USMI joined nearly 60 other organizations in supporting a full Senate vote on the nomination of Pam Patenaude as HUD Deputy Secretary. Click below to read the full coalition letter. Click here to download the letter as a PDF.

Category: Announcements & Statements

Statement: March 2017 FHFA Credit Risk Transfer Progress Report and RFI

The following statement can be attributed to Lindsey Johnson, USMI president and executive director:

“Private mortgage insurance is a 60-year old bedrock of the housing system that for decades has helped low down payment borrowers qualify for mortgage financing—more than 25 million borrowers to date—and has provided critical credit risk protection to the government and taxpayers through numerous housing cycles. MI works and is a reliable form of credit risk protection, as evidenced by the more than $50 billion in claims that mortgage insurers paid to the GSEs through the downturn. As FHFA states in its progress report, private mortgage insurance remains the primary form of credit enhancement used on mortgages sold to the GSEs with loan-to-value ratios over 80 percent, and in the first quarter of 2017 MI covered $48 billion of mortgages the agencies purchased.

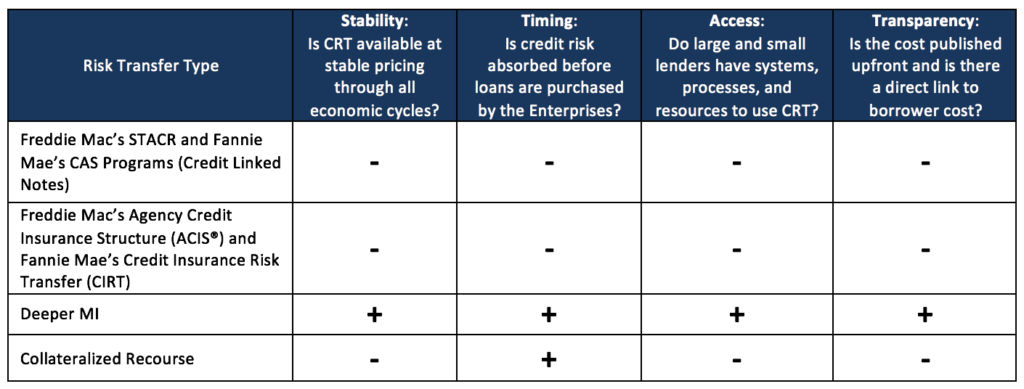

“In the absence of comprehensive GSE reform, FHFA is rightfully exploring options in the credit risk share market through various pilots, and USMI encourages greater balance, transparency, and comparable standards among these options. The cost of credit enhancement has more than doubled for many of the back-end CRT tranches sold, which indicates price volatility continues to be present for these transactions. Our industry remains confident that greater potential benefits can be realized through front-end risk sharing, specifically as outlined in our proposal last year to explore deeper MI coverage, where even more risk is transferred away from the government before it ever touches the GSEs’ balance sheets. The vast majority (more than 97 percent based on risk in force) of CRT transactions to date have been done on the back-end, with the GSEs warehousing credit risk before transferring to the private sector. The GSEs need not carry this level of risk considering there is ample opportunity to increase or at a minimum balance the level of front-end transactions.

“We also encourage equivalent counterparty standards for other CRT transactions, similar to the stringent requirements of mortgage insurers. Doing this will ensure taxpayers are better protected. In the last two years, MIs have materially increased their claims paying ability in both good and bad economic times due to new higher capital standards under the Private Mortgage Insurance Eligibility Requirements (PMIERs). All MIs have met or exceeded PMIERs requirements as of December 31, 2015.”

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

Statement: Requests to Reduce FHA Mortgage Insurance Premiums

![]()

![]()

USMI Statement on Requests to Reduce FHA Mortgage Insurance Premiums

WASHINGTON — Over the last couple of weeks, there have been requests, including from some trade organizations and Democratic members of Congress for the U.S. Department of Housing and Urban Development (HUD) Secretary Ben Carson to reinstate a cut scheduled under the Obama Administration to the Federal Housing Administration (FHA) mortgage insurance premiums (MIP). The following statement can be attributed to Lindsey Johnson, USMI President and Executive Director:

“Helping creditworthy homebuyers qualify for mortgage financing despite a low-down payment is good policy. It is precisely why conventional loans with private mortgage insurance (MI) and the government-backed FHA loans exist. However, reducing FHA premiums is neither necessary nor prudent at this time. Credit remains available for these borrowers in the conventional market, where the risk is backed by private capital, such as MI. A FHA premium reduction will only draw borrowers served in this market over to the FHA, where the risk is 100 percent backed by the government and taxpayers.

“The FHA has and continues to serve an important role in the housing finance system. While the financial health of the FHA has improved since the financial crisis, it is by no means in a position to have the fees it charges for the insurance it provides reduced. Taxpayers are currently exposed to more than $1 trillion in mortgage risk outstanding at the FHA. This would only increase if FHA premiums were reduced.

“Rather than reduce premiums, the FHA should continue to make the needed improvements to its financial health. Policymakers should also work to establish a more coordinated and transparent housing policy that will promote increased access to low down payment lending while at the same time decreasing the federal government’s role in housing, such as reducing or eliminating the GSEs’ loan level price adjustments (LLPAs)—a more effective and prudent means for improving access to mortgage finance credit. Further, we strongly urge against any change to FHA’s life of loan coverage. Unlike private MI, which is cancellable, FHA’s insurance coverage does not go away—thus, taxpayers are on the hook for FHA-insured mortgages for the entire life of the loan.

“Private capital can and should play a leading role in insuring low down payment mortgages so the government and taxpayers are protected from mortgage credit risk. Past FHA commissioners strongly agree with this sentiment. For over 60 years, private MI has been a time-tested and reliable way for Americans to become homeowners sooner—with more than 25 million borrowers helped to date. USMI looks forward to working with all interested parties in Congress and the housing market to ensure we create a housing finance system that protects taxpayers while also promoting homeownership throughout the country.”

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

Statement: Mortgage Bankers Association Report on Reform Recommendations for the GSEs and the Housing Finance System

![]()

![]()

USMI Statement on Mortgage Bankers Association Report on Reform Recommendations for the GSEs and the Housing Finance System

WASHINGTON — Lindsey Johnson, President and Executive Director of the U.S. Mortgage Insurers (USMI), today issued the following statement on the Mortgage Bankers Association report on reform recommendations for Fannie Mae and Freddie Mac (the GSEs) and the housing finance system:

“Today the Mortgage Bankers Association (MBA) released a thoughtful report that outlines its recommendations to reform Fannie Mae and Freddie Mac (the GSEs) and the housing finance system. The report covers many areas and USMI is particularly pleased that MBA recognizes the value of loan-level credit enhancement and the benefit of private mortgage insurance (MI). Importantly the report promotes greater use of front-end credit risk sharing, including through private mortgage insurance. The report also recognizes the important functions of private market participants such as lenders, private mortgage insurers and others, and reinforces that there should be a bright line between the functions of these private market participants in the primary market, and those of secondary market participants. Housing finance is the last, and possibly the greatest, unfinished reform needed from the financial crisis. USMI is pleased to see MBA and other industry, trade and consumer groups provide ideas and proposals for how to reform the housing finance system and we look forward to continuing to work with MBA and others to promote reforms to the housing finance system to put more private capital in front of taxpayer risk and to create a more sustainable housing finance system that works for market participants, taxpayers and consumers.

“For 60 years, MI has provided effective credit risk protection for our nation’s mortgage finance system. This time-tested form of private capital should be the preferred method of absorbing credit loss in front of any government guaranty, helping to minimize taxpayer risk while ensuring mortgage credit remains accessible.”

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

Statement: Senate Confirmation of Ben Carson as HUD Secretary

![]()

USMI Statement on Senate Confirmation of Ben Carson as HUD Secretary

WASHINGTON — Lindsey Johnson, President and Executive Director of the U.S. Mortgage Insurers (USMI), today issued the following statement on the United States Senate confirmation of Ben Carson as Secretary of the Department of Housing and Urban Development (HUD):

“USMI congratulates Secretary Carson on his Senate confirmation to lead the U.S. Department of Housing and Urban Development, a critical federal agency that is a component of the more than $10 trillion U.S. single-family outstanding mortgage debt market. We look forward to collaborating with Secretary Carson and HUD on a comprehensive and coordinated housing policy to promote a stronger and more equitable mortgage finance system that serves American taxpayers, homebuyers and lenders.

“The U.S. mortgage insurance industry welcomes Secretary Carson’s statements that more private capital needs to be brought into the mortgage market and USMI members stand ready to do more, building on the industry’s 60-year history as an effective and time-tested source of credit loss protection. Private MI shields the government and taxpayers from mortgage-related risks in the U.S. housing market that is available during both good and bad housing market cycles.

“In the past six decades, private capital in the form of MI has helped more than 25 million families get into homes; in 2016 alone, MI helped nearly 830,000 families purchase or refinance homes – nearly 50 percent of whom were first-time homebuyers. We look forward to working with Secretary Carson and his team to continue serving American families while also reducing risk to taxpayers and the government.”

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

Statement: FHA Mortgage Insurance Premium Reduction

WASHINGTON —The Federal Housing Administration (FHA) announced today it will reduce its mortgage insurance premiums (MIPs) by 25 basis points. In November 2016, a HUD official stated there would be no additional MIPs cuts following its annual report to Congress on the financial status of its Mutual Mortgage Insurance Fund (MMIF), which showed it had finally reached its required capital levels after nearly a decade of severe stress. The following statement can be attributed to Lindsey Johnson, USMI President and Executive Director:

“While the MMIF is making needed improvements to its financial health, now is the time to establish a more coordinated housing policy to ensure broad access to low down payment lending while reducing the government’s footprint in housing and protecting taxpayers. Arbitrary reductions to the FHA’s MIP is bad policy because it pulls borrowers who would otherwise be served by the conventional Fannie Mae and Freddie Mac market, which is backed by private mortgage insurance for first losses versus the taxpayer. Taxpayers are currently exposed to $1.3 trillion in mortgage risk outstanding at FHA. As a result, and unless Fannie Mae and Freddie Mac make commensurate fee adjustments to reflect the FHA decision, the government will likely assume increased amounts of mortgage credit risk.

“We agree with views of past FHA commissioners who contend private capital should play a leading role in guaranteeing low down payment mortgage credit risk so the government and taxpayer don’t have to. Given the wide availability of MI-backed mortgages, the FHA does not need to undercut private capital. USMI continues to believe that FHA serves a very important role, but it has expanded its footprint dramatically since the financial crisis and should instead remain focused on its core mission of serving underserved borrowers. FHA and the GSEs should be much more coordinated to promote broad sustainable homeownership.

“The last time FHA reduced its premiums in 2015, the move resulted in a high volume of FHA loan refinancing versus new mortgage origination, in essence maintaining the same borrowers and home loans while collecting less in insurance premiums. In other words, the same FHA mortgage credit risk but with less protection. This will result in a less financially resilient FHA and increased risk for taxpayers.”

For the consumer, private MI offers distinct advantages over FHA mortgage insurance. For instance, unlike FHA, private MI can be cancelled once approximately 20 percent equity is achieved either through payment or home price appreciation. This step immediately lowers the monthly mortgage for the homeowner.

Private mortgage insurers, who put their own capital at risk to mitigate mortgage credit risk, provided over $50 billion in credit risk protection since the financial crisis to the GSEs and did not take any taxpayer bailout. The market has been strengthened since the financial crisis as all MIs have all implemented significant new capital requirements, or the Private Mortgage Insurer Eligibility Requirements (PMIERs), which are stress-tested financial and capital requirements established by Fannie Mae, Freddie Mac and the Federal Housing Finance Agency, enhancing MI’s ability to assume mortgage credit risk in the future.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

Statement: FHA’s Annual Report to Congress

![]()

For Immediate Release

Media Contact: Dan Knight

202-777-3544

USMI Statement on FHA’s Annual Report to Congress

WASHINGTON — Today, the Federal Housing Administration (FHA) released its “Annual Report to Congress Regarding the Financial Status of the Mutual Mortgage Insurance Fund (MMIF) Fiscal Year 2016.” The following statement can be attributed to Lindsey Johnson, USMI President and Executive Director:

“Consistent with improvement in the overall mortgage credit market, we welcome the news that FHA’s single-family forward program and the home equity conversion mortgage (HECM) program are combined above the statutory required 2 percent capital ratio. Now that FHA’s single-family fund has climbed its way back, this moment presents an opportunity for the new Administration and lawmakers to consider a coordinated housing policy to ensure broad access to low downpayment lending while reducing the government’s footprint in housing and protecting taxpayers.

“FHA serves an important countercyclical role in the mortgage finance system. Following the financial crisis, FHA’s insured market share grew nearly 300 percent from its pre-crisis market and remains at elevated levels today — and it has taken nearly a decade for the MMIF to recover from serving this countercyclical role. Now that FHA is back to meeting the 2 percent ratio requirement, there is also an opportunity to focus on strengthening FHA’s capital standard, which is dramatically less than what is required of FHA’s private market counterparts, to make the agency more financially resilient going forward. Changes in market conditions, or changes in the very volatile HECM program, could easily push the FHA back into the red.

“Further, this is also the time to refocus the FHA back to its core mission. Fortunately, today there is a healthy low downpayment GSE mortgage market — backed by private mortgage insurance — available to borrowers so FHA no longer needs to play an oversized role in our housing market. Private mortgage insurers put their own capital at risk to mitigate mortgage credit risk, provided over $50 billion in credit risk protection since the financial crisis to the GSEs, and did not take any taxpayer bailout. And this market has been strengthened since the financial crisis as all MIs have all implemented significant new capital requirements, or the Private Mortgage Insurer Eligibility Requirements (PMIERs), which are stress-tested financial and capital requirements established by Fannie Mae, Freddie Mac and the Federal Housing Finance Agency, enhancing MI’s ability to assume mortgage credit risk in the future.

“The MI industry and FHA should serve complementary roles to promote broad and sustainable homeownership. To accomplish this, FHA needs to not only become more financially resilient, in line with the rest of the financial system, but also remain focused on its core mission of serving underserved communities. USMI stands ready to work with the new Administration and Congress to enhance a mortgage finance system that meets the needs of low downpayment borrowers while protecting taxpayers.”

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

Press Release: Comments on FHFA’s Single-Family Credit Risk Transfer Request for Input

For Immediate Release

October 11, 2016

Media Contact: Dan Knight

(202) 777-3547

USMI Submits Comments on FHFA’s Single-Family Credit Risk Transfer Request for Input

Mortgage insurers outline industry’s role in shifting greater risk away from taxpayers in an equitable way for all lenders while expanding access to homeownership

WASHINGTON — U.S. Mortgage Insurers (USMI) submitted comments to the Federal Housing Finance Agency (FHFA) today regarding its Single-Family Credit Risk Transfer (CRT) Request for Input (RFI) and steps to further shield the government sponsored enterprises (GSEs), Fannie Mae and Freddie Mac, as well as American taxpayers, from losses from mortgage-related risks. In its comments, USMI highlights the distinct advantages of front-end CRT done through expanded use of mortgage insurance (MI) that can address existing shortcomings in the GSEs’ credit risk transfer transactions and that can offer substantial benefits for taxpayers, lenders of all sizes, and borrowers.

USMI notes in its comments that “increasing the proportion of front-end CRT in the Enterprises’ CRT strategy will advance four key objectives of a well-functioning housing finance system by ensuring that: (1) a substantial of private capital loss protection is available in bad times as well as good; (2) such private capital absorbs and deepens protection against first losses before the government and taxpayer; (3) all sizes and types of financial institutions have equitable access to CRT; and (4) CRT costs are transparent, thereby enhancing borrower access to affordable mortgage credit.”

“By design, and as evidenced by the more than $50 billion in claims our industry paid during and since the financial crisis, mortgage insurance provides significant first-loss risk protection for the government and taxpayers against losses on low-down payment loans,” said Lindsey Johnson, President and Executive Director of USMI. “As the government explores ways to further reduce mortgage-related risk while also ensuring that Americans continue to have access to affordable home financing, experience shows that mortgage insurance is the answer, particularly when you consider mortgage insurance protection is at work before the risk even reaches the GSEs’ balance sheets.”

While USMI commends FHFA in its comment letter for establishing principles and risks to evaluate front-end CRT structures, which will enable the GSEs and other market participants to analyze the virtues and shortcomings of each form of CRT using an analytical framework, it urges that “the RFI principles should apply to both existing and proposed CRT activities.”

Among other questions, the RFI inquired about benefits of front-end CRT for small lenders. USMI explains in its letter that “small lenders derive optimal benefits from CRT programs that are familiar, have minimal implementation costs, and are based on lender selection among several market participants. Accordingly, MI works very well for small lenders (and deeper-cover MI similarly would work very well for small lenders) because it is already part of their current credit origination processes, is available with transparent pricing, and is available to lenders of all sizes. On the other hand, small lenders have no access to and derive no direct benefits from back-end forms of CRT.”

“In addition to the specific goal of shifting more risk from Fannie Mae and Freddie Mac, and unlike back-end CRT, mortgage insurance plays a direct role in helping families who have good credit but can’t afford large down payments to qualify for a mortgage. For nearly sixty years, mortgage insurers have been leaders in helping millions of Americans, particularly first-time homebuyers, purchase homes in an affordable way,” Johnson said.

Johnson added, “MI is one of the best forms of time-tested credit risk protection for our nation’s mortgage finance system. Mortgage insurers have taken steps to enhance both their claims paying ability—by increased capital and operational standards—and their claims paying process through updated Master Policy Agreements. MI is private capital directly tied to housing. Unlike some other forms of CRT structures, MI is dedicated to a housing finance system in good and bad economic times. By using more MI to provide deeper front-end risk sharing on loans the GSEs guaranty, the GSEs and taxpayers will be at a much more remote risk of losses. Promoting greater front-end risk sharing with MI is a way to help build a strong, stable housing finance system, provide prudent access to affordable mortgage credit, protect taxpayers, and help facilitate the homeownership aspirations for Americans for years to come. ”

USMI’s full comments to FHFA can be found here. A fact sheet on USMI’s comments can be found here.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

Statement: New GSE Credit Insurance Pilot Program

For Immediate Release

September 27, 2016

Media Contact: Dan Knight

(202) 777-3547

USMI Statement on New GSE Credit Insurance Pilot Program

WASHINGTON — Lindsey Johnson, President and Executive Director of U.S. Mortgage Insurers (USMI), said the following today upon the announcement from Freddie Mac about a new pilot program involving mortgage insurers:

“For the past four years, Freddie Mac and Fannie Mae have been experimenting with a number of structures to shift risk away from the GSEs to the private markets. The program announced yesterday for an offering with affiliates of private mortgage insurers is the latest addition to this effort. While it is good to see the GSEs continue to explore ways to reduce the government’s mortgage credit risk exposure, this new offering is effectively a form of credit insurance that Freddie Mac stated builds on its Agency Credit Insurance Structure (ACIS), which is a back-end credit insurance program. While some mortgage insurers are exploring and may ultimately participate in this new credit insurance program, we believe it is important to note that this new structure should not be confused with the deep cover, true mortgage insurance front-end credit risk transfer proposal that we and others have been advocating for.

As the FHFA seeks comment through the RFI process on additional ways to do greater front-end risk sharing, USMI continues to believe that MI is one of the best, time-tested forms of credit risk protection for our nation’s mortgage finance system. We also believe that using more traditional deep cover MI would be a key component to a sound housing policy in the future. Specifically, our industry proposes expanding the current risk protection provided by MI, which today guards up to 35 percent of a loan’s value, as a means of front-end credit risk transfer. This will significantly protect taxpayers while also ensuring borrower access to low down payment mortgages. Having the GSEs increase that protection coverage would put more private capital at risk—precisely what taxpayers and the economy need. Such an entity-based program would make greater use of private capital, put the GSEs and taxpayers in a more remote loss position, allow lenders of all sizes and types to participate, and, importantly, help ensure access to affordable homeownership. As it has been for the past sixty years, private MI can be provided consistently through all economic cycles. We look forward to continuing that dialogue with FHFA, Fannie Mae and Freddie Mac, policymakers, and other stakeholders.”

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

Press Release: USMI Names Patrick Sinks Chairman

For Immediate Release

June 30, 2016

Media Contacts

Laura Capicotto (202) 777-3536 (lcapicotto@clsstrategies.com)

USMI Names Patrick Sinks Chairman

New Leadership Marks a New Chapter for the Mortgage Industry

WASHINGTON — U.S. Mortgage Insurers (USMI) today announced Patrick Sinks will serve as the organization’s new chairman. Sinks is MGIC Investment Corporation’s Chief Executive Officer (CEO) and succeeds USMI Chairman Rohit Gupta, President and CEO of Genworth Mortgage Insurance (MI). Sinks’ appointment marks a new chapter for USMI since its formation in March 2014.

“Restoring stability in the housing economy and setting a long-term course for the mortgage finance system remains a top priority among regulators, lawmakers and industry stakeholders in Washington. I am pleased to serve as USMI chairman as these issues take form given the critical role mortgage insurance plays in facilitating homeownership and protecting taxpayers from government exposure to mortgage risk,” said Sinks.

Sinks previously served as USMI’s Vice Chair. He has served as MGIC’s CEO since March 2015 and brings over three decades of experience in the mortgage insurance industry to USMI’s chairmanship. He began his career with MGIC at its primary subsidiary Mortgage Guaranty Insurance Corporation (MGIC) in 1978 as a member of the accounting team. He served in numerous roles at MGIC, including President and Chief Operating Officer of both MGIC Investment Corporation (MTG) and MGIC prior to being named CEO.

“Patrick’s wealth of experience and proven leadership are tremendous assets to our industry association and I look forward to continuing our work,” said Lindsey Johnson, President and Executive Director of USMI. “I want to also offer my gratitude to Rohit for his dedication to USMI as one of the association’s first chairmen. We are very appreciative of the time and devotion he has given to the organization and value his continued role on our board of directors.”

Bradley M. Shuster, who is the Chairman of the Board and Chief Executive Officer for NMI Holdings, Inc., will take over as Vice Chair for USMI.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

Statement: FHFA Credit Risk Transfer Progress Report and RFI

{kind=link}

For Immediate Release

June 30, 2016

Media Contacts

Laura Capicotto (202) 777-3536 (lcapicotto@clsstrategies.com)

USMI Statement on FHFA Credit Risk Transfer Progress Report and RFI

The Federal Housing Finance Agency (FHFA) has released a Progress Report and Request for Input (RFI) on Single-Family Credit Risk Transfers as a follow-up to the release of the 2016 Scorecard for Fannie Mae, Freddie Mac, and Common Securitization Solutions. U.S. Mortgage Insurers (USMI) welcomes the opportunity to work with FHFA and the government sponsored enterprises (GSEs) on specific steps the GSEs need to take to increase the amount and levels of credit risk transferred. Front-end risk sharing with deeper coverage using private mortgage insurance (MI) will address existing shortcomings in the GSEs’ credit risk transfer efforts and offers substantial benefits for taxpayers and borrowers.

“The MI industry has taken substantial steps to be well positioned to provide more private capital in front of the GSEs’ risk exposure with increased and enhanced capital and reliability standards. MIs are well positioned to do more right now to protect taxpayers and help borrowers,” said Lindsey Johnson, President and Executive Director of USMI. “In the absence of comprehensive reform, we should explore many options in the credit risk share market, with greater balance among them. With three years of largely back-end risk sharing transactions, the potential benefits of front-end risk sharing have not been realized. Unfortunately, the RFI inadequately portrays the role private mortgage insurers (MIs) play in assuming credit risk and the steps MIs have taken to strengthen capital and counterparty standards (click here for MI reliability fact sheet). The RFI discusses many risks but neither provides quantitative analysis of the size and relative importance of those risks, nor proposes or requests proposals for ways to quantify those risks. A strong case exists for expanding mortgage insurance coverage down to 50 percent of the value of the loan and doing it on the front-end, before the risk ever reaches the GSEs’ balance sheets, as part of the next phase of experimentation.”

USMI looks forward to commenting on the following issues as part of the RFI process:

- The need for a balance of methods to offload the mortgage risk concentrated at the GSEs and to enhance housing finance reform possibilities;

- The need for equivalency of standards to be consistently applied to all sources of housing finance and credit enhancement to ensure there is no regulatory arbitrage;

- The need to address pricing and modeling transparency;

- The need to ensure that a broad set of lenders have equitable access to the system; and

- The need to have risk sharing partners that will stay in the market in good times and bad, including during another market downturn when the housing finance system is under stress.

Front-end risk sharing via deeper cover MI transfers credit risk to MIs at the time the loan is originated, which reduces risk before it ever gets to the GSEs and provides real time price transparency so that any savings can be passed on to borrowers.

“While we understand the Enterprises’ consideration of exposure to all counterparties, we think increased private capital by strong counterparties further reduces taxpayer risk and should be encouraged. The MI industry is ready and prepared to do more,” said Johnson. “MIs have raised $9 billion in new capital since the financial crisis, and are well positioned to raise additional capital to meet demand.”

MIs covered roughly $50 billion in claims to the GSEs since conservatorship. Throughout the financial crisis, USMI members never stopped paying claims, never received any bailout money from the Federal government, and continued to write new insurance. In fact, since the crisis, MIs have paid all valid claims, with 96 percent paid in cash and the remainder due over time. MIs have materially increased their claims paying ability in both good and bad economic times due to new higher capital standards under the Private Mortgage Insurance Eligibility Requirements (PMIERs). All MIs have met or exceeded PMIERs requirements as of December 31, 2015.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

Letter: USMI Joins Call for Reduction in Unnecessary GSE Fees on Borrowers

For Immediate Release

June 22, 2016

Media Contacts

Laura Capicotto (202) 777-3536 (lcapicotto@clsstrategies.com)

USMI Joins Call for Reduction in Unnecessary GSE Fees on Borrowers

Consumer and Industry Groups United for Lower LLPAs

(June 22, 2016) – Today, U.S. Mortgage Insurers (USMI) joined 25 financial services and residential real estate trade associations and consumer groups, including the National Association of Realtors, Mortgage Bankers Association, National Association of Home Builders, Credit Union National Association, as well as the Center for Responsible Lending and Consumer Federation of America, in a letter to Federal Housing Finance Agency (FHFA) Director Mel Watt calling for Fannie Mae or Freddie Mac (the government sponsored enterprises, or “GSEs”) to reduce or eliminate loan level price adjustments (LLPAs) charged by the GSEs.

“Housing credit remains too tight and too many qualified borrowers are unable to get access to affordable mortgage credit, in large part because the GSEs are still charging LLPAs eight years after the financial crisis,” said Lindsey Johnson, USMI President and Executive Director. “Low down-payment borrowers are being double charged for the risk being assumed by private mortgage insurance (MI). These additional fees are particularly burdensome for low- and moderate-income and first-time homebuyers. It’s time borrowers get the full benefit of the credit risk transferred away from the GSEs to private capital in the form of MI.”

For a copy of the joint letter, click here.

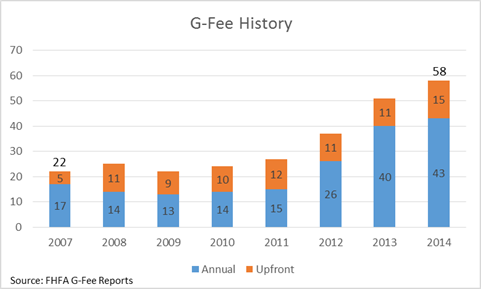

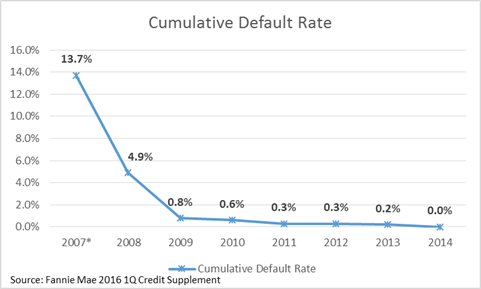

Guaranty fees (or “G-fees”) are fees charged by the GSEs on individual loans they purchase to cover any losses in the event of a default. LLPAs are additional fees first introduced by the GSEs in 2008, during the financial crisis. Borrowers often pay LLPAs in the form of higher mortgage rates. LLPAs continue to be charged nearly eight years later despite significant improvement in the credit quality of GSE-backed loans and strengthened participants in the mortgage finance industry, including lenders and private mortgage insurers. In fact, GSE fees, including LLPAs, are currently two and half times higher than during the mortgage crisis, while the cumulative default rate has decreased from 13.7 percent to near zero.

Low down-payment loans purchased by the GSEs are already covered by MI, which provides the GSEs with substantial protection against first losses on these loans, reducing GSE and taxpayer risk exposure. Mortgage Insurers (MIs) covered more than $50 billion in claims to the GSEs since conservatorship, resulting in substantial savings to taxpayers. MIs have raised $9 billion in new capital since the financial crisis and implemented the Private Mortgage Insurers Eligibility Requirements (PMIERs), a new, rigorous set of capital standards established by the GSEs. The MI industry covers first loss mortgage credit risk ahead of the taxpayers and is ready to do more. Accordingly, FHFA should ensure that the GSEs price credit risk in a manner that is transparent and that reduces arbitrary or unnecessary borrower costs.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.