2016 decision, the FHA has decided to tighten its underwriting and lending standards due to concerns that it is allowing too many risky loans to be insured. The FHA has observed extensive risk layering in recent years and this action is intended to ensure the FHA’s financial stability for years to come. According to the Wall Street Journal, the FHA “told lenders this month it would begin flagging more loans as high risk. Those mortgages, many of which are extended to borrowers with low credit scores and high loan payments relative to their incomes, will now go through a more rigorous manual underwriting process…” The FHA stated in its letter that the “announcement comes after Federal Housing Commissioner Montgomery publicly stated numerous times in recent months that FHA must seek the right balance between managing risk and fulfilling its mission of supporting sustainable homeownership.”

Fannie and Freddie announce newly appointed CEOs. Both Fannie Mae and Freddie Mac have announced the appointments of their new CEOs following their individual six-month searches. Fannie Mae appointed as its CEO commercial mortgage executive Hugh Frater, who joined Fannie’s board of directors in 2016 and served as interim CEO for several months after Tim Mayopoulos stepped down in October 2018. Meanwhile, Freddie Mac’s board of directors named its current president David Brickman as its new CEO, succeeding Donald Layton, who will retire in July. Brickman was promoted to president in September 2018 and has been with Freddie Mac since 1999.

The Honorable Mitch McConnell Majority Leader United States Senate S-230, U.S. Capitol Washington, DC, 20510

The Honorable Chuck Schumer Minority Leader United States Senate S-221, U.S. Capitol Washington, DC 20510

Dear Majority Leader McConnell and Leader Schumer:

The undersigned organizations, representing a wide range of perspectives in the housing and mortgage finance industry, write to strongly encourage the confirmation of Dr. Mark Calabria as Director of the Federal Housing Finance Agency (FHFA).

A longtime public servant, Dr. Calabria is a respected expert in housing finance with detailed knowledge of the intricacies of the housing and mortgage finance markets. As one of the Congressional staffers who helped craft the Housing and Economic Recovery Act of 2008, Dr. Calabria has demonstrated a keen understanding of the critical role of the FHFA as both regulator and conservator of Fannie Mae and Freddie Mac (the “Enterprises”). Additionally, through his experience as a staffer on the U.S. Senate Committee on Banking, Housing, and Urban Affairs, and at the National Association of REALTORS®, National Association of Home Builders, and the U.S. Department of Housing and Urban Development, Dr. Calabria understands the need for FHFA to be transparent and methodical in its development and enforcement of policies.

The FHFA has an incredibly important mission of ensuring for a liquid and robust mortgage market, while regulating the Enterprises and their $5.4 trillion in mortgage credit risk, along with the Federal Home Loan Bank system.1 It is critical for the Senate to proceed expeditiously to confirm a permanent Director at the FHFA in order to best promote an efficient national secondary mortgage market that facilitates access to affordable mortgage financing for all creditworthy borrowers during all market conditions. Dr. Calabria recognizes the need to balance this mission with the protection of taxpayers from mortgage credit risk while avoiding market disruptions when improving and implementing policy. Any new Director should also maintain increased transparency with essential public feedback to guarantee that any potential changes are in the best interests of consumers, the supporting industries, and the overall economy.

Dr. Calabria has a deep understanding of the secondary mortgage market and the complex policy issues that affect the entities the FHFA oversees. Dr. Calabria’s decades of experience in the public and private sectors have prepared him to execute the duties of Director and address the agency’s mission and significant regulatory priorities.

We respectfully request the swift confirmation of Dr. Calabria as Director of the FHFA to protect and ensure the continuation of a strong real estate market and overall economy.

Sincerely,

American Academy of Housing and Communities American Land Title Association (ALTA) The Commercial Real Estate Finance Council (CREFC) Community Associations Institute Consumer Mortgage Coalition Leading Builders of America Make Room Manufactured Housing Association for Regulatory Reform (MHARR) Manufactured Housing Institute Mortgage Bankers Association Nareit National Affordable Housing Management Association The National Apartment Association National Association of Home Builders The National Association of Housing Cooperatives National Association of REALTORS® National Council of State Housing Agencies National Leased Housing Association National Multifamily Housing Council The Real Estate Roundtable Real Estate Services Providers Council, Inc. (RESPRO) The Realty Alliance U.S. Mortgage Insurers

The year 2019 is already shaping up to be significant for the debate on the future of the housing finance system. With the Administration’s pick for Federal Housing Finance Agency (FHFA) Director Mark Calabria likely to be confirmed in the coming weeks, there has been a renewed focus on the futures of Fannie Mae and Freddie Mac (the GSEs) and the need for reforms. Just last month, Senate Banking Committee Chairman Mike Crapo (R-ID) released an outline on housing finance reform. House Financial Services Committee Chairwoman Maxine Waters (D-CA) has also detailed her legislative priorities, which includes housing reform and a particular focus on affordable housing issues. U.S. Mortgage Insurers (USMI) agrees with Chairman Crapo, Chairwoman Waters, and other policymakers who continue to see the need for meaningful reforms to address structural concerns at the GSEs. While the Administration can take steps to provide the necessary oversight of and enhancements to the GSEs, structural reform must be done by Congress.

This week, I will join other witnesses to testify on behalf of USMI on Chairman Crapo’s outline for housing finance reform and will specifically highlight the important role that private mortgage insurance (MI) plays each day to help middle-income and first-time buyers to become homeowners despite modest down payments. Not only does private MI help to provide access to mortgage credit for American homebuyers, but it also provides important protections for the overall mortgage finance system, which translates to protections for the federal government and taxpayers. Here is why private MI serves a valuable role.

MI Helps Low Down Payment Homebuyers

Private MI is a time-tested way to help borrowers qualify for low down-payment home financing. Research by the National Association of REALTORS® shows that Americans continuously cite saving for a down payment as one of the biggest hurdles for attaining homeownership and first-time homebuyers on average have a down payment of seven percent. Private MI helps bridge the gap for many borrowers to attain homeownership sooner than they otherwise would. In fact, for the past three years, private MI has been the leader in the total insured market to provide borrowers with to access to low down payment mortgage financing. All told, for over 60 years private MI has helped nearly 30 million families nationally purchase or refinance a home, with more than one million borrowers alone in 2018. Of those borrowers, nearly 60 percent of purchase loans went to first-time homebuyers and more than 40 percent of borrowers with MI had annual incomes below $75,000.

MI Protects Taxpayers and Government from Risk

Private MI not only provides affordable access to credit for homebuyers, but it also plays a critical role in protecting U.S. taxpayers from mortgage credit risk in the event of borrower defaults. Private MI serves as the first layer of protection in the conventional mortgage market against defaults that may occur on GSE-purchased mortgages. Private MI attaches to a loan the day that the loan is originated, which means that even before the lender might sell the mortgage into the GSE-backed secondary market, it is protected by private capital and therefore doesn’t directly expose the government. In this regard, when it comes to insuring low down payment mortgages, MI serves as a “second pair of eyes” on that risk. This helps ensure borrowers are placed into sustainable homeownership and adds an additional layer of protection in the mortgage finance system. This loan-level credit enhancement that attaches to the loan at origination is a feature that should be maintained in a future housing finance system.

Mortgage insurers have strong incentives to actively manage this mortgage credit risk because when a conventional-insured mortgage defaults, private MI bears the first layer of financial loss (on average 25 percent of the mortgage value). This structure of MI protection has been effective and, according to the Urban Institute, for GSE “30-year fixed rate, fully documented, fully amortizing mortgages, the loss severity of loans with private MI is 40 percent lower than that without, despite the higher Loan-to-Value of mortgages with private MI.”

It’s been over 10 years since the 2008 financial crisis, which prompted the federal government to place the GSEs into conservatorship. Comprehensive housing finance reform is long overdue and as Congress and the Administration move forward with this important work, private MI looks forward to continuing to play its invaluable role in providing access to credit and unparalleled taxpayer protection.