WASHINGTON — Lindsey Johnson, President of U.S. Mortgage Insurers (USMI), today issued the following statement on the confirmation of Brian Montgomery by the United States Senate to serve as Deputy Secretary of the U.S. Department of Housing and Urban Development (HUD):

“USMI congratulates Deputy Secretary Brian Montgomery on his bipartisan Senate confirmation to help lead the U.S. Department of Housing and Urban Development (HUD). HUD serves as an important component of the more than $16 trillion U.S. outstanding mortgage debt market, and we know that Deputy Secretary Montgomery is deeply committed to HUD’s mission and to policies that support homeowners and renters.

“Deputy Secretary Montgomery is a respected, seasoned mortgage finance expert. His unique experience in both the private and public sectors, including his time as Assistant Secretary for Housing – Federal Housing Commissioner for HUD in the Donald Trump, George W. Bush, and Barack Obama administrations as well as his time as Acting HUD Secretary has been and will continue to be a major asset to the U.S. housing finance system. We are confident that Deputy Secretary Montgomery will help lead HUD and strengthen HUD’s programs and operations, and his leadership will be invaluable during these trying times in which his expertise and knowledge will be of great value.

“USMI and the private mortgage insurance industry look forward to working with Deputy Secretary Montgomery, Secretary Benjamin Carson, and other HUD leaders to establish a coordinated and robust housing finance system that prudently enables affordable homeownership for American families and also protects taxpayers from undue mortgage risk.”

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org

Consumer Financial Protection Bureau (CFPB) Director on QM Rule. On January 17, CFPB Director Kathy Kraninger sent a letter to select members of Congress notifying them of the CFPB’s intentions to eliminate the debt-to-income (DTI) ratio requirement and move to a standard based on an alternative metric, specifically a pricing threshold. She wrote that the CFPB would extend the QM definition “for a short period until the effective date of the proposed alternative or until one or more of the GSEs [government sponsored enterprises] exits conservatorship, whichever comes first.” As for the DTI requirement, Director Kraninger proposed replacing it for a pricing threshold, such as the difference between the loan’s annual percentage rate (APR) and the average prime offer rate (APOR) for a comparable transaction (the APOR-approach).

Industry and Consumer Groups Call for Maintaining Prudent Underwriting Guardrails as Part of QM Patch Replacement. In response, on January 21, USMI joined eight other organizations on a letter to Director Kraninger recommending the CFPB replace the current QM definition with one that relies on measurable underwriting thresholds and the use of compensating factors (such as liquid reserves, limited payment shock, and/or a larger down payment from the borrower’s own funds) for higher risk mortgages (those loans with DTI ratios above 45 and up to 50 percent). This letter goes on to explain how alternative recommendations (e.g., using pricing thresholds) would have a negative impact on minority and lower income borrowers and should be avoided through the better approach of relying on other compensating factors that enable prudent underwriting and affordable access to credit.

The organizations also urged “that the transition period from the existing GSE Patch to the new QM framework be sufficiently long to allow market participants adequate time to plan for, and adjust to, new rules and underwriting standards” in order to avoid the risks of regulatory uncertainty “that might cause mortgage originators to retreat from lending to creditworthy homebuying and refinancing borrowers.”

Kraninger Testifies before House Financial Services Committee. On February 6, Director Kraninger testified before the House Committee on Financial Services where the discussion on the QM definition continued. Representatives Nydia M. Velasquez (D-NY), Brad Sherman (D-CA), French Hill (R-AR), Warren Davidson (R-OH), Alma Adams (D-NC), and Anthony Gonzalez (R-OH) all raised questions on the CFPB’s plan to replace the DTI requirement and its potential impact on the housing finance market and on low-to-moderate income borrowers’ access to safe and affordable mortgage finance credit. When asked on the timing for the release of the QM Notice of Proposed Rulemaking (NPR), Director Kraninger responded “no later than May,” which was affirmed this week by the Bureau when it formally announced it will issue proposed changes to the QM definition by May. Director Kraninger said, “[t]he bureau will propose an alternative, such as a pricing threshold, to better ensure that responsible, affordable mortgage credit remains available to consumers.” If you have not read it yet, USMI released a blog last year with observations and recommendations for replacing the QM and balancing prudent underwriting with borrower access to affordable mortgage finance in the conventional market.

USMI Speaks on QM “in a Post-Patch World.” On February 18, USMI President Johnson spoke at a panel co-hosted by the Mortgage Bankers Association (MBA) and Women in Housing Finance (WHF) on the future of QM after the expiration of the QM Patch. The panel discussed how the housing industry could change in the near future and the roles that other housing intuitions, like private mortgage insurance (MI), will play in supporting a vibrant housing industry.

USMI President Lindsey Johnson at Structured Finance Association (SFA). This week, USMI President Johnson, along with Pete Carroll from Core Logic, Andrew Davidson from Andrew Davidson & Co., Rajiv Kamilla from Goldman Sachs, Larry Platt from Mayer Brown, and Jeremy Switzer from Penny Mac, spoke on a panel at SFA’s conference in Las Vegas titled, “Building Industry Governance for the PLS Market.” Johnson discussed the important governance changes and enhancements in quality controls and industry practices and regulation that have occurred in the conventional market that would greatly benefit the private label security (PLS) market, including the underwriting criteria that have developed under the QM Patch. Johnson also spoke about the role private MI can play to bring greater credit quality assurances and ensure prudent risk management in the PLS market.

Federal Housing Finance Agency Moves Ahead with Plans to End Conservatorship. On February 3, FHFA awarded the investment bank Houlihan Lokey Inc. a potential $45 million advisory contract to help recapitalize the GSEs as part of the government’s plan to end their conservatorships. FHFA Director Mark Calabria stated “[h]iring a financial advisor is a significant milestone toward ending the conservatorships of the enterprises,” adding that “[t]he next major milestone for the FHFA is the re-proposal of the capital rule, which will happen in the near future.”

FHFA Issues a Request for Input (RFI) on Federal Home Loan Bank (FHLBank) Membership. Earlier this week, the FHFA issued a RFI for FHLBank membership, in which it seeks input “on whether the FHFA’s existing regulation on FHLBank membership ensures the FHLBank System, consistent with statutory requirements, remains safe and sound, provides liquidity for housing finance through the housing and business cycle, and supports the FHLBanks’ housing finance and community development mission.”

Administration and Congress Take Action on Housing Affordability. Yesterday, the FHFA announced the authorization of payments for 2019 from the GSEs to the Department of Housing and Urban Development (HUD) for the Housing Trust Fund and Treasury for the Capital Magnet Fund. The Housing Trust Fund, an affordable housing program designed to increase and preserve the supply of decent, safe, and sanitary affordable housing for extremely low- and very low-income households, received $326.4 million and the Capital Magnet Fund, a program focused on the developments, preservation, rehabilitation, and purchase of housing for low income families, received $175.8 million. Congress also took steps this week to explore housing affordability and the House Financial Services Committee marked up and approved four bills concerning housing and community development:

H.R. 5931, the “Improving FHA Support for Small Dollar Mortgages Act of 2020” (Clay-Stivers), would require FHA to conduct a review of its policies to identify barriers to supporting mortgages under $70k and report to Congress within one year with a plan for removing such barriers. The bill was reported favorably to the House by a recorded vote of 48 to 0.

H.R. 149, the “Housing Fairness Act of 2020” (Rep. Green), would authorize increased funding for HUD’s Fair Housing Initiatives Program in addition to creating a new competitive matching grant program to support comprehensive studies of the causes and effects of ongoing discrimination and segregation, and the implementation of pilots to test solutions. The bill was reported favorably to the House by a recorded vote of 33 to 25.

H.R. 4351, the “Yes in My Backyard Act” (Rep. Heck), would require localities receiving CDBG funding to submit a plan to track and report on the implementation of certain land use policies that promote housing production. The bill was agreed to and reported favorably to House by a voice vote.

H.R. 5187, the “Housing Is Infrastructure Act” (Chairwoman Waters), would authorize $100.6 billion for investments in the nation’s affordable housing infrastructure, including public housing, supporting housing for seniors and people with disabilities, making housing affordable to the lowest-income people, and rural and Native American housing. The bill was reported favorably to the House by a recorded vote of 33 to 25.

Dana Wade Nominated as Federal Housing Administration (FHA) Commissioner. On February 20, the White House announced President Trump’s intent to nominate Dana Wade as FHA Commissioner and oversee the agency’s $1.3 trillion portfolio. USMI President Lindsey Johnson issued a statement applauding the nomination, stating that USMI “look[s] forward to working closely with Dana Wade in seeking ways to establish a more complementary, collaborative, and consistent housing finance system that prudently enables homeownership for American families while also protecting taxpayers.”

USMI President Lindsey Johnson on the FHA Insurance Fund.Scotsman Guide shared USMI President Lindsey Johnson’s views on the current health of the FHA insurance fund in an article on the wider industry debate surrounding the FHA’s insurance fund. Johnson noted that the insurance fund is highly vulnerable to market changes, adding that “[t]axpayers are currently exposed to over $1.19 trillion in outstanding mortgage risk at the FHA. This would only increase if FHA insurance premiums were reduced. Also, any change to FHA’s life-of-loan coverage would mean exposing taxpayers to further undo risk.”

ICYMI: Extension of the MI Tax Deduction. In January, Congress passed the Further Consolidated Appropriations Act of 2020, which retroactively extended tax deductions for mortgage insurance premiums to calendar year 2018 and remains in effect throughout 2020. USMI President Lindsey Johnson issued a statement praising the extension saying, “[w]e are pleased Congress extended the mortgage insurance tax deduction for years 2018 through the end of 2020. Private MI has helped more than 30 million middle-income Americans become homeowners over the last 60 years, and for over 10 years the deductibility of mortgage insurance has helped benefit millions of these hard-working borrowers.” According to the most recent IRS statistics of income, in 2017 alone more than 2.285 million taxpayers benefited from the MI premium tax deduction. The deduction is available to homeowners (married filing jointly) with MI who have adjusted gross incomes under $100,000 and phases-out for adjusted gross incomes up to $110,000. Earlier this week, the IRS issued a news release (IR-2020-44) describing the procedure for taxpayers to claim benefits of for expired provisions for already-closed tax years. According to guidance from the IRS, homeowners seeking to retroactively claim a tax deduction for mortgage insurance premiums for tax year 2018 will need to file an amended return using form 1040-X.

WASHINGTON — Lindsey Johnson, President of the U.S. Mortgage Insurers (USMI), today issued the following statement on the nomination of Dana Wade to serve as Federal Housing Commissioner:

“USMI applauds the White House’s announcement of the President’s intent to nominate Dana Wade as the Federal Housing Commissioner to lead the Federal Housing Administration (FHA) and oversee the agency’s $1.3 trillion portfolio. Wade is a respected expert with broad experience in financial and housing policy issues. Her previous work, including her time as Acting Federal Housing Commissioner and Assistant Secretary for Housing, will allow her to swiftly start to address the important issues facing the housing finance system. We look forward to working closely with Dana Wade in seeking ways to establish a more complementary, collaborative, and consistent housing finance system that prudently enables homeownership for American families while also protecting taxpayers.”

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

USMI President Lindsey Johnson appeared on “Best Real Estate Investing Advice Ever” with Joe Fairless to discuss her background in mortgage finance and the role of private mortgage insurance in today’s mortgage system.

The Honorable Kathleen L. Kraninger Director Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20552

Dear Director Kraninger:

The undersigned organizations are writing in response to the Consumer Financial Protection Bureau’s (Bureau) rulemaking regarding the definition of a Qualified Mortgage (QM). Our organizations represent diverse housing finance stakeholders, including consumer groups, lenders, and mortgage insurers, and we appreciate the opportunity to provide our joint perspectives in addition to our individual comment letters that were submitted in response to the Bureau’s Advance Notice of Proposed Rulemaking (ANPR). The Ability-to-Repay (ATR) rule in the Dodd-Frank Wall Street Reform and Consumer Protection Act is one of the most important consumer safeguards in the legislation, and the Bureau’s regulations to promulgate and execute it will directly affect access to safe and affordable mortgage finance credit. We all agree that maintaining access to affordable and sustainable mortgage credit should be a key objective of the Bureau’s revised rulemaking.

We appreciate the Bureau’s thoughtful approach to assessing and implementing potential changes to the QM definition. This letter contains our joint recommendation that the Bureau implement a QM definition that relies on measurable underwriting thresholds and the use of compensating factors for higher risk mortgages rather than either a pricing-based QM definition that uses the spread between the annual percentage rate (APR) and the Average Prime Offer Rate (APOR) as a proxy for underwriting requirements (the “APOR approach”) or a hard cut-off at either 43% or 45% DTI.

Specifically, this coalition strongly supports:

1. The continued use of a modified debt-to-income (DTI) ratio in conjunction with certain compensating factors, which could be used in the underwriting process and would provide guidance to creditors on their use; and

2. Significant changes to Appendix Q to rely on more flexible and dynamic standards for calculating income and debt.

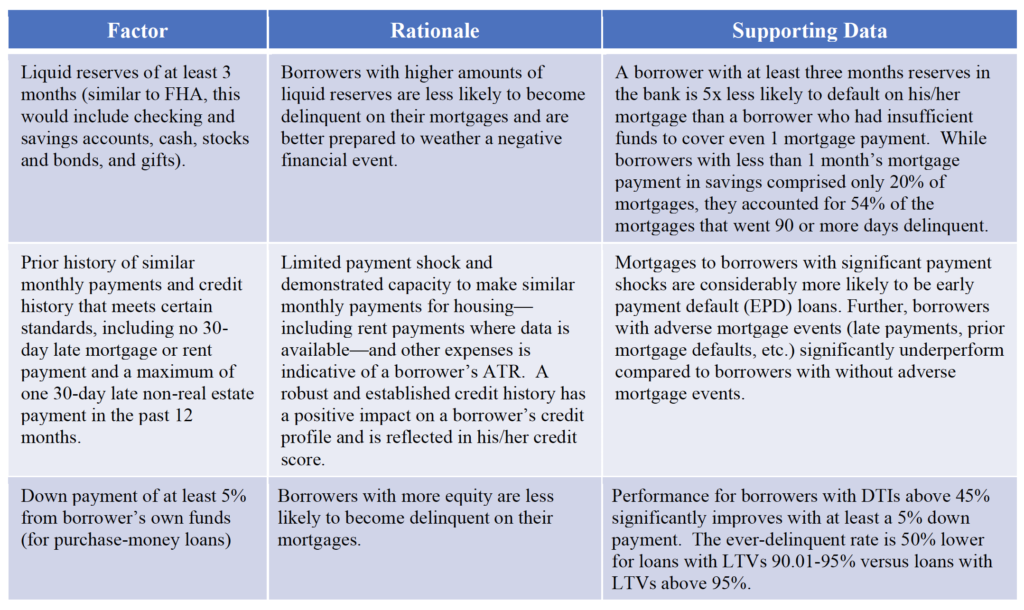

Compensating Factors Would Enable Prudent Underwriting and Affordable Access to Credit

The Bureau should establish a set of transparent mitigating underwriting criteria – “compensating factors” – for mortgages with DTI ratios above 45% and up to 50%. While DTI is not the most predictive factor in assessing a borrower’s ability to repay, it can, in concert with compensating factors, function as a bright line that mitigates undue risk in the conventional market while continuing to provide affordable access to mortgage finance for creditworthy borrowers. Moreover, DTI is a widely and commonly used metric when considering a borrower’s ability to repay in mortgage loan underwriting and is the standard in the current rule issued in 2013. While a higher DTI may indicate increased stress for the borrower and a consequent strain on ability to repay, the presence of other positive credit characteristics – such as liquid reserves, limited payment shock, and/or a down payment from the borrower’s own funds – can mitigate the heightened risk and limit the risk layering that drives loan nonperformance. In fact, the automated underwriting systems (AUSs) used by Fannie Mae and Freddie Mac (the GSEs), as well as proprietary AUSs used by primary market lenders, have always used compensating factors to assess borrowers’ ATR, and such a multifactor approach has long been the standard for manual underwriting throughout the industry.

The efficacy of using compensating factors for high-DTI mortgages is demonstrated by the track record of loans acquired by the GSEs. Rather than introducing undue risk to the housing finance system, these loans have performed well. In fact, high-DTI loans (with ratios between 45.1% and 50%) underwritten using compensating factors outperform loans with lower DTI ratios (between 35.01% and 45%). The lower delinquency rates on the higher DTI loans are almost certainly due to the presence of appropriate compensating factors in the GSEs’ AUSs.

The table below reflects one specific set of compensating factors we believe are appropriate for borrowers with DTIs above 45% and up to 50% that could be tailored for the revised rule. These recommendations are based on: (1) internal analysis and efforts to “back into” the compensating factors currently used by the GSEs to avoid a dramatic shift in the market; and (2) known factors that significantly impact borrowers’ ATR. This is by no means an exhaustive list and we welcome further discussion about compensating factors and their respective predictiveness. The Bureau’s final rule on the QM definition could authorize the GSEs, Federal Housing Finance Agency (FHFA), or an independent standard-setting entity to formulate a transparent list of compensating factors and should make the underlying data and analysis available to the public for ongoing review and assessment to ensure that dynamic compensating factors can be updated to reflect changes in the market and mortgage credit risk environment.

Using an APOR-Only Approach Does Not Meet the Legislative Intent of the Statute and Does Not Appropriately Measure Ability to Repay

The APOR approach is premised on the faulty idea that pricing fully captures credit risk and that, in turn, credit risk is a reasonable marker for ability to repay. In the mortgage industry, a loan’s pricing reflects a number of factors outside of an individual borrower’s credit profile, including a lender’s balance sheet capacity, prepayment speeds, the value of mortgage servicing rights, business goals, and broader economic considerations. With regard to risk, pricing does consider down payment and credit score, but often fails to capture risk-mitigating characteristics such as borrower reserves, DTI ratios, and payment shock.

Any QM definition that relies solely on the statutory ATR requirements or the price of a loan will be seriously flawed. ATR requirements are too broad and do not adequately reflect a borrower’s ability to repay. On the other hand, a loan’s price can be manipulated to gain QM safe-harbor status.

There are several important consumer protection concerns at issue. First, loans made within the QM safe harbor are not, practically speaking, subject to underwriting thresholds/requirements for determining ATR because if a loan meets the product feature requirements along with any other adopted QM standards, no adjudicative body or regulator can “look under the hood” and examine the fuller underwriting process.

Second, if the only underwriting protection is APOR, mortgages could be made to financially vulnerable borrowers at a price just below the safe harbor threshold even though the borrowers’ financial/credit profiles might otherwise call for greater underwriting analysis consideration and ATR protections. This mispricing of risk helped set the 2008 financial crisis in motion.

Third, using this approach assumes creditors are able to uniformly and accurately price risk of repayment, an assumption that was disproven in the financial crisis and ignores market and economic pressures that can drive underpricing of risk.

Fourth, an APOR approach could increase risk within the mortgage finance system as APOR is a trailing indicator of risk and can be procyclical. Therefore, periods of sharply rising rates could cause temporary suspensions in lending that could impact prime loans with higher risk attributes. Additionally, during periods of low rates and loose credit, borrowers run the risk of being overextended.

An APOR Approach Could Make It Harder for Creditworthy Low Down Payment and Minority Borrowers to Obtain Mortgages

Moving from a DTI-based QM standard to an APOR approach could reduce the ability of low down payment and minority borrowers to obtain conventional mortgages. For example, based on 2018 Home Mortgage Disclosure Act (HMDA) data, $11-12 billion in GSE purchase origination volume had loan-to-value (LTV) ratios of >80% and APRs with spreads in excess of APOR + 150 basis points. Further, based on the same dataset, African American and Hispanic borrowers were twice as likely as white borrowers to have mortgages with APRs in excess of the APOR + 150 basis points safe harbor spread.

Many qualified borrowers who are not able to obtain mortgages that meet an APOR standard under a revised QM definition would be denied access to homeownership opportunities while other qualified borrowers in this category would see their loan options reduced. Some mortgages that would normally have been made in the conventional market would gravitate towards the 100% taxpayer-backed FHA, an outcome that is inconsistent with the Administration’s housing finance reform principles and objectives as articulated in the September 2019 reports from the Department of the Treasury and the Department of Housing and Urban Development.

Regardless of the solution chosen, we urge that the transition period from the existing GSE Patch to the new QM framework be sufficiently long to allow market participants adequate time to plan for, and adjust to, new rules and underwriting standards. Any transition to a new QM rule ought to be smooth and well thought-out. Otherwise it risks regulatory uncertainty that might cause mortgage originators to retreat from lending to creditworthy homebuying and refinancing borrowers.

Thank you again for the opportunity to share our collective perspectives on the Bureau’s work regarding the QM definition. The expiration of the GSE Patch and what is developed to replace it will have significant implications for consumers’ access to affordable and sustainable mortgage finance credit. We hope to have a continued constructive dialogue through a robust comment process to result in the best future standard and we welcome the opportunity to serve as resources as the Bureau works toward a proposed, and then final, rule.

Sincerely,

Consumer Federation of America Community Home Lenders Association The Community Mortgage Lenders of America Independent Community Bankers of America National Association of Federally-Insured Credit Unions National Association of REALTORS® National Community Stabilization Trust National Consumer Law Center (on behalf of its low-income clients) U.S. Mortgage Insurers

CC: Andrew Duke Brian Johnson Mark McArdle Kirsten Sutton Thomas Pahl

WASHINGTON — U.S. Mortgage Insurers (USMI) President Lindsey Johnson issued the following statement on the decision made by the U.S. Congress to extend the tax deduction for mortgage insurance (MI) premiums in the H.R.1865 – Further Consolidated Appropriations Act, 2020.

“We are pleased Congress extended the mortgage insurance tax deduction for years 2018 through the end of 2020. Private MI has helped more than 30 million middle-income Americans become homeowners over the last 60 years, and for over 10 years the deductibility of mortgage insurance has helped benefit millions of these hard-working borrowers—the majority of whom made annual incomes of less than $75,000.

“This tax deduction was first available to taxpayers in 2007 and extended multiple times since then on a bipartisan basis. The last deduction expired at the end of 2016, and with this last extension for amounts paid or accrued after December 31, 2017, and before December 31, 2020, lawmakers demonstrate their commitment towards helping low-down payment and first-time homebuyers.

“Over the last six decades, private MI has bridged the gap between a 20 percent down payment and access to mortgage finance credit. In the past year alone, MI helped more than 1.2 million homeowners purchase or refinance homes.”

According to the most recent IRS statistics of income, in 2017 alone more than 2.285 million taxpayers benefited from the MI premium tax deduction. The deduction is available to homeowners with MI who have an adjusted gross income under $100,000 and phases-out for adjusted gross incomes up to $110,000. USMI data show that nearly 60 percent of purchase loans with private MI go to first-time homebuyers and more than 40 percent of borrowers with private MI have incomes below $75,000.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

WASHINGTON — U.S. Mortgage Insurers (USMI) President Lindsey Johnson issued the following statement on the decision made by the U.S. Congress to extend the tax deduction for mortgage insurance (MI) premiums in the H.R.1865 – Further Consolidated Appropriations Act, 2020.

“We are pleased Congress extended the mortgage insurance tax deduction for years 2018 through the end of 2020. Private MI has helped more than 30 million middle-income Americans become homeowners over the last 60 years, and for over 10 years the deductibility of mortgage insurance has helped benefit millions of these hard-working borrowers—the majority of whom made annual incomes of less than $75,000.

“This tax deduction was first available to taxpayers in 2007 and extended multiple times since then on a bipartisan basis. The last deduction expired at the end of 2016, and with this last extension for amounts paid or accrued after December 31, 2017, and before December 31, 2020, lawmakers demonstrate their commitment towards helping low-down payment and first-time homebuyers.

“Over the last six decades, private MI has bridged the gap between a 20 percent down payment and access to mortgage finance credit. In the past year alone, MI helped more than 1.2 million homeowners purchase or refinance homes.”

According to the most recent IRS statistics of income, in 2017 alone more than 2.285 million taxpayers benefited from the MI premium tax deduction. The deduction is available to homeowners with MI who have an adjusted gross income under $100,000 and phases-out for adjusted gross incomes up to $110,000. USMI data show that nearly 60 percent of purchase loans with private MI go to first-time homebuyers and more than 40 percent of borrowers with private MI have incomes below $75,000.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

Some hailed the Department of Housing and Urban Development’s annual report on the Federal Housing Administration’s financial status as evidence that the government mortgage insurance program should lower its fees. And they said that FHA should consider expanding its footprint in the housing finance market.

But HUD Secretary Ben Carson made clear that while FHA’s financial health has improved, it should “maintain its focus on providing access to mortgage financing to low- and moderate-income families that cannot be fulfilled through traditional underwriting.”

The FHA serves an important countercyclical role in the housing finance system; however, it is important that policymakers recognize that there is a vibrant conventional market that is able to serve many borrowers and prudently help them access affordable mortgage finance. Further, because FHA-backed mortgages protect 100% of the risk, expanding the FHA would mean expanding taxpayer exposure to that risk. This is simply not necessary.

Indeed, low down payment lending is critically important to the U.S. housing system. It gives many first-time home buyers access to the conventional mortgage market without requiring them to put a full 20% down. In the third quarter of 2019, nearly 80% of first-time homebuyers used these mortgages — 35% of which were backed by private mortgage insurance. With the private sector taking the first-loss risk exposure on these loans, the federal government, and thus taxpayers, are far more protected from mortgage credit risk.

The FHA-insured market and the conventional market should complement one another rather than compete. The conventional market — where the credit risk is backed by private capital — is well positioned to play a bigger role in facilitating access to affordable credit. It can do so without unnecessarily saddling the government or taxpayers with risk.

This better enables the FHA to focus on its mission of supporting those borrowers who do not have access to traditional financing — and to ensure it can play its countercyclical role through all market cycles.

In 2018, conventional loans with private MI helped more than one million low down payment borrowers — nearly 60% of which were first-time homebuyers and nearly 40% had incomes below $75,000. And in the first three quarters of 2019, nearly 47% of insured loans had private MI and the industry supported almost $275 billion in new originations. On the other hand, the FHA has over $1.2 trillion of outstanding risk exposure in 2019, according to the HUD report.

For borrowers, conventional low down payment mortgages with private MI are a good deal, because they are affordable despite a higher loan-to-value ratio and the insurance cancels once 20% equity is built. This results in direct savings for the borrower, compared to the FHA where premiums are typically paid for the life of the loan. Further, according to a recent analysis by the Urban Institute, loans with private MI were more affordable than loans backed by FHA for the majority of credit score and down payment cohorts for low down payment borrowers. And for the housing system these loans are a good deal because compared to FHA-backed mortgages, there is less risk exposure for taxpayers. Plus private mortgage insurers serve as a second set of eyes during the underwriting process to ensure that borrowers are set up for sustainable homeownership.

Instead of asking how FHA lending can be expanded the debate should revolve around prudently making low down payment mortgages in general more affordable and accessible to ensure risk is being managed appropriately. It can be done. Secretary Carson and other regulators have outlined in their recent reform plans ways to promote private capital supporting the housing finance system where possible.

Further the mortgage credit landscape is very different today than it was prefinancial crisis, largely due to new statutory restrictions of mortgage product features and federal regulation. For example, the Qualified Mortgage Rule provides the necessary safeguards for lending and underwriting. These safeguards, including measurable thresholds to assess a borrower’s ability-to-repay, have resulted in much better and safer mortgages being originated. In fact, foreclosure rates are at a 20-year low.

As regulators assess changes to mortgage underwriting requirements, including the expiration of the GSE patch in the QM Rule, these changes should be done in a coordinated manner with federal housing agencies by collaborating to create and implement a harmonized standard that can apply across the conventional and FHA mortgage markets alike to ensure a level playing field. Otherwise, the resulting regulatory patchwork could create arbitrage opportunities, lock some consumers out of the market due to higher costs, and merely shift, rather than reduce, the government’s exposure to mortgage credit risk.

Our housing regulators have a significant opportunity to strike the right balance to ensure that both access and risk are managed throughout the mortgage finance system. Private mortgage insurers understand this delicate balance and look forward to working with them to achieve sustainable levels for each.

###

National Mortgage News originally published USMI President Lindsey Johnson’s opinion piece, “No, the FHA should not be pushed to the brink again” on December 24. The piece was also published by American Banker.

USMI President Lindsey Johnson appeared on “Wine and Dime” with Amy Irvine to discuss how private mortgage insurance can help millenials get into their first home.

As the year draws to a close, the focus is on the end-of-year legislative and rulemaking deadlines—as well as looking at what’s ahead for housing in 2020. Earlier this month, the Urban Institute published an updated report that provides analysis on private mortgage insurance (MI) borrowers and the role private MI plays in reducing mortgage risk exposure. In November, the Federal Housing Finance Agency (FHFA) announced its plans to re-propose the Enterprise Capital Rule in 2020. In addition, Citizens Against Government Waste (CAGW) and National Taxpayers Union (NTU) released analysis of the Trump Administration’s Housing Finance Reform Plans, emphasizing the need to transition the government sponsored enterprises (GSEs), Fannie Mae and Freddie Mac, out of conservatorship. It highlights the role that private capital can play in facilitating such a transition. The Senate also moved closer to filling a very important housing policy position at the Department of Housing and Urban Development (HUD) when Federal Housing Administration (FHA) Commissioner Brian Montgomery was approved by the Senate Banking Committee to serve as HUD’s Deputy Secretary. Finally, FHFA and HUD increased loan limits for mortgages acquired by the GSEs and insured by the FHA, respectively.

Urban Institute releases an update to its MI chart book. On December 4, the Urban Institute published an updated analysis of the MI market, highlighting both the role that MI has played in enabling homeownership, as well as the protection private MI offers lenders, the GSEs, and taxpayers. The report, which included national and state-specific data, highlighted the borrowers currently being served by private MI, noting these borrowers tend to have higher credit scores and lower loan-to-value (LTV) and debt-to-income (DTI) ratios than FHA borrowers. The report highlights the important role private MI plays in helping to ensure low- to moderate-income and first-time homebuyers have access to the conventional market. It details that private MI is more affordable than FHA-back loans for the majority of combinations of FICO score and LTV ratios of 96.5, 95, 90, and 85 percent. The report also found that private MI borrowers tend to have lower credit scores, higher LTV and DTI ratios, and are more likely to be first-time homebuyers than conventional borrowers without private MI. Importantly, GSE loans with private MI have lower loss severities than non-private MI GSE loans, despite their higher LTV ratios. In other words, private MI is highly effective in allowing more qualified borrowers enter the mortgage market and achieve homeownership, while significantly reducing losses to the GSEs, which in turn reduces taxpayers’ risk.

FHFA’s Enterprise Capital Rule. In mid-November, FHFA announced its plans to re-propose the Enterprise Capital Rule in 2020. Director Mark Calabria remarked, “the Capital Rule is one of the most important rules I will issue as Director. This rule will be re-proposed and finalized within a timeline fully consistent with ending the conservatorships. Requiring the Enterprises to build capital that can properly support their risk ensures that taxpayers will never be on the hook again during an economic downturn.” Speaking at an event hosted by the Federalist Society on Tuesday, Director Calabria indicated that the FHFA is targeting Q1 of 2020 to re-propose the capital rule.

Originally introduced in 2018, the process of retaining capital at the GSEs is viewed as a critical first step to end their conservatorships. When FHFA first announced the plan in 2018, USMI submitted a comment letter stating it “supports meaningful and appropriate capital requirements for Fannie Mae and Freddie Mac and appreciates the FHFA for initiating this rulemaking process.” USMI agrees the rule is one of the most significant rules to be issued in that it will determine the future role of the GSEs, how private capital will be able to continue to support the conventional market to protect taxpayers, and importantly, the level of access and affordability of mortgage finance credit for consumers. USMI supports the FHFA working to re-propose and finalize a capital rule for the GSEs that strikes an appropriate balance between borrowers’ access to affordable mortgage finance and creates robust and countercyclical capital requirements that creates a transparent and level playing field, and that better insulates the GSEs and taxpayers from mortgage credit risk

CAGW and NTU released analysis of the Trump Administration’s Housing Finance Reform Plans. CAGW and NTU’s recent report offers a compelling argument in favor of enacting meaningful reforms at the GSEs to strengthen the nation’s housing finance system, concluding that “without comprehensive reform, taxpayers are likely to bail out the GSEs again in the future.” After analyzing the Treasury Department’s Housing Finance Reform Plan, CAGW and NTU believe that GSE reform should be guided by the following principles: 1) creating a sustainable, cautious path to recapitalization and release that minimizes systemic risk; 2) protecting taxpayers through stringent capital backstops and liquidity requirements; and 3) restricting mission creep and promoting private-sector competition.

Further, the report outlines several regulatory changes needed to facilitate the GSEs’ transition out of conservatorship including among other things that the Consumer Financial Protection Bureau (CFPB) should allow the current Qualified Mortgage (QM) Rule, known as the “GSE Patch,” to be replaced by transparent and consistent rules that apply across the industry. “Conservatorship was never meant to last forever,” the report concludes. By implementing these changes, the Trump Administration, Congress, FHFA, Treasury, and HUD have the opportunity to reshape the mortgage market and, ultimately, safeguard American taxpayers.

Senate Banking Committee advances Brian Montgomery’s nomination to serve as HUD Deputy Secretary. On December 11, FHA Commissioner Brian Montgomery was approved by a bipartisan vote of 20-5 in the U.S. Senate Committee on Banking, Housing and Urban Affairs to serve as HUD’s Deputy Secretary. His nomination will now move on to the Senate for final confirmation. In a statement issued on October 8, USMI applauded Montgomery’s nomination and commended him for his extensive background and experience that will allow him to immediately begin work on the most important issues facing the housing finance system.

FHFA and HUD increase loan limits for 2020. On November 26, FHFA announced the maximum conforming loan limits for mortgages acquired by the GSEs in 2020. The baseline limits for 2020 will be $510,400 and the high-cost area limit will be $765,600 – this represents an approximate 5 percent increase from the 2019 loan limits. These changes mean that the maximum conforming loan limit will be high in 2020 in all but 43 counties in the country. On December 3, the FHA announced the 2020 county loan limits for single-family mortgages the agency insures and issued a Mortgagee Letter outlining the “2020 Nationwide Forward Mortgage Limits.” FHA sets the loan limits for most counties at 115 percent of the country’s median home price and, for 2020, set the “floor” for low-cost areas at $331,760 (65 percent of the national conforming limit) and the “ceiling” for high-cost areas at $765,600 (150 percent of the national conforming limit) for one-unit properties.

For many Americans, the biggest hurdle in buying a home is the down payment. According to a recent report, 49% of non-homeowners stated that not having enough money for a down payment and closing costs was a major obstacle to purchasing a home. Many people also mistakenly believe lenders require a 20% down payment to qualify for mortgage financing.

Data shows that by using private mortgage insurance (MI), millions of homebuyers with down payments as low as 3% or 5% have been approved for affordable and well-underwritten mortgages.

In the past year alone, MI has helped more than 1.1 million borrowers purchase or refinance a mortgage. Nearly 60% were first-time homebuyers, and more than 40% had annual incomes below $75,000.

How MI works

In addition to the other elements of the mortgage underwriting process — such as verifying employment and determining the borrower’s ability to afford the monthly payment — lenders require borrowers to commit some of their own money before approving their mortgage loan. This is where MI entered the system more than 60 years ago, to bridge the down payment gap and help creditworthy borrowers qualify for a mortgage without large down payments.

Benefits of MI

It helps you buy a home sooner. On average it could take 20 years for a household earning the national median income of $61,372 to save 20%, plus closing costs, for a $262,250 home, the median sales price for a single-family home. MI helps borrowers qualify with as little as 3% down.

It is temporary, leading to lower monthly payments down the road. MI can be cancelled once 20% equity is established, either through payments or home price appreciation. Borrowers typically can cancel MI within the first five to seven years. This is not the case for the vast majority of mortgages insured by the Federal Housing Administration. FHA mortgage insurance premiums stay on the loan for the life of the loan.

It provides several flexible payment options. Your lender can offer several MI product options for MI payment; the most common is paid monthly along with your mortgage until the MI cancels.

MI is a stable, cost-effective way to obtain a low down payment mortgage, and offers distinct benefits to borrowers. It’s been a cornerstone of the U.S. housing market since 1957, providing more than 30 million families with the opportunity to own homes despite financial barriers. If you are considering purchasing a home, it is important to understand your options, including your low down payment options. To learn more, visit LowDownPaymentFacts.org.