It’s hard to believe there’s only 15 days until the first day of Spring 2021—a time that marks, for most years, the start of the busiest homebuying season. As the Biden Administration has filled more of its key positions, policymakers and industry leaders continue to focus on top priorities, including COVID-19 and its impact on many borrowers and the housing market, as well as ways to address racial and economic disparities in mortgage lending to ensure homeownership is an achievable goal for all Americans through thoughtful rulemakings and targeted polices. Below are some of the key developments U.S. Mortgage Insurers (USMI) has been following over the last month.

USMI Highlights Industry Leaders in Honor of Black History Month

USMI Member Spotlight: Radian

COVID Stimulus Bill Provides Housing Support

CFPB Delays QM Rule Implementation

Senate Banking Committee Holds Hearing on CFPB Director Nominee

Government Agencies Extend Forbearance & Foreclosure Protections

USMI Submits Comments to FHFA on Appraisal Policies

What We’re Listening To: Natixis Podcast

What We’re Reading: Brookings on GSE Reform

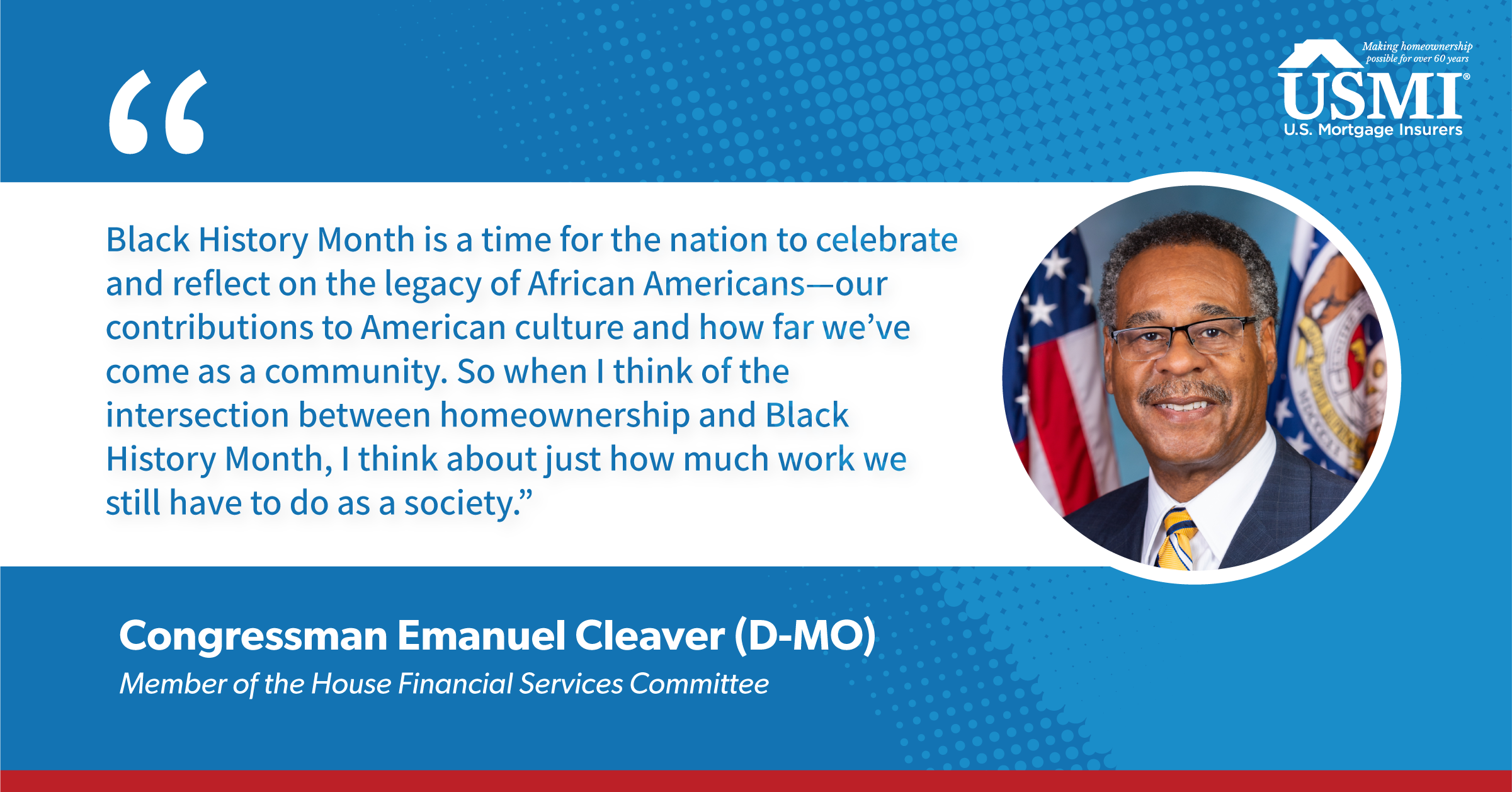

- USMI Highlights Industry Leaders in Honor of Black History Month. In February, USMI reached out to prominent leaders in the housing finance industry to discuss their work and perspectives on the goal of increasing Black homeownership in America. USMI spoke with Congressman Emanuel Cleaver (D-MO), chair of the House Committee on Financial Services’ Subcommittee on Housing, Community Development, and Insurance; Phyllis Caldwell, former Chief of the Homeownership Preservation Office at the U.S. Department of the Treasury; Lisa Rice, President and CEO of the National Fair Housing Alliance; and Alanna McCargo, Senior Advisor for Housing Finance at the U.S. Department of Housing and Development (HUD). Each of these leaders offered insights on the housing industry and how policymakers can work to help close the racial homeownership gap. USMI is grateful for their leadership and looks forward to continuing to work with them to expand Black homeownership and build wealth.

- USMI Member Spotlight: Radian. In February, USMI began a new blog series to spotlight its members every couple of months and highlight how the industry is working to address critical issues within the housing finance system. Topics include expanding access to affordable and sustainable homeownership opportunities, ensuring taxpayer protection through increased capacity for risk sharing with mortgage insurance (MI), and providing recommendations for a coordinated federal housing policy. USMI kicked off the series with Derek Brummer, President of Radian’s Mortgage Business and Chairman of USMI’s Board. In the interview, Brummer emphasized Radian’s commitment to “the American dream of homeownership responsibly and sustainably through products and services that span the mortgage and real estate spectrum.” He noted the key role MI plays in bridging the down payment gap, and the benefits borrowers receive from having access to low down payment mortgages in the conventional market backed by private MI rather than being limited to mortgages backed by the Federal Housing Administration (FHA). “Optionality is a key component of affordability and accessibility,” he remarked.

He also discussed the future of housing policy, touching on President Biden’s executive order to address racial equity through housing, the nomination of Marcia Fudge to serve as the next HUD Secretary, and the opportunities for policymakers to increase Black homeownership and access to affordable mortgage credit. Brummer said, “Policymakers and the housing industry have the opportunity to correct inequities and sustainably increase minority homeownership.” Read the full interview here.

- COVID Stimulus Bill Provides Housing Support. In the early hours of February 27, the House passed H.R. 1319, the American Rescue Plan Act of 2021, in a 219-212 vote. The $1.9 trillion aid package includes a significant amount of housing aid—$30 billion in emergency rental assistance, $10 billion for a Homeowner Assistance Fund, $100 million for housing counseling services, $20 million for fair housing initiatives, and several programs for the homeless. The bill is now in the Senate where it has already been subject to numerous modifications, including the elimination of the minimum wage increase due to the “Byrd Rule,” and more targeted direct payments to Americans. Earlier this year, USMI joined with several consumer and industry groups in sending letters to President Biden and congressional leadership urging them to include direct homeowner assistance in a COVID-19 relief bill to help families who are at risk of losing their homes due to the economic fallout from the pandemic. Click here to read more about USMI’s policy priorities to expand access and affordability in housing.

- CFPB Delays QM Rule Implementation. On March 3, the Consumer Financial Protection Bureau (CFPB) released a notice of proposed rulemaking (NPRM) to delay the planned July 1 mandatory compliance date for the December 2020 General Qualified Mortgage (QM) Final Rule by 15 months to October 1, 2022. The CFPB is accepting comments until April 5. If finalized, the NPRM would allow for mortgages whose applications were received by lenders prior to October 1, 2022 to receive QM status using any of the following three standards: (1) the 2013 General QM definition that relied on a debt-to-income (DTI) cutoff; (2) the 2020 price-based General QM definition; (3) or the government sponsored enterprises (GSEs) Patch (so long as the GSEs remain in conservatorship). The CFPB noted it “believes that an extension of the mandatory compliance date may help to ensure stability and access to affordable, responsible credit in the mortgage market.”

The CFPB previously announced on February 23 that it is considering whether to revisit the December 2020 General QM and Seasoned QM Final Rules. The first replaced the 43 percent DTI ratio QM standard with a price-based definition and the second created a new QM category based on loan seasoning. Should the CFPB reevaluate aspects of the General QM definition, it could decide to modify the thresholds for Safe Harbor (Average Prime Offer Rate, or APOR, + 150 basis points, or bps) and Rebuttable Presumption (APOR + 225 bps). USMI, along with consumer groups and other industry organizations, has repeatedly urged the CFPB to increase the Safe Harbor threshold to APOR + 200 bps to best level the playing field across the mortgage market and ensure minority, low-income, and first-time homebuyers continue to have access to affordable and safe conventional mortgages.

- Senate Banking Committee Holds Hearing On CFPB Director Nominee. On March 2, Rohit Chopra, President Biden’s nominee for CFPB Director, testified before the Senate Banking Committee. In his written testimony, Chopra highlighted the ongoing challenges facing Americans in the housing sector due to the impacts of COVID-19 and suggested opportunities for reform in the mortgage market. He said that “fair and effective oversight” in the market could promote a “resilient and competitive financial sector,” while also addressing the systemic inequities faced by families of color. He also said, “administration of consumer protection laws can help families navigate their options to save their homes.”

In response to questions from Senator Jon Tester (D-MT), Chopra stated that “the CFPB is not here to dictate housing finance policy, it’s to make sure that the prohibitions when it comes to our mortgage laws are adhered to. And when it comes to QM it is important that we balance the consumer protections that Congress has put into place with access to mortgages.”

- Government Agencies Extend Forbearance & Foreclosure Protections. On February 16, President Biden announced the extension of COVID-19 forbearance and foreclosure protections for homeowners with government-backed mortgages through June 30. This included expanding COVID-19 forbearance to allow for up to 2-3 month extensions for homeowners who requested a forbearance on or before June 30. The administration outlined its priorities to extend protections as providing immediate relief to homeowners across America, supporting hard-hit communities of color, and providing a centralized resource for housing assistance.

The Federal Housing Finance Agency (FHFA) followed suit February 25 and announced extensions of COVID-19 relief for single-family mortgages guaranteed by the GSEs, Fannie Mae and Freddie Mac. This included extending the moratorium on foreclosures and real estate owned evictions through June 30 and expanding the maximum forbearance period to 18 months for borrowers with active COVID-19 forbearance plans as of February 28. FHFA Director Mark Calabria stated that “[f]rom the start of the pandemic, FHFA has worked to keep families safe and in their home, while ensuring the mortgage market functions as efficiently as possible. Today’s extensions of the COVID-19 forbearance period to 18 months and foreclosure and eviction moratoriums through the end of June will help align mortgage policies across the federal government.”

- USMI Submits Comments to FHFA on Appraisal Policies. On February 26, USMI submitted a comment letter to FHFA providing feedback on initiatives to modernize appraisal processes and answer specific questions in the agency’s Request for Information (RFI) on Appraisal-Related Policies, Practices, and Processes. USMI wrote that “FHFA should implement rules designed to ensure that innovations around the appraisal process are done when there is demonstrable benefit to the broader housing finance system, including greater transparency, efficiency, accuracy of property valuations, and lower costs for borrowers and market participants.” USMI also emphasized that attention should be given to the expansion of appraisal waivers, particularly for the 80 percent loan-to-value (LTV) market, where “appraisal waivers can materially impact LTV ratios, the pricing and risk assessments associated with the GSEs’ guarantee fees, MI premiums, and loan-level capital requirements.” USMI noted that these considerations are “more acute for higher LTV loans since the margin of error is slim for these mortgages and could expose the GSEs and the housing finance system to greater credit risk.”

- What We’re Listening To: Natixis Podcast. USMI President Lindsey Johnson spoke with Natixis Investment Managers’ Vice President of Government Relations Susan R. Olson on the Natixis Insights podcast. They discussed housing finance reform and possible changes under the Biden administration.

- What We’re Reading: Brookings on GSE Reform. The Brookings Institution published a new report titled, “Government-sponsored enterprises at the crossroads: The value of the Treasury’s interest in the GSEs should be used to increase affordable housing and advance racial equity, and the GSEs should be regulated as utilities.” Authored by Michael Calhoun, President of the Center for Responsible Lending, and Lewis Ranieri, Chairman and CEO of Ranieri Solutions, who assert that “[a] utility structure should be implemented permanently in order to secure the GSEs as an emergency backstop during a crisis, enhance operation of the GSEs in regular times, and advance the GSEs’ public mission.”