As the end of 2020 approaches, U.S. Mortgage Insurers (USMI) want to recognize and thank everyone who has worked to support homeowners and the U.S. housing finance system during a year full of unprecedented challenges. This past year has also ushered in significant federal regulatory and policy proposals and changes, and below are some of the key developments that we are following late this year. In 2021, USMI looks forward to working with policy makers and others to support a housing finance system that creates homeownership opportunities backed by private capital for more Americans.

FHFA Issues Final Capital Rule. On November 18, the Federal Housing Finance Agency (FHFA) released its final rule on the Enterprise Regulatory Capital Framework (ERCF) outlining post-conservatorship capital requirements for the government sponsored entities (GSEs), Fannie Mae and Freddie Mac. The GSEs will collectively be required to hold $284 billion in capital, representing approximately $20 billion more than was outlined in the 2020 proposed rule and more than $100 billion than the 2018 proposal. FHFA Director Mark Calabria said the ERCF “puts Fannie Mae and Freddie Mac on a path toward a sound capital footing” and it is “another milestone necessary for responsibly ending the conservatorships.” While appropriate capital standards for the GSEs is a critical reform, USMI continues to urge FHFA to implement additional reforms necessary to put the housing finance system on a more stable footing. It is essential for these reforms to occur before the GSEs are released from conservatorship in order to strengthen the housing finance system and ensure that the GSEs’ operations comply with their congressional charters.

Many organizations commented that the capital rule is an essential component of reforming the nation’s housing finance system, though several housing groups and policymakers also expressed concern about the impact of the final rule on consumers’ cost and access to mortgage finance credit. The Center for Responsible Lending said the final rule “places the burden of future catastrophic risk on the backs of these hardworking families and will unnecessarily raise the cost of mortgages for all borrowers, resulting in limited credit availability.” It added, “the rule pushes homeownership farther away from families of color long denied mortgage credit access.” Similarly, the National Association of REALTORS® also raised concerns about the impact of the rule on the cost of mortgage finance credit. Sen. Sherrod Brown (D-OH), ranking member of the U.S. Senate Committee on Banking, Housing, and Urban Affairs, wrote in a statement that “the GSEs help millions fulfill the dream of homeownership – especially those living in underserved rural and urban areas. Director Calabria’s rush to finish this rule without addressing concerns raised about its effects is a recipe for disaster and is patently unfair to America’s homeowners and renters.”

The final rule goes into effect 60 days after it is published in the Federal Register.

Treasury Secretary Mnuchin Testifies Before Congress—Fields Questions on Possible GSE Exit from Conservatorship. On December 1 and 2, Treasury Secretary Steven Mnuchin testified before the Senate Banking Committee and the House Financial Services Committee (HFSC), respectively. While both hearings focused on the Treasury Department’s response to the COVID-19 crisis and its implementation of the CARES Act programs and relief, Secretary Mnuchin also addressed the GSEs’ possible exit from conservatorship.

Senators on both sides of the aisle expressed concern regarding an exit from conservatorship for the GSEs. Senator Mike Round (R-SD) noted that in “a perfect world that conservatorship should have been ended some time ago,” but voiced his concern that releasing the GSEs too early would call into question the strength of the housing sector and asked Secretary Mnuchin about an appropriate timeline. Secretary Mnuchin reiterated the importance of the GSEs having “appropriate capital” levels before being released and emphasized that the Treasury Department has made “no decisions” on this matter. The Secretary also fielded similar questions and concerns from lawmakers when he appeared before the HFSC the next day. Among those that raised objections to the GSEs’ exit from conservatorship was HFSC Chairwoman Maxine Waters (D-CA), who expressed concerns that the Treasury Department is working with the FHFA to “rush” the GSEs out of conservatorship.

In a December 10 blog post, the American Action Forum (AAF) opined on the parameters of consent orders for the GSEs and the need for additional actions to ringfence Fannie and Freddie. AAF President Doug Holtz-Eakin wrote, “The GSEs are notorious for sidestepping caps on compensation, lobbying bans, accounting standards, and more. Capital accumulation is the easy part. A really tight leash would require a consent decree specifying in great detail the management and operation of the GSEs, and with sufficient foresight to anticipate the condition that will prevail in future housing and financial markets.”

In a blog post released in recent weeks, USMI outlined key reforms that should occur, especially ahead of the possible release of the GSEs from conservatorship.

House Financial Services Chairwoman Waters Sends Letter to President-Elect Biden. Last week, Chairwoman Waters sent a letter to President-elect Joe Biden and his transition team detailing recommendations to immediately reverse several of the actions by the Trump Administration that fall within the HFSC’s jurisdiction, including changes to the Consumer Financial Protection Bureau’s (CFPB) rulemaking and enforcement activities, as well as enhancements for oversight of Wall Street. Chairwoman Waters also called on President-elect Biden to issue an order preventing evictions and to promote stable housing during the pandemic. Key housing regulations in the letter include FHFA’s Enterprise Regulatory Capital Framework, which Chairwoman Waters said should be rescinded and also the CFPB’s General Qualified Mortgage rulemaking, which the Chairwoman recommended be paused until “various options can be thoroughly analyzed examining the potential impact for access to credit and consumer protections.”

More broadly, Chairwoman Waters called on President-elect Biden to support affordable housing by addressing homelessness, promoting housing affordability, and fair housing regulations. The Chairwoman detailed a full list of policy recommendations for the Biden Administration, which can be found here.

Changes in FHFA Leadership. FHFA announced that Principal Deputy Director Adolfo Marzol plans to retire on December 18, 2020. Director Calabria praised Marzol for his work at FHFA, specifically his leadership to “spearhead the Enterprise capital rule” and his “central role in the response to COVID-19.” Chris Bosland, FHFA’s Senior Advisor for Regulation, will succeed Marzol as the Principal Deputy Director.

FHA Issues New Loan Limits and Commissioner Dana Wade Reacts. On December 2, the Federal Housing Administration (FHA) released its 2021 Nationwide Forward Mortgage Limits. The new national conforming limit is $548,250 for a one-unit property. The FHA’s low-cost area limit for a single unit property will increase to $356,362, or 65% of the new confirming mortgage limit. However, in high-cost areas, the new loan limit is $822,375, or 150% of the 2021 conforming loan limit. This is the fifth year in a row that the FHA has increased the floor limits. FHA Commissioner Dana Wade expressed concern about the increase stating, “FHA has seen consistent increases in loan limits during the past few years, putting it in a position to serve a segment of borrowers that may be better-served by the conventional market.” Wade continued, “FHA’s mission is to support low-to-moderate income borrowers, so why does the law permit FHA to insure mortgages up to $822,375? This is a question for Congress and the taxpayers who stand behind FHA to answer.”

What We Are Reading:Forbes published an article titled, “4 Ways To Get A Low-Down-Payment Mortgage Without An FHA Loan.” The article noted one of the main benefits of private mortgage insurance (PMI) over government-backed loans: “You can cancel [PMI] once you have 20% equity. With an FHA loan, you would have to pay monthly mortgage insurance premiums for at least 11 years, if not for the life of the loan.”

WASHINGTON— Lindsey Johnson, President of the U.S. Mortgage Insurers (USMI), released the following statement on the Federal Housing Administration’s (FHA) release of its Fiscal Year 2020 Annual Report to Congress on the financial status of the Mutual Mortgage Insurance Fund (MMIF):

“Today’s report shows that the MMIF’s combined capital ratio stands at 6.10 percent, up from 4.84 percent last year, well above the statutory requirement of 2 percent. We applaud the FHA’s steadfast commitment to improving the fiscal health of the fund especially during these challenging times. The FHA continues to play an important role in the housing finance system, and we commend its ongoing collaboration with industry efforts to stabilize the market amidst the COVID-19 pandemic.

“The FHA is a vital part of the housing finance system and it must continue to focus on enhancing its financial strength to best serve the borrowers who need it the most. This is especially important for the FHA in a post-pandemic environment to ensure the agency does not unnecessarily expose taxpayers to undue mortgage credit risk. While some have called for the FHA to reduce its mortgage insurance premiums, the report makes it clear that this is unnecessary and imprudent at this time as consumers continue to have access to low cost mortgage credit. A reduction would diminish the MMIF’s ability to withstand potential stress caused by the economic fallout from the pandemic, evidenced in the nearly 11.6 percent of FHA-insured mortgages that are classified as seriously delinquent. Further, calls to end the premiums for the life of FHA loans are just a veiled way of reducing premiums. Such a move would jeopardize FHA’s ability to serve the borrowers who rely on its insurance today, and borrowers in the future who may need FHA to access homeownership. Now, more than ever, is the time for the FHA to sustain its financial health and focus on its core mission — to serve borrowers the conventional market is unable to adequately serve.

“USMI and our member companies look forward to continuing to work with FHA and Congress to foster a robust housing finance system that meets the needs of low down payment borrowers while protecting taxpayers. To this end, it is essential that federal policymakers advance a coordinated housing policy to best balance consumers’ access to affordable mortgage finance and prudent management of mortgage credit risk.”

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

October has been a busy month in housing finance. Last week, USMI issued a new report on the strength and resiliency of the private mortgage insurance (MI) industry. The report highlights regulatory and industry-led reforms since the 2008 financial crisis which have enabled it to better serve homebuyers and lenders. It also continued to urge the Federal Housing Finance Agency (FHFA) to develop policies for the government sponsored enterprises (GSEs), Fannie Mae and Freddie Mac, to promote a more stable and equitable housing finance system post-conservatorship. While all eyes are on the election this week, below are other important issues USMI is tracking:

New USMI Report Released on MI Industry. Last week, USMI released a new report titled, “Private Mortgage Insurance: Stronger and More Resilient.” The report highlights significant regulatory and industry-led reforms taken since the 2008 financial crisis to improve and strengthen the role of private MI in the nation’s housing finance system. It analyzes the various steps the industry and regulators have undertaken and continue to take to ensure sustainable mortgage credit through all market cycles and to better serve low down payment borrowers in the conventional market, especially during critical economic times like these.

Upon the report’s release, USMI President Lindsey Johnson said, “Though private mortgage insurers have been a crucial part of the housing finance system for more than 60 years, this is definitely ‘not your father’s’ MI industry. Enhanced capital and operational standards, as well as increased active management of mortgage credit risk, including through the distribution of credit risk to the global reinsurance and capital markets, has put the industry in a stronger position.” She added, “These enhancements will enable the industry to be a more stabilizing force through different housing cycles — including the current COVID-19 crisis — which greatly benefits the GSEs and taxpayers and enhances the conventional mortgage finance system.”

The report details several of the major enhancements to the industry in the last decade, including: Private Mortgage Insurer Eligibility Requirements (PMIERs); New Master Policy; Rescission Relief Principles; and MI Credit Risk Transfer (MI-CRT) Structures. The report provides an update on the growing MI-CRT market, noting that as of October 2020, private MI companies have transferred nearly $41.4 billion in risk on approximately $1.8 trillion of insurance-in-force (IIF) since 2015 using 23 reinsurance deals and 30 insurance-linked note (ILN) transactions.

USMI Blog on FHFA Re-Proposed ERCF and Strategic Plan. This week, USMI published a blog titled, “Capital Alone is Not Comprehensive Housing Finance Reform: More Administrative Actions are Required & FHFA’s Re-Proposed Capital Framework Should be Modified.” The piece emphasizes the importance of the appropriate level of capital for Fannie Mae and Freddie Mac, but also the need for additional reforms prior to the GSEs’ exit from conservatorship. FHFA’s re-proposed ERCF will guide FHFA as it works to release the GSEs from conservatorship. As proposed, the ERCF would require the GSEs to hold about 10 times their current capital levels ($243 billion versus $28 billion, respectively, as of Q2 2020) and roughly five times their projected losses under a severe economic downturn. USMI submitted its comment letter on the re-proposed ERCF in August 2020 and published an executive summary as well.

USMI agrees that a robust and appropriately tailored capital standard for the GSEs is necessary and should strike the right balance to ensure consumers’ continued access to affordable mortgage credit while also protecting taxpayers. However, the ERCF has several overly conservative elements, such as the treatment of private MI and CRT transactions, as well as numerous non-risk adjusted capital buffers. Instead, USMI suggests FHFA should reduce or eliminate non-risk based elements and build the capital rule around an insurance framework, given the GSEs’ core function is a guaranty business. The framework should ultimately ensure adequate capital for the risks taken by the GSEs, but should not be set to an arbitrarily high level that puts homeownership out of reach for many American families.

USMI’s Comments on FHFA’s Strategic Plan. USMI’s blog also discusses USMI’s recommendations for FHFA’s Strategic Plan for Fiscal Years 2021-2024. USMI welcomes FHFA’s work on a post-conservatorship capital framework, but notes that it is important to recognize that capital alone is not comprehensive GSE reform, and additional actions are necessary to reform the housing finance system and put it on more stable footing for the long-term.Earlier this month, USMI submitted a comment letter to FHFA on its Strategic Plan. In its comment, USMI recommended that FHFA take further steps to reduce the GSEs’ risk exposure, level the playing field, and increase transparency around the GSEs’ pricing and business operations. USMI called for FHFA to take five specific actions in advance of the GSEs’ exit from conservatorship:

Limit the GSEs’ activities to those necessary to fulfill their intended role of facilitating a liquid secondary market for mortgages, preserving the “bright line” separation between the primary and secondary mortgage markets;

Increase transparency around the GSEs’ operations, credit decisioning, technologies, and role in the housing finance system;

Require a “notice and comment period” process and prior approval for new products and activities at the GSEs;

Require that counterparty standards be set by or in coordination with FHFA, and not just the GSEs; and

Promote a clear, consistent, and coordinated housing finance system.

FHFA Proposed Rule for New Enterprise Products and Activities. Last week, FHFA released a proposed rule concerning “Prior Approval for Enterprise Products” that would require the GSEs to provide notice to FHFA before undertaking a new activity and obtain prior approval from FHFA before offering a new product. USMI welcomes Director Calabria’s effort to establish a more transparent and objective process for the development and implementation of new GSE products and activities. USMI further believes that the GSEs should only introduce new products, activities, and pilots when there is clear and compelling evidence that the GSEs are needed to fill a market void that the private market cannot meet. This rule would allow a rigorous review of the GSEs’ efforts and ensure that the GSEs’ activities are not duplicative nor unfairly competitive with the primary and private market participants.

In response to the release of the proposed rule, the National Taxpayers Union (NTU) published a blog titled, “Latest GSE Rule Protects Taxpayers and Businesses from Government Overreach.” NTU praised the rule as it would “help to ensure that the GSEs are neither crowding out private market competitors nor expanding obligations back-stopped by taxpayers.” NTU said the proposed rule is a “constructive step that protects taxpayers and private businesses from government overreach.”

Urban Institute Releases October 2020 Chartbook. This week, the Urban Institute published its October chartbook on housing finance. Included in this comprehensive analysis of industry data are updates on the MI industry, beginning on page 32. The Chartbook highlights that “Mortgage insurance activity via the FHA, VA and private insurers increased from $197 billion in Q2 2019 to $327 billion in Q2 2020, a 57.4 percent increase. In the second quarter of 2020, private mortgage insurance written increased by $51.3 billion, FHA increased by $17.2 billion and VA increased by $56.4 billion relative to Q2 2019.”

USMI President on “Main St. Finance” Podcast. USMI’s members work to help low down payment borrowers have access to affordable mortgage credit. To share that message, USMI President Lindsey Johnson joined the “Main St. Finance” podcast to discuss the 20 percent down payment myth and the different low down payment options available to borrowers. Specifically, she explained how private MI bridges the down payment gap to help home-ready buyers get in their home sooner while also protecting lenders, the GSEs, and taxpayers from mortgage credit-related losses. Listen to podcast here.

ICYMI: CFPB Extends GSE Patch. On October 22, the Consumer Financial Protection Bureau (CFPB) issued a final rule to extend the GSE Patch until the CFPB implements a new General Qualified Mortgage (QM) definition. USMI previously submitted a comment letter on the Bureau’s proposed updates to the General QM definition, as well as a comment letter which recommended the CFPB set the sunset date for the GSE Patch to be at least six months after the effective date of the General QM definition final rule.

USMI President Lindsey Johnson appeared on the Main Street Finance podcast and discussed the benefits of private mortgage insurance and how it supports home-ready buyers to get in their home sooner. Listen here.

Since Fannie Mae and Freddie Mac (the “GSEs”) entered conservatorship in 2008, federal policymakers and industry professionals have debated their future role in the housing finance system, as well as what reforms are appropriate and necessary to put the GSEs on stable footing for the long term.

Twelve years later, the Federal Housing Finance Agency (FHFA) is taking steps to release the GSEs from conservatorship. To that end, FHFA has proposed an Enterprise Regulatory Capital Framework (ERCF) intended to prevent future failures by requiring the GSEs to hold much more capital. In fact, the re-proposed ERCF would require the GSEs to hold about 10 times their current capital levels ($243 billion versus $28 billion, respectively, as of Q2 2020) and roughly five times their projected losses under the most severe economic downturn.

Importantly, the proposed framework supposes that the GSEs will return to their pre-conservatorship status in the housing finance system—quasi-government companies—with congressional charters, missions, and mandates, yet private companies with profit objectives. FHFA’s re-proposed capital framework is intended to help the GSEs avoid taxpayer bailouts by building and maintaining large enough capital reserves to withstand future downturns.

USMI agrees that a robust and appropriately tailored capital standard for the GSEs is necessary and should strike the right balance to ensure consumers maintain access to affordable mortgage credit while also protecting taxpayers. The best way to achieve these objectives is to have a standard that reflects the business models of the GSEs, whose primary business is a guaranty business, and that is akin to an insurance framework. Further, the capital framework should be objectively risk-based, and the quantity and quality of capital requirements should be completely transparent and analytically justified.

In its comment letter to FHFA on its 2020 proposed rule, USMI identified key issues with the re-proposed ERCF and provided recommendations for ensuring greater balance between the two aforementioned objectives. (An executive summary of USMI’s observations and recommendations is available here). While actions taken during conservatorship have strengthened the GSEs, it is clear that additional reforms are necessary to improve the GSEs’ operations in advance of their exit from conservatorship. USMI strongly urges FHFA to turn its attention to critical reforms that incentivize the prudent management of mortgage credit risk and ensure access to affordable and sustainable mortgages for home-ready consumers.

INCREASE, NOT DECREASE THE USE OF PRIVATE CAPITAL

Proposed Capital Rule Disincentivizes Critical Loss Protection and Beneficial Risk Transfer

While we support strong GSE balance sheets to best serve borrowers and protect taxpayers from mortgage credit risk, certain elements of the re-proposed rule would promote risk consolidation at the GSEs and disincentivize the distribution of risk. The ERCF should incentivize the increased transfer of mortgage credit risk to private capital where possible. Unfortunately, as many stated in their comment letters to the proposed ERCF, the reduced capital benefit for private mortgage insurance (MI), punitive treatment of credit risk transfers (CRT), and proposed floors on mortgage exposures would likely reduce the GSEs’ ability or willingness to transfer risk to other sources of private capital.

Until Congress enacts comprehensive housing finance reform and/or gives FHFA the authority to charter additional GSEs, it is imperative that the concentration of mortgage credit risk at Fannie Mae and Freddie Mac be transferred to highly regulated counterparties to appropriately underwrite, actively manage and hold capital against. One way FHFA can accomplish this objective is to provide the appropriate capital benefit to the GSEs for transferring risk—based on an historical analysis of the capital credit that should be given to any such counterparty or risk transfer. To ensure that credit risk is transferred to strong counterparties, FHFA—rather than the GSEs—should establish and update robust operational and capital requirements for GSE counterparties, as necessary. Transparent and objective standards will promote a level playing field and ensure that private market participants can perform an important role in de-risking the GSEs. Private MI and the GSEs’ CRT programs are important tools to bring private capital into the housing finance system and any final rule on GSE capital requirements should recognize their risk-reducing benefits.

However, it seems that in addressing some of the structural weaknesses of CRT, the proverbial “baby was thrown out with the bathwater” by the current proposed rule. Instead, to fully assess the weaknesses and determine the appropriate capital relief that the GSEs should receive for different forms of CRT, FHFA should publish a transparent model that capital markets executions and reinsurance transactions can be modeled against. This will ensure that weaknesses are properly addressed but will also maintain integrity and increase transparency and consistency in FHFA and the private market’s assessment of and capital benefit for CRT and will better ensure a viable CRT market going forward.

Balance Capital Requirements with Access to Sustainable Mortgage Finance Credit

Importantly, the re-proposed rule, if implemented in its current form, could push homeownership out of reach for many Americans –particularly minority and first-time homebuyers –or it could leave many borrowers with the lone option of obtaining a mortgage backed by the Federal Housing Administration (FHA). According to the Urban Institute[1] and the GSEs themselves,[2] the capital proposal would result in higher costs for borrowers and less mortgage credit availability, as higher capital requirements would necessitate higher profits to support the capital. For the GSEs, this will mean higher Guarantee Fees (G-Fees), raising the cost of homeownership for millions, with a disproportionate negative impact on lower wealth and traditionally underserved borrowers. In light of these increased costs, many of these borrowers, would migrate to the FHA market.

The proposed ERCF has a number of overly conservative elements, as well as numerous examples of non-risk aspects. Instead, FHFA should reduce or eliminate non-risk based elements and establish the capital rule around an insurance framework, given the GSEs’ core guaranty business is to ensure the adequate capital for the risks taken by the GSEs, but not an arbitrarily high level of capital that puts homeownership out of reach for many American families.

THE NEXT STEPS FOR STRENGTHENING THE HOUSING FINANCE SYSTEM

FHFA’s work on a post-conservatorship capital framework is a welcome development. However, it is important to recognize that capital alone is not comprehensive GSE reform

In order to put the housing finance system on a more sustainable path and to best serve consumers and taxpayers, it is imperative that FHFA implement reforms beyond increasing capital before the GSEs exit conservatorship. In September, FHFA released its “Strategic Plan: Fiscal Years 2021-2024,”outlining goals to fulfill its statutory duties as both regulator and conservator of the GSEs. While a primary goal of the plan is to take actions to support the GSEs’ recapitalization and exit from conservatorship, FHFA invited comments on the “mile markers,” or additional reforms or thresholds to be met by the GSEs and/or FHFA prior to the GSEs’ exit from conservatorship.

It is imperative that FHFA take steps to further reduce the GSEs’ risk exposure, level the playing field, and increase transparency around the GSEs’ pricing and business operations. As recommended in USMI’s comment letter on the Strategic Plan to FHFA, the agency should take the following actions to strengthen the housing finance system prior to the GSEs’ release from conservatorship:

Limit the GSEs’ activities to those necessary to fulfill their intended role of facilitating a liquid secondary market for mortgages, preserving the “bright line” separation between the primary and secondary mortgage markets. Pursuant to their unique congressional charters, the GSEs are required to restrict their activities to secondary market functions. FHFA should implement regulatory guardrails to ensure that the GSEs do not encroach on primary market activities and do not disintermediate private market participants.

Increase transparency around the GSEs’ operations, credit decisioning, technologies, and role in the housing finance system. Absent proper guardrails and transparency for market participants, the GSEs’ innovation can further hardwire their technologies and systems into the housing finance system. Though technology can lead to positive transformation, often these technologies make critical underwriting or credit decisioning less opaque and more centralized in the GSEs. Further, this additional entrenchment complicates the prospects and logistics of enacting permanent structural reforms.

Require a “notice and comment period” process and prior approval for new products and activities at the GSEs. While in conservatorship, the GSEs have rolled out, with little to no transparency, pilots and programs which have often represented expansions into activities long considered to be functions of the primary mortgage market. Recently, FHFA proposed a new rule that would establish a more transparent and objective process for the development and approval of new GSE products and activities. USMI welcomes these efforts and urges FHFA to implement an approval process that facilitates robust feedback from interested stakeholders and ensures that any new products and activities support the GSEs’ explicit public policy objectives, support and do not compete with other market participants on an unlevel playing field, and comply with their charters. While USMI looks forward to reviewing and commenting on all aspects of the proposed rule, it is a much-needed step in the right direction as it relates FHFA’s oversight of the GSEs.

Require that counterparty standards be set by or in coordination with FHFA, and not just the GSEs. FHFA should promulgate strong risk-based capital and operational standards for GSE counterparties, similar to what was established through the development of the Private Mortgage Insurers Eligibility Requirements (PMIERs). Greater transparency and oversight of the GSEs and their counterparties should be conducted in a manner to increase transparency, reduce conflicts of interest, and to ensure the GSEs cannot arbitrarily pick winners and losers or promote opportunities to arbitrage the rules.

Promote a clear, consistent, and coordinated housing finance system. It is paramount for FHFA to work with other federal regulators, including the U.S. Department of Housing and Urban Development (HUD) and Consumer Financial Protection Bureau (CFPB), to reduce—not merely shift—credit risk in the housing finance system. A coordinated and clearly articulated federal housing policy will ensure that American consumers are best served by housing market participants and that the federal government is adequately protected from mortgage credit risk related losses.

Over 10 Years of Reforms and Continued Evolution Make Private Mortgage Insurers Stronger and More Resilient

Industry has facilitated affordable, low down payment mortgages for over 33 million households, contributing to a more stable housing finance market

WASHINGTON — U.S. Mortgage Insurers (USMI), the association representing the nation’s leading private mortgage insurance (MI) companies, today released a report that highlights the many regulatory and industry-led reforms taken since the 2008 financial crisis to improve and strengthen the role of private MI in the nation’s housing finance system. The report, “Private Mortgage Insurance: Stronger and More Resilient,” analyzes the various steps the industry and regulators undertook and continue to take to ensure sustainable mortgage credit through all market cycles and to better serve low down payment borrowers in the conventional market, especially during critical times such as the present.

“Though private mortgage insurers have been a crucial part of the housing finance system for more than 60 years, this is definitely ‘not your father’s’ MI industry. Enhanced capital and operational standards, as well as increased active management of mortgage credit risk, including through the distribution of credit risk to the global reinsurance and capital markets, has put the industry in a stronger position,” said Lindsey Johnson, President of USMI. “These enhancements will enable the industry to be a more stabilizing force through different housing cycles — including the current COVID-19 crisis — which greatly benefits the GSEs and taxpayers and enhances the conventional mortgage finance system.”

The report also highlights the steps the industry has taken since the beginning of the pandemic to support the federal government foreclosure prevention programs, including the announcements made by Fannie Mae and Freddie Mac regarding forbearance programs and other mortgage relief available to support borrowers impacted by COVID-19. USMI members have focused their efforts on helping borrowers remain in their homes by supporting their lender customers during these challenging times.

Among the enhancements to the industry in the last several years, the report outlines and analyzes the following:

Private Mortgage Insurer Eligibility Requirements (PMIERs) – Adopted in 2015 and updated in 2018 and 2020, PMIERs nearly doubled the amount of capital each mortgage insurer is required to hold. USMI members collectively hold more than $5.1 billion in excess of these requirements.

New Master Policy – Updated terms and conditions from mortgage insurers for lenders, which provide lenders with greater clarity pertaining to coverage.

Rescission Relief Principles – First published in 2013 and updated in 2017, these principles allow MIs to offer day-one certainty to lenders of coverage, including automatic relief after 36 timely payments.

MI Credit Risk Transfer (MI-CRT) Structures – Private MI companies have transferred $41.4 billion in risk on over $1.8 trillion of insurance- in-force (IIF) since 2015—through both reinsurance and insurance-linked notes.

Through the programmatic execution of MI-CRT transactions, the industry continues to transition the business into an aggregate-manage and distribute model for mortgage credit risk. The implementation and expansion of MI-CRT programs have demonstrated the industry’s ability to tap multiple sources of capital to support new business and actively manage and distribute risk.

Since 1957, the MI industry has served the U.S. government and taxpayers as an effective and resilient form of private capital, standing as the first layer of protection against risk and mortgage defaults. Importantly, MI has enabled affordable, low down payment homeownership for more than 33 million people. In 2019 alone, more than 1.3 million borrowers purchased or refinanced a loan with private MI, accounting for nearly $385 billion in new mortgages.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org

Dr. Mark A. Calabria Director Federal Housing Finance Agency Constitution Center 400 7th Street SW Washington, DC 20219

Dear Director Calabria:

U.S. Mortgage Insurers (USMI) represents America’s leading providers of private mortgage insurance (MI) and our members are dedicated to a strong housing finance system backed by private capital that enables access to prudent and sustainable mortgage finance. The MI industry has more than 60 years of expertise in underwriting and actively managing mortgage credit risk to balance access to affordable credit with protecting Fannie Mae and Freddie Mac (the GSEs) and the American taxpayer from mortgage credit-related losses. During that time, the MI industry helped more than 33 million households achieve sustainable homeownership, including more than 1.3 million in the past year alone.

On September 22, 2020 the Federal Housing Finance Agency (FHFA) released its “Strategic Plan: Fiscal Years 2021-2024” (Strategic Plan) that establishes goals for FHFA to fulfill its statutory duties as both regulator and conservator of the GSEs. USMI appreciates the opportunity to submit input on the Strategic Plan and provide feedback on the framework and requirements for forthcoming FHFA actions. At a high level, USMI commends FHFA for formalizing the establishment of its new strategic goals to: (1) ensure safe and sound regulated entities through world-class supervision; (2) foster competitive, liquid, efficient, and resilient (CLEAR) national housing finance markets; and (3) position the FHFA as a model of operational excellence by strengthening its workforce and infrastructure. USMI supports these goals and they are consistent with the observations and recommendations outlined in our October 2018 administrative reform report.

A primary goal of the Strategic Plan is to take actions that strengthen the operations and oversight of the GSEs to support their exit from conservatorship. This is consistent with the Administration’s March 2019 “Memorandum on Federal Housing Finance Reform,” which called on the U.S. Department of the Treasury (Treasury) to develop a plan to “End[] the conservatorships of the GSEs upon the completion of specified reforms” and Treasury’s subsequent “Housing Reform Plan” which stated that “In parallel with recapitalizing the GSEs, FHFA should begin the process of ending the GSEs’ conservatorships.” While it will ultimately fall to Congress to complete the difficult work of making permanent and structural changes to the housing finance system, despite a number of legislative proposals over the past 12 years, Congress has yet to pass comprehensive reform. Though congressional action is still needed to provide for the necessary structural reforms, including a transparent and paid-for explicit guarantee of the GSEs’ mortgage-backed securities, the FHFA and Administration can take certain actions to further reduce taxpayer risk exposure, level the playing field, and provide greater transparency regarding GSE pricing and practices—ultimately to put the GSEs and the housing finance system on more stable footing going forward.

Over the summer, the FHFA re-proposed a post-conservatorship capital framework for the GSEs, which you have routinely characterized as the most important rulemaking that will occur during your time as Director. As indicated in our comment letter, USMI urges FHFA to adopt appropriate capital standards for the GSEs and believes that a well calibrated capital framework is a critical reform. However we also strongly believe that additional reforms are necessary, including reforms that reflect the lessons learned during and since the 2008 financial crisis, reduce the GSEs’ duopolistic market dominance, and create long-term safety and soundness in the housing finance system. These reforms, if done correctly, will help to reduce taxpayer risk exposure and ensure that home-ready Americans continue to have sustainable access to prudent mortgage finance credit. Further, actions taken by the FHFA and Administration should help facilitate, not inhibit, Congress’ ability to complete comprehensive housing finance.

As Director of the FHFA, you have previously indicated that the agency “will continue to engage with Treasury to develop a responsible plan to end the conservatorships—with a clear road map and mile markers—and to adjust the Treasury share agreements accordingly.” We are pleased that there are specific “mile markers” and reforms that will have to be met prior to ending the conservatorships of the GSEs. These reforms and mile markers should be met before the GSEs exit conservatorship and are mostly possible if done by the Director of FHFA in his role as conservator. You have stated on a number of occasions your desire and intent to improve competition in the marketplace with the GSEs, noting that “[c]ompetition lowers prices, improves quality, and drives innovation…and ensure[s] no institution is ‘too big to fail.’” However, even if Congress were to provide FHFA the authority to grant charters to new guarantors, for competition to ever exist in the marketplace, the GSEs’ significant market advantages would have to be addressed. Over the decades—and particularly during their more than 12 years in conservatorship—the GSEs have made significant investments in proprietary systems and technologies that have made the mortgage finance system even more reliant on the GSEs. Addressing these vast advantages and implementing these reforms is necessary ahead of allowing the GSEs to build capital and exit conservatorship, where they would otherwise be able to leverage their existing capital and operational advantages to maintain their market dominance.

During conservatorship, stakeholders across the ideological spectrum have put forth a multitude of proposals and recommendations on housing finance reform. While they differ on various details, the proposals and recommendations have a critical similarity among them—they generally recognize that the GSEs should not be recapitalized and released before certain necessary meaningful reforms are completed and made permanent. Further, these proposals also include many common features for what should be considered “mile markers” to be met in advance of ending the net-worth sweep and ahead of the GSEs retaining capital. To varying degrees, many of the leading legislative and Administrative proposals for GSE reform have leaned on a utility-like secondary mortgage market function for the GSEs to reduce their current duopoly and market power in the mortgage finance system. Nearly all such proposals call for capping the GSEs’ rates of return, limiting their scope of activities to secondary market functions, and providing open and transparent access to the GSEs’ data, pricing, and technologies for private market participants, policymakers, and consumers. As to Congress, recent legislative proposals envision a role for the GSEs in a future housing system with an explicit government guarantee at the security level, call for the GSEs to ensure access for smaller lenders, and include transparent affordable housing requirements. These proposals signify that Congress feels there are critical functions currently imbedded in the GSEs and deems these functions/features necessary in a future housing finance system—either within the GSEs or placed in a separate utility or public exchange.

Ultimately, we believe that any actions taken by the Administration should seek to further four key policy objectives: (1) maintain what works in the current system; (2) further reduce taxpayer risk; (3) level the playing field between the GSEs and private market participants; and (4) provide greater transparency regarding the GSEs’ pricing and business practices. At a minimum, prior to the GSEs’ release from conservatorship, USMI urges FHFA to take the following administrative actions to achieve the above stated policy objectives:

Limit the GSEs’ activities to only those necessary for the GSEs to fulfill their intended role of facilitating a liquid secondary market for mortgages, preserving a bright line separation between primary and secondary market activities.

Objective 2.1 of the Strategic Plan calls on the FHFA to “ensure the activities of the regulated entities stay within the boundaries of their charters and appropriately respond to market events and downturns.” USMI strongly supports policies and supervision that preserve the “bright line” separation between the primary and secondary mortgage markets. It is imperative that the GSEs’ activities be limited to the secondary mortgage market, as stipulated by their congressional charters which explicitly state that their purposes are to “provide stability in the secondary market for residential mortgages; to respond appropriately to the private capital market; to provide ongoing assistance to the secondary market for residential mortgages…; and to promote access to mortgage credit throughout the Nation.” Before the GSEs are released from conservatorship, FHFA should use its authority to implement regulatory guardrails to ensure the GSEs do not encroach on primary market activities and do not disintermediate private market participants. Infringements of the longstanding bright line serve only to increase the GSEs’ market dominance and diminish the role that private capital plays in the housing finance system. For instance, the selection of loan-level credit enhancement has been a function of the primary mortgage market for more than 60 years and it is critical that it remains as such going forward to ensure that a vibrant, competitive private MI market is maintained to benefit taxpayers and consumers, and to prevent greater entrenchment of the GSEs.

Increase transparency around the GSEs’ operations, credit decisioning, technologies, and role in the housing finance system.

Implementing elements of a utility-like secondary market function for the GSEs, including transparency around their data, technology, and pricing, are appropriate guardrails that can help ensure the GSEs’ activities are within the bounds of their charters. Further, initiatives and technologies at the GSEs, such as those that seek to reduce the use of appraisals for purposes of assessing collateral during the underwriting process, can dramatically increase risk in the mortgage finance system if not done with transparency and in collaboration with other market stakeholders. Innovation, without proper guardrails and transparency, can further hardwire the GSEs’ automated underwriting systems (AUSs) into the broader housing finance system and complicate the prospects and logistics of enacting permanent structural reforms.

Require a “notice and comment period” process and prior approval of new products and activities.

During their 12 years in conservatorship, the GSEs have developed and introduced programs, products, and pilots with little to no transparency, often representing expansions into areas of the mortgage finance system considered to be functions of the primary mortgage market. This includes pilots for guaranteeing loans for single-family rentals, financing a select group of large non-banks to support mortgage servicing operations, executing lender risk sharing credit risk transfer (CRT) transactions, and utilizing less regulated and capitalized forms of credit enhancement – Fannie Mae’s “Enterprise-Paid Mortgage Insurance” (EPMI) and Freddie Mac’s “Integrated Mortgage Insurance” (IMAGIN). These pilots were introduced into the market without transparency for stakeholders and without a comment period to receive industry input on both the need for the pilots and recommendations to improve their operations. In some cases, they were only made available to a select group of industry participants—generally at the sole discretion of the GSEs, thereby picking winners and losers among industry participants. More recently, FHFA has directed the GSEs to end some of these pilots, and has indicated it plans to release a Request for Input (RFI) or Notice of Proposed Rulemaking (NPR) regarding the prior approval of new products and programs at the GSEs. USMI strongly supports a regulatory mechanism to exercise greater scrutiny of new GSE activities to ensure they support the GSEs’ explicit public policy objectives and comply with their charters. New products, activities, and pilots should only be allowed when there is clear and compelling evidence that the GSEs are needed to fill a market void that the private market cannot meet. A robust approval process that complies with the Administrative Procedure Act (APA) and provides for input from market participants and stakeholders will help ensure that private capital plays a significant role in the mortgage market and prevent the GSEs from being further entrenched in the housing finance system.

Require that counterparty standards be set by the FHFA.

Objective 2.1 of the Strategic Plan also calls on the FHFA to “establish standards for sellers, servicers, and counterparties to the regulated entities that strengthen the overall function and resiliency of the mortgage markets.” Private MIs are one of the only counterparties that have rigorous capital and operational standards, the Private Mortgage Insurer Eligibility Requirements (PMIERs), set by the GSEs and approved by FHFA, which were finalized through a public comment process. MIs must comply with the PMIERs standards in order to insure loans guaranteed by the GSEs. PMIERs ensure MI counterparty creditworthiness, as well as providing minimum standards for capital, operations, procedures, conflicts of interest, and other controls. USMI supports the FHFA promulgating strong risk-based capital and operational standards for all credit enhancement providers to ensure the availability of first-loss, loan-level credit enhancement across market cycles.

The Administration has an opportunity to promote greater transparency and oversight of the GSEs and their counterparties and to correct what has proven to be at times a conflicting role that the GSEs play by both setting standards for market participants and then competing against these same private market participants. Lenders and other market participants should feel confident that they can access the secondary market on a level playing field with their competitors, based on clear and transparent standards. While diminished under a more utility-like system, there will still be a conflict for the GSEs to set counterparty standards, as there will continue to be opportunities to arbitrage the rules to compete with the private market and/or to pick winners and losers in the marketplace. A further post-conservatorship complication is that the GSEs may not continue to collaborate on PMIERs updates and the existence of two competing eligibility standards could cause market arbitrage opportunities and market distortions. Therefore, FHFA, under its authority and responsibility as regulator, should remain intently engaged in the development and approval of PMIERs. It is also important that the FHFA create transparent and consistent/comparable standards that promote a level playing field across counterparties.

Further, consistent with nearly all other federal financial regulatory regimes, the FHFA as a prudential regulator of the GSEs should supervise the GSEs’ risk management processes and financial health. FHFA should use its regulatory authority whenever possible (as opposed to its authority as conservator) to minimize regulatory arbitrage by having a coordinated and consistent oversight approach.

Promote a clear, consistent, and coordinated housing finance system.

Finally, actions taken by FHFA should increase transparency and consistency, and should reduce, not merely shift, mortgage credit risk in the housing finance system. To accomplish this, the FHFA should work closely with other federal regulators to implement a transparent and coordinated housing policy that facilitates access to credit, promotes prudent mortgage underwriting, and creates a level playing field. Robust coordination between the FHFA, U.S. Department of Housing and Urban Development (HUD), and Consumer Financial Protection Bureau (CFPB) will ensure that borrowers are best served by housing market participants and that the federal government, and therefore American taxpayers, are adequately protected from losses related to mortgage credit risk. Federal policy should clarify which borrowers should be served by the GSE backed market and which are better served by the Federal Housing Administration (FHA). This is consistent with Treasury’s “Housing Reform Plan, which stated that “FHFA and HUD should develop and implement a specific understanding consistent with these defined roles for the GSEs and the FHA so as to avoid duplication of Government support.” Importantly, the GSEs have demonstrated that first-time homebuyers and borrowers with low down payments can effectively be supported by the conventional market. The GSEs and MIs have a long history of facilitating access to affordable and prudently unwritten low down payment mortgages, and conventional loans with private MI have been the preferred option for low down payment borrowers for every year since 2016. These home-ready borrowers should have mortgage options and not be categorically restricted to government-insured programs such as the FHA.

A primary aspect of promoting a coordinated housing finance system is that the Administration, and FHFA specifically, should advance policies that promote borrowers being served by the conventional market, by private capital, where possible. As stated in our comment letter on the re-proposed Enterprise Regulatory Capital Framework, USMI strongly encourages FHFA to promote private capital standing in front of the GSEs, including through loan-level first-loss protection through entities that can actively manage mortgage credit risk, such as private MIs. Further, the Administration could encourage or require these private entities to disperse credit risk, similar to how private MIs currently operate and use the reinsurance and capital markets to further distribute mortgage credit risk to diverse global sources of capital.

A well-functioning housing finance system should provide consistent, affordable credit to borrowers across the nation and through all parts of the credit cycle without putting taxpayers at undue risk. Fixing our nation’s housing finance system and putting it on a sustainable path is the last piece of unfinished business following the 2008 financial crisis. We urge the FHFA and Administration to pursue the reforms enumerated above to ensure greater taxpayer protection and a more level playing field that enables a more transparent housing finance system and promotes sustainable access and affordability.

Sincerely,

Lindsey D. Johnson President U.S. Mortgage Insurers

As Congress returns from the August recess, regulators closed out the public comment periods for two proposed rules that will substantially impact the housing finance system and borrowers’ access to mortgage credit. Though there has been considerable focus on these important rulemakings over the past several months, policymakers, industry stakeholders, and USMI members remain hard at work supporting the housing finance system as we continue to adapt to and navigate the health and economic consequences of the COVID-19 pandemic. Below are the latest happenings from USMI and key topics we are tracking.

USMI Submits Comments to FHFA on Proposed Enterprise Regulatory Capital Framework. On August 31, USMI submitted its comments to the Federal Housing Finance Agency (FHFA) on the re-proposed Enterprise Regulatory Capital Framework (ERCF). In its comments, USMI emphasized the importance of constructing a balanced, transparent, and analytically justified post-conservatorship capital framework for the government sponsored enterprises (GSEs), Fannie Mae and Freddie Mac. USMI President Lindsey Johnson said that “while sufficient levels of capital are important to the sustainable operation of Fannie Mae and Freddie Mac, excessive capital requirements could have a detrimental effect on mortgage availability.” She also added that these excessive capital requirements could, in turn, push mortgage lending outside of the conventional mortgage market.

USMI also called for more transparent and objective treatment of the GSEs’ counterparties, especially private mortgage insurers that already meet a set of rigorous capital and operational requirements known as the Private Mortgage Insurer Eligibility Requirements (PMIERs). In its comment letter, USMI provided the FHFA with detailed analysis to demonstrate that the capital credit for private MI should be increased to be consistent with historical analysis. Similarly, USMI suggested that the proposed rule should encourage, and not discourage, private capital to absorb more risk in front of the GSEs and taxpayers.

A number of other organizations shared similar assessments and recommendations. The Urban Institute said that “the capital requirements on purchase loans should be lower, and more credit should be given to mortgage insurance.” National Taxpayers Union recommended that “[t]he proposed rule should promote, and not disincentivize private capital—including transferring first-loss credit risk through the use of loan level credit enhancement, such as private mortgage [insurance] and through transferring other layers of credit risk through responsible CRT.”

Finally, USMI noted that the revised capital standard is only one element of comprehensive GSE reform, calling on the FHFA to ensure the GSEs are appropriately regulated, maintain their position as market makers, and preserve the bright line separation between the primary and secondary mortgage markets.

USMI’s full comments on the 2020 proposed rule can be found here, an executive summary can be found here, and its comments on the 2018 proposal can be found here.

FHFA Director Calabria Testifies Before House Financial Services. On September 16, FHFA Director Mark Calabria testified before the House Financial Services Committee and provided an overview of the FHFA’s response to the COVID-19 pandemic and the ERCF. A number of members on the Committee focused their comments and questions on the ERCF with Representative Steve Stivers (R-OH) noting in his comments to Director Calabria that in the ERCF “one of the things that doesn’t get credit is MI coverage that’s above the minimum level.” Congressman Stivers and several representatives from both sides of the aisle also shared concerns that the ERCF would negatively impact and inhibit the CRT market. Director Calabria committed to following up with Congressman Stivers to provide additional details on capital credit for greater MI coverage as well as credit for CRT. Additionally, Chairwoman Maxine Waters (D-CA) as well as Representatives Nydia Velazquez (D-NJ), Bill Foster (D-IL), and Alma Adams (D-NC) shared concerns that the capital requirements outlined in the ERCF are excessive and could increase mortgage rates, especially for minority borrowers. Finally, there were a number of questions and comments related to the GSEs’ exit from conservatorship and other reforms that should happen prior to their exit. Representative Ted Budd (R-NC) questioned Director Calabria about the GSEs pilot programs, IMAGIN and EPMI, and asked, “[s]hould a GSE in conservatorship or in any state be permitted to set capital [standards] for counterparties and then compete against them in the primary market?” Director Calabria shared that this is a regulatory issue that was delayed by COVID-19, but that it is an issue the FHFA is committed to resolving.

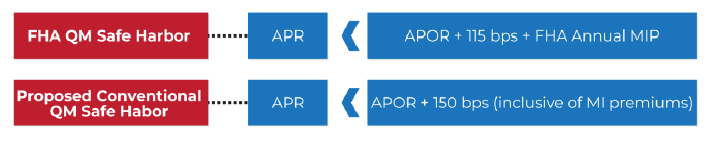

USMI Submits Comments on General Qualified Mortgage Definition. On September 8, USMI submitted comments to the Consumer Financial Protection Bureau (CFPB) for its proposed rule on the General Qualified Mortgage (QM) Definition. USMI urged the Bureau “to strike a proper balance between prudent and transparent underwriting standards, and access to affordable and sustainable mortgage finance credit for home-ready borrowers.” It further noted that the current proposed rule could limit access to the conventional market for traditionally underserved borrowers. In its letter, USMI recommended that the QM Safe Harbor should be set at 200 basis points (bps) above the Average Prime Offer Rate (APOR) to ensure the QM definition does not inadvertently limit access to credit for home-ready borrowers, particularly Black and Hispanic borrowers who are twice as likely to have spreads above the proposed 150 bps Safe Harbor threshold.

USMI also agreed with the Bureau’s assessment that a hard 43 percent debt-to-income (DTI) ratio would be the most harmful option for the General QM definition because it would severely limit access to credit in the conventional market. This assessment was consistent with USMI’s 2019 comment letter in response to the CFPB’s Advance Notice of Proposed Rulemaking (ANPR) on the QM Definition. Also consistent with its 2019 comment letter, USMI suggests a better approach to a General QM definition would be a standard that includes a higher DTI threshold up to 50 percent with specified compensating factors.

USMI also urged the CFPB to allow sufficient time for a smooth transition from the temporary QM category, the “GSE Patch,” to the new General QM definition. In August, USMI submitted comments to the CFPB on the GSE Patch, recommending the Bureau set the sunset date for the GSE Patch to be at least six months after the effective date of the General QM definition final rule. USMI wrote that “this time will be critical given the extensive and still undetermined scope of COVID-19 on the financial services industry as it focuses resources on responding to the economic and health fallout from the pandemic.”

Coalition Urges CFPB to Increase the QM Safe Harbor Threshold. USMI also co-signed a joint industry trade letter with 11 other housing policy and consumer advocate groups calling on the CFPB to increase the QM Safe Harbor threshold from 150 to 200 bps over the current APOR. USMI previously discussed the need for increasing the Safe Harbor threshold to mitigate borrower impact in a blog post. USMI wrote that based on its analysis of “mortgage originations, loan performance, market dynamics, and the need to ensure consumer access to affordable mortgage finance, we recommend that this threshold should be pegged to the same threshold as the QM status, which the NPR suggests should be 200 bps.” Doing so would result in a more level playing field and by changing that threshold, would mitigate the impact on borrowers.

ICYMI: USMI Column Published in The Dallas Morning News.On August 17, USMI published its latest column titled, “The Smarter Way to Buy a Home.” USMI breaks down the 20 percent down payment myth and explains how private mortgage insurance can help home-ready buyers get in their house sooner. USMI also highlights that private mortgage insurance is temporary, unlike other low-down payment options. USMI notes that once the borrower reaches 20 percent equity in their house, private mortgage insurance cancels—which is a significant advantage to borrowers considering a low down payment mortgage. Read the column in The Dallas Moring News.

USMI President Lindsey Johnson appeared on the Practical Wealth Show podcast with Curtis May and discussed how private mortgage insurance helps home-ready buyers get in their home sooner.

WASHINGTON — U.S. Mortgage Insurers (USMI), the association representing the nation’s leading private mortgage insurance (MI) companies, submitted its comment letter to the Consumer Financial Protection Bureau (CFPB or Bureau) for its proposed rule on the General Qualified Mortgage (QM) Definition under the Truth in Lending Act (Regulation Z).

“While the CFPB is undertaking a thoughtful process to update the General QM definition, USMI urges the Bureau to strike a proper balance between prudent and transparent underwriting standards, and access to affordable and sustainable mortgage finance credit for home-ready borrowers,” said Lindsey Johnson, President of USMI. “Changes to the QM definition will broadly inform standards and practices across the mortgage market, but the currently proposed rule could limit access to the conventional market for the very borrowers that have traditionally been underserved.”

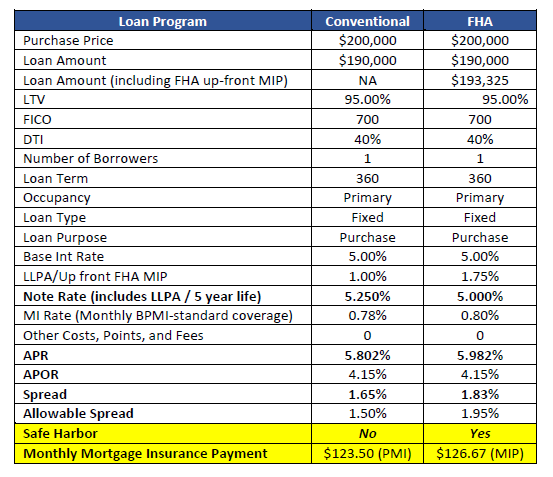

To ensure the QM definition does not inadvertently limit access to credit for home-ready borrowers, and particularly minority borrowers, USMI recommends that the QM Safe Harbor should be set at 200 basis points (bps) above the Average Prime Offer Rate (APOR). USMI states that this modification to the proposed rule would create a level playing field for the QM standard across the conventional and government mortgage markets, adding that historical delinquency data demonstrates that conventional mortgages with rate spreads between 150 bps and 200 bps are prudently underwritten and sustainable loans that have performed well.

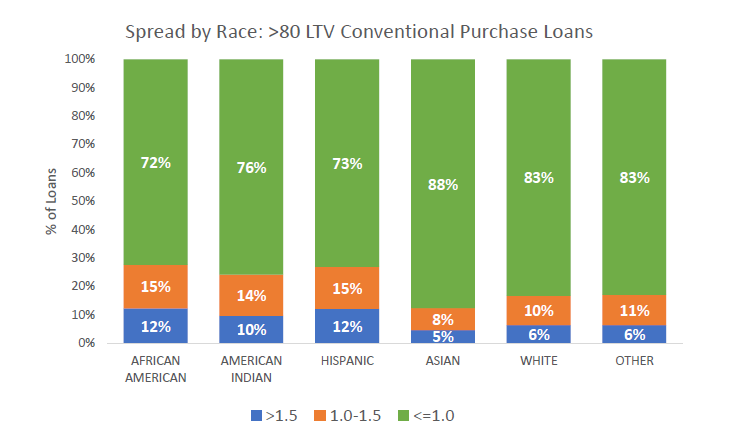

USMI highlights that “[a]ccording to 2019 Home Mortgage Disclosure Act (HMDA) data for conventional low down payment purchase mortgages (>80 percent loan-to-value ratio), Black and Hispanic borrowers were twice as likely as White borrowers to have mortgages with annual percentage rates in excess of the APOR plus 150 bps Safe Harbor spread. Under the proposed rule, many of the borrowers who are above the 150 bps threshold will be left only with the option of a Federal Housing Administration (FHA) loan, which means they have significantly fewer competitive choices in terms of product offerings and loans.”

Further, USMI agrees with the Bureau’s assessment that a hard 43 percent debt-to-income (DTI) ratio cap would be the most harmful option for the General QM definition because it would severely limit access to credit in the conventional market. Consistent with its September 2019 comment letter in response to the CFPB’s Advance Notice of Proposed Rule (ANPR) on the QM Definition, USMI continues to believe that the best approach to a General QM definition would be a standard that includes a higher DTI threshold with specified compensating factors.

In its comments, USMI advises the CFPB to preserve robust and measurable underwriting standards and practices as part of the requirements for “consider and verify” that have been proven to balance access to credit and prudent mortgage underwriting standards. With the elimination of reliance on a DTI cap and the introduction of a “consider and verify” standard for mortgage underwriting, it is critical that the CFPB identify specific requirements or best practices to be used by lenders to qualify for the compliance safe harbor.

Other recommendations to the CFPB include: working closely with federal regulators to implement a transparent and coordinated housing policy that promotes access to credit and prudent mortgage underwriting and creates a level playing field; and reconsidering its approach to adjustable-rate mortgages (ARMs) by amending the NPR to exclude 5-year ARM products from the proposed treatment of short-reset ARMs, as data demonstrates that ≥5-year ARM performance is in line with, or better than, >20-year fixed rate mortgages.

Finally, USMI urges the CFPB to provide sufficient time for a smooth transition from the temporary QM category (known as the government sponsored enterprises or “GSE Patch”) to the new General QM definition. This is particularly important given the extensive and undetermined scope of COVID-19 as the financial services industry appropriately focuses resources on responding to the economic and health fallout from the pandemic.

USMI writes, “[d]epending on the complexity of the finalized revisions to the General QM definition, the significance of the penalties for a violation of the [ability to repay]/QM Rule, and the large number of mortgage industry participants that will need to update their operations and systems, USMI recommends that the Bureau set the sunset date for the GSE Patch to be at least six months after the effective date of the general QM definition final rule. This would allow lenders to use either the GSE Patch or the new General QM definition during the mortgage underwriting process.”

USMI’s full comments on the CFPB’s proposed General QM Definition can be found here; its comment letter to the Bureau on the GSE patch extension can be found here; the 2019 comment letter to the CFPB’s Advance NPR can be found here; and its blog on why the Safe Harbor threshold should be increased can be found here.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org

The Honorable Kathleen Kraninger Director Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20052

Re: Qualified Mortgage Definition under the Truth in Lending Act (Regulation Z): General QM Loan Definition, Docket No. CFPB 2020-0020

Dear Director Kraninger:

U.S. Mortgage Insurers (USMI)1 represents America’s leading providers of private mortgage insurance (MI). Our members are dedicated to a strong housing finance system backed by private capital that enables access to prudent and sustainable mortgage finance for borrowers, while also protecting Fannie Mae and Freddie Mac (the GSEs) and the American taxpayer from mortgage credit-related losses. The MI industry has more than six decades of expertise in underwriting and actively managing mortgage credit risk. Our member companies are uniquely qualified to provide insights on federal policies concerning underwriting standards for the conventional mortgage market, especially given our experience balancing prudent underwriting with access to affordable credit.

USMI appreciates the opportunity to comment on the Consumer Financial Protection Bureau’s (Bureau) NNotice of Proposed Rulemaking (NPR)2 regarding changes to the General Qualified Mortgage (QM) definition. Done right, a revised General QM definition will promote prudent underwriting that enables home-ready borrowers to receive fairly priced and affordable conventional mortgages. USMI and other housing finance stakeholders recognize that changes to the General QM definition will broadly inform underwriting standards and practices across the mortgage market. As discussed below, we are concerned that, as contemplated, the proposed rule could limit access to the conventional market for the very borrowers that have traditionally been underserved.

In our comments below, USMI will discuss the following observations and recommendations:

The Safe Harbor should be set at 200 basis points (bps) above the Average Prime Offer Rate (APOR) to ensure that the General QM definition does not inadvertently limit access to credit for home-ready borrowers, and particularly minority borrowers.

As part of the requirements for “consider and verify,” the Bureau’s final rule should preserve robust and measurable underwriting standards and practices that have been proven to balance access to credit and prudent mortgage underwriting standards.

It is critical that the Bureau work closely with federal regulators to implement a transparent and coordinated housing policy that promotes access to credit, prudent mortgage underwriting, and creates a level playing field.

The Bureau should reconsider its approach to adjustable-rate mortgages (ARMs) and amend the NPR to exclude five-year ARM products from the proposed treatment of short-reset ARMs.

USMI agrees with the Bureau’s assessment that a hard 43% debt-to-income (DTI) ratio cap would be the most harmful option for the General QM definition because it would severely limit access to credit in the conventional market. Consistent with our comment letter dated September 16, 2019 in response to the Bureau’s Advance Notice of Proposed Rulemaking on the QM Definition, we continue to believe that the best approach to a General QM definition would be a standard that includes a higher DTI threshold with specified compensating factors. Please see Appendix A for additional information about a General QM definition that retains a DTI limit.

Overview of QM Definition or the Conventional Market

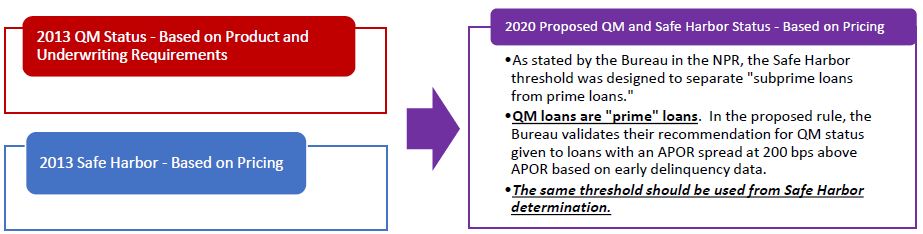

2013 ATR/QM Rule Street Reform and Consumer Protection Act (Dodd-Frank)4 that created specific mortgage product restrictions and required the Bureau to promulgate the Ability-to-Repay/Qualified Mortgage Rule (ATR/QM Rule). The Bureau’s final ATR/QM Rule – issued in June 2013 and made effective on January 10, 2014 – created a General QM category with a 43% DTI limit and requirements concerning product features and points and fees, as well as a temporary QM category for mortgages that met statutory limitations on product features and points and fees and are eligible for purchase by Fannie Mae or Freddie Mac. This temporary QM category has become known as the “GSE Patch,” and the 2013 final rule stipulated that the GSE Patch would sunset the earlier of: (1) the GSEs exiting conservatorship; or (2) January 10, 2021. The GSE Patch has served its intended purpose of maintaining credit availability in the conventional mortgage market and CoreLogic estimates that approximately 16% of 2018 mortgage originations ($260 billion) were made as QM loans by virtue of the GSE Patch. We note that, under the Patch, QM loans have included mortgages with DTI ratios up to 50% with compensating factors.

The Dodd-Frank Act went beyond previous federal consumer protection laws that were largely intended to root out predatory, subprime mortgage products, including the Home Ownership and Equity Protection Act (HOEPA) that defined a class of “higher priced mortgage loans” (HPMLs). HOEPA was later expanded in 2001 and 2008 to provide for a presumed violation of the law when a lender engaged in a pattern of originating higher-priced mortgages without verifying and documenting the borrower’s ATR. Dodd-Frank went beyond HPMLs to address concerns about mortgage underwriting practices by creating specific mortgage product restrictions and requiring the CFPB to promulgate a rule defining “Qualified Mortgage” based on specific underwriting criteria. As promulgated in the 2013 final rule, QM and Safe Harbor were determined by two separate measures: QM status was based on product and underwriting requirements; and Safe Harbor was based on loan pricing. Given that distinction, the different standards made a certain amount of sense. Under the 2020 proposed rule, however, QM status and Safe Harbor are measured using the same metric – price – so there is no longer any reason to set those standards at different spread amounts. As further discussed below, and as the Bureau validates based on early delinquency data, this spread threshold should be set at 200 bps above APOR.

2020 NPR The NPR would remove the 43% DTI limit and instead grant QM status to a mortgage “only if the annual percentage rate (APR) exceeds [the] APOR for a comparable transaction by less than two percentage points as of the date the interest rate is set.” Although the NPR recommends establishing the pricing threshold for defining QM loans at an APR spread of 200 bps over APOR, it also preserves the APR spread over APOR of 150 bps to distinguish between Safe Harbor and Rebuttable Presumption QM loans.

QM Safe Harbor Threshold Should be Increased to APOR Plus 200 bps

Safe Harbor Threshold Will Determine the Conventional Mortgage Market If the final General QM rule maintains a pricing-based QM, the Bureau should increase the spread that is used to delineate Safe Harbor loans and Rebuttable Presumption loans from 150 bps to 200 bps over APOR. This would not only align the delineation with the APOR threshold that the Bureau recommends using to determine QM status, but would also broaden access to the conventional QM market for more home-ready borrowers and create a more level and coordinated housing finance system across the government and conventional mortgage markets.

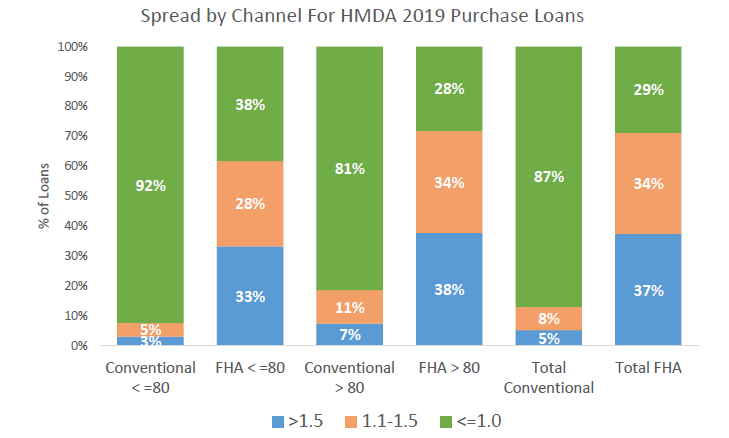

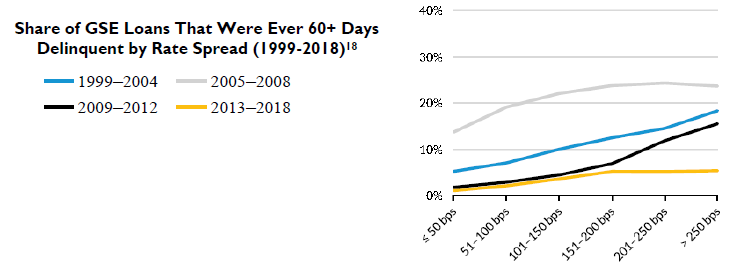

Determining the Safe Harbor threshold impacts the makeup for the conventional market and who it will be able to serve under a new General QM definition because so few Rebuttable Presumption mortgages have been originated in the conventional market since the final QM rule was implemented in 2014. This is because mortgage lenders have sought to minimize their legal risk by almost exclusively originating QM Safe Harbor loans, thus effectively making the Safe Harbor threshold the standard for QM loans. Home Mortgage Disclosure Act (HMDA) data shows that only 4.6% of purchase QM conventional mortgages and 2.5% of refinance QM conventional mortgages from 2019 were above the APOR plus 150 bps Safe Harbor threshold. However, this data should not be mistakenly interpreted as an indication that there is not a market interest in safely lending above this threshold. In fact, lenders are willing to make loans with pricing above 150 bps when those loans have Safe Harbor status, as evidenced by the fact that loans insured by the Federal Housing Administration (FHA) are five times more likely to be originated with spreads above 150 bps than conventional market loans because the FHA Safe Harbor delineation is set at close to 200 bps. It is also important to look at the performance of loans with higher spreads. Historical GSE 60 plus days delinquency data underscores that loans with spreads up to 200 bps above APOR have performed well, are sustainable mortgages that have been made to creditworthy borrowers, and should qualify for QM Safe Harbor treatment.

Minority Borrowers are Denied Greater Choice and Access to Credit as a Result of a Safe Harbor Threshold at 150 bps Above APOR Failure to increase the QM Safe Harbor threshold to 200 bps above APOR misaligns the Safe Harbor definition across the government and conventional mortgage markets and results in the same mortgage being a QM Safe Harbor in one channel, but merely a Rebuttable Presumption QM in another, effectively denying that borrower true choice in lenders and mortgage products. This impact is particularly acute for minority borrowers who overwhelmingly rely on low down payment mortgages to purchase their homes. According to 2019 HMDA data for conventional low down payment purchase mortgages (>80% loan-to-value or LTV), Black and Hispanic borrowers were twice as likely as White borrowers to have mortgages with APRs in excess of the APOR plus 150 bps Safe Harbor spread.