For Immediate Release

January 14, 2016

Media Contacts

Robert Schwartz 202-207-3665 (rschwartz@rasky.com)

USMI Names MGIC’s Pat Sinks as Vice Chair

Expanded Leadership Team Reflects Growing Industry Presence

(January 14, 2016) U.S. Mortgage Insurers (USMI) today announced that Patrick Sinks, Chief Executive Officer of MGIC, will serve as the organization’s Vice Chair. This new role reflects the growing presence in Washington of the MI industry since the organization’s formation in March, 2014, and builds on the appointment in September, 2015 of Lindsey Johnson as USMI’s President and Executive Director.

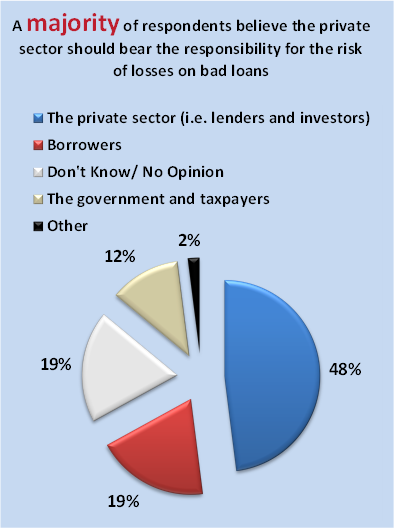

“As policymakers look for more ways to increase the role of private capital to protect taxpayers and expand homeownership, this is a critical time for housing finance policy and the MI industry,” said Sinks. “I look forward to helping USMI be an active voice in Washington on housing finance policy, including reducing taxpayer risks by expanding GSE risk sharing with the proven reliability of MI.”

“Pat brings a wealth of experience and expertise to our mission to inform housing finance policy,” said Rohit Gupta, Chair of USMI and President and CEO of U.S. Mortgage Insurance at Genworth. “We will be actively engaged in many important policy discussions this year, and in Pat’s new capacity as Vice Chair, he will greatly enhance those efforts.”

Patrick Sinks has served as MGIC Investment Corporation’s Chief Executive Officer since March 2015. Pat brings more than three decades of experience in the mortgage insurance industry to USMI, beginning his career with the company at its primary subsidiary Mortgage Guaranty Insurance Corp. (MGIC) in 1978. Pat has served numerous roles at MGIC, including President and Chief Operating Officer of both MGIC Investment Corporation (MTG) and MGIC prior to being named Chief Executive Officer.

###

U.S. Mortgage Insurers (USMI) is dedicated to a housing finance system backed by private capital that enables access to housing finance for borrowers while protecting taxpayers. Mortgage insurance offers an effective way to make mortgage credit available to more people. USMI is ready to help build the future of homeownership. Learn more at www.usmi.org.

Download as PDF