At the midpoint of the first session of the 117th Congress, policymakers are shifting their focus from the COVID-19 recovery to other priorities on the horizon, chiefly infrastructure, and proposed changes to the tax code to fund investments.

Congressional Democrats are rallying around President Biden’s infrastructure proposals, the American Jobs Plan and American Families Plan, which take a holistic view of infrastructure by including traditional infrastructure projects like roads, bridges, railways, and housing as well as non-traditional infrastructure concepts like universal preschool and childcare. Specifically, Democrats are championing housing policies intended to promote equitable communities and give traditionally underserved Americans a stake in those communities. This includes increasing access to homeownership and wealth-building opportunities.

While both parties agree on the need to upgrade the nation’s roads and bridges, and increase broadband access, Republicans and some Democrats have expressed concerns about the expansive scope of the proposed infrastructure projects, along with certain “pay for” provisions.

Housing and Homeownership in America

There is also growing bipartisan attention to the state of housing in the U.S. Even while a record number of first-time homebuyers entered the market in 2020, longstanding concerns about housing access and affordability have been amplified due to rapidly rising home prices. While homeowners have experienced significant equity gains over the past several years, including nearly 11 percent in 2020, strong home price appreciation (HPA) and severely limited supply has locked some borrowers out of the market. This situation has raised concerns from both Republicans and Democrats, as some of the strongest HPA has occurred in rural states.

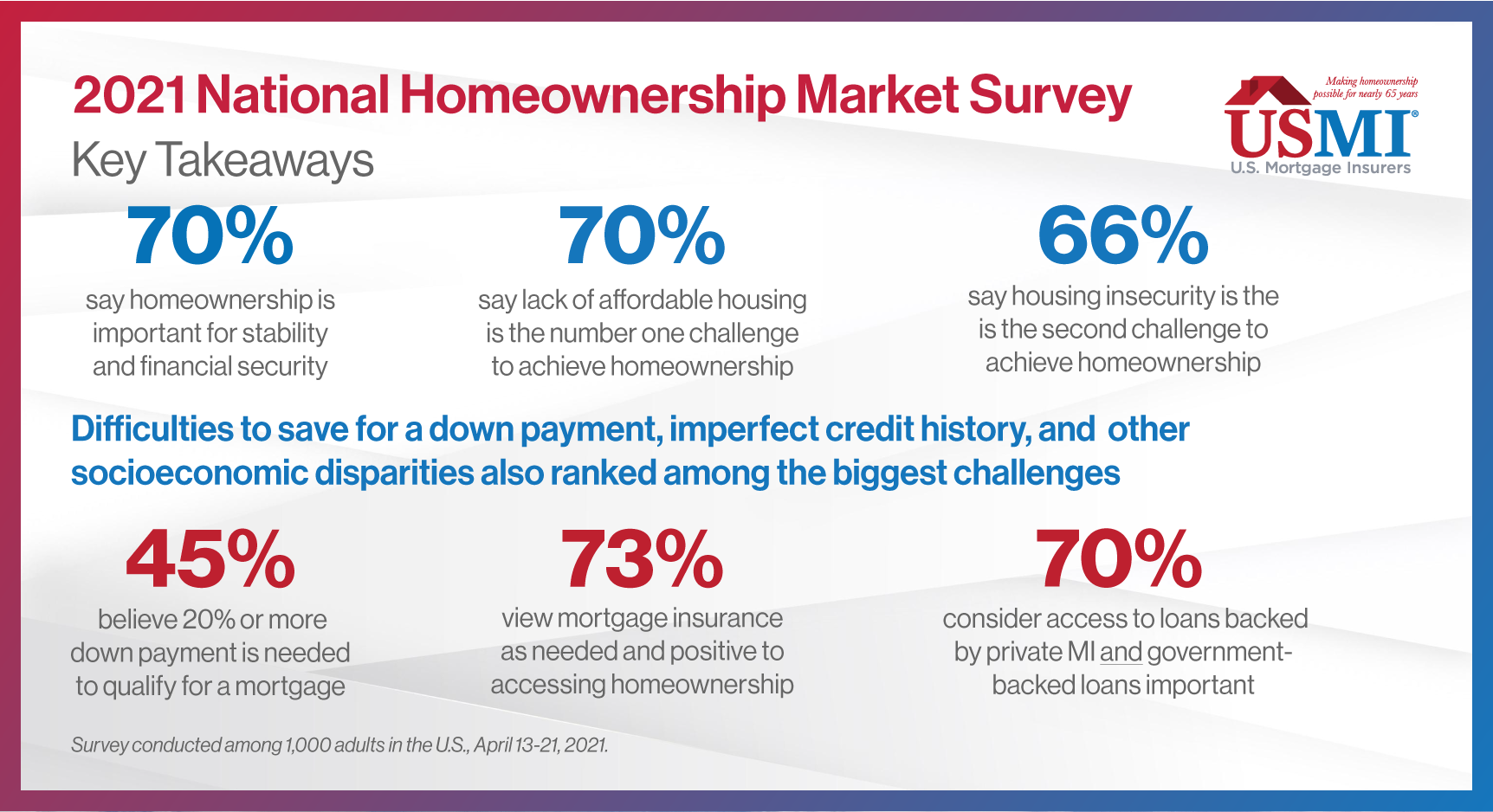

These trends have garnered nationwide attention as the effects of COVID-19 reinforced the importance of stable housing, and the value of homeownership and wealth building among Americans. Simultaneously, Millennials aspire to enter the home purchase market in larger numbers. Today, interest rates are low but as interest in homeownership has risen among first-time buyers, so has its cost. Additionally, in a tight purchase market, affordability—and the 20 percent down payment that 45 percent of Americans believe is required to obtain a mortgage, as reported in USMI’s 2021 National Homeownership Market Survey—is farther out of reach, particularly for those who do not have intergenerational wealth or equity from a previous/current home.

Not only policymakers are eyeing solutions to these challenges. As employers look to attract and retain younger workers, some companies have introduced innovative ways to help employees bridge the down payment gap, or other ways to sustainably increase housing affordability. Redwood Trust has introduced a benefit—the Redwood Employee Home Access Program—that covers the cost of mortgage insurance (MI) for employees. When the program launched in April 2021, Redwood CEO Chris Abate noted that “homeownership is the bedrock of our communities. It builds family wealth and contributes to a sense of inclusion, security, and wellbeing,” and added that Redwood seeks to put homeownership within reach of all its employees. Abate encouraged other employers to offer this benefit, similar to subsidizing health insurance. This type of incentive increases affordability, while also maintaining sustainability, as MI will remain in place and offer protection against the risk of higher loan-to-value loans.

Housing Supply is Critical

In Washington, the conversations around housing access and affordability have recognized the impact of limited housing supply on house prices as a primary driver of around affordability issues. Strong demand over the past twelve months has exacerbated the dearth of supply of such homes, construction of which has lagged pre-2008 levels. Congress has already introduced a variety of bipartisan legislation focused on increasing the supply of housing for low- and middle-income Americans, including the “Yes in My Backyard Act” (HR 3198/S 1614) and the “Housing Supply and Affordability Act” (HR 2126/S 902). Further, President Biden’s proposed budget for fiscal year 2022 contains tax incentives for the construction of low-income housing units for both renters and owner-occupants. Democratic infrastructure proposals aim to further increase supply by dedicating funding for affordable housing development.

Bridging the Down Payment Gap

USMI’s 2021 National Homeownership Market Survey noted that the inability to save for a down payment is among the biggest challenges Americans face when it comes to buying a home. The Biden administration and Congressional Democrats are also aware of this, and how it particularly affects those who lack intergenerational wealth to bridge the down payment gap and first-time homebuyers facing a historically competitive housing market. A number of legislative proposals have been put forward related to down payment assistance (DPA) and supporting homeownership. However, policymakers remain cognizant that the housing market does not need additional demand pushed into the market—the key will be increasing homeownership, particularly among traditionally underserved groups, without further decreasing affordability in the housing market.

First-Time/First-Generation DPA Proposals:

“Housing Is Infrastructure Act of 2021”: Released on April 14, House Financial Services Committee (HFSC) Chairwoman Maxine Waters (D-CA) introduced a bill including legislative text (Section 116) for targeted DPA which also exists as a standalone bill, the “Down Payment Toward Equity Act of 2021”. Chairwoman Waters’ proposal appropriates up to $10 billion for targeted DPA that is limited to first-time, first-generation homebuyers (although those who have lost homes due to foreclosure, deed-in-lieu or short sale also are eligible). Further, income for qualified recipients is limited to 120 percent of area median income (AMI), except in areas with high costs of housing, in which case income limit rises to 180 percent of AMI. Down payment grants are limited to $20,000 (or $25,000 in the case of a qualified homebuyer who is a socially and economically disadvantaged individual). The bill also includes conditional repayment terms for recipients who sell their home within five years.

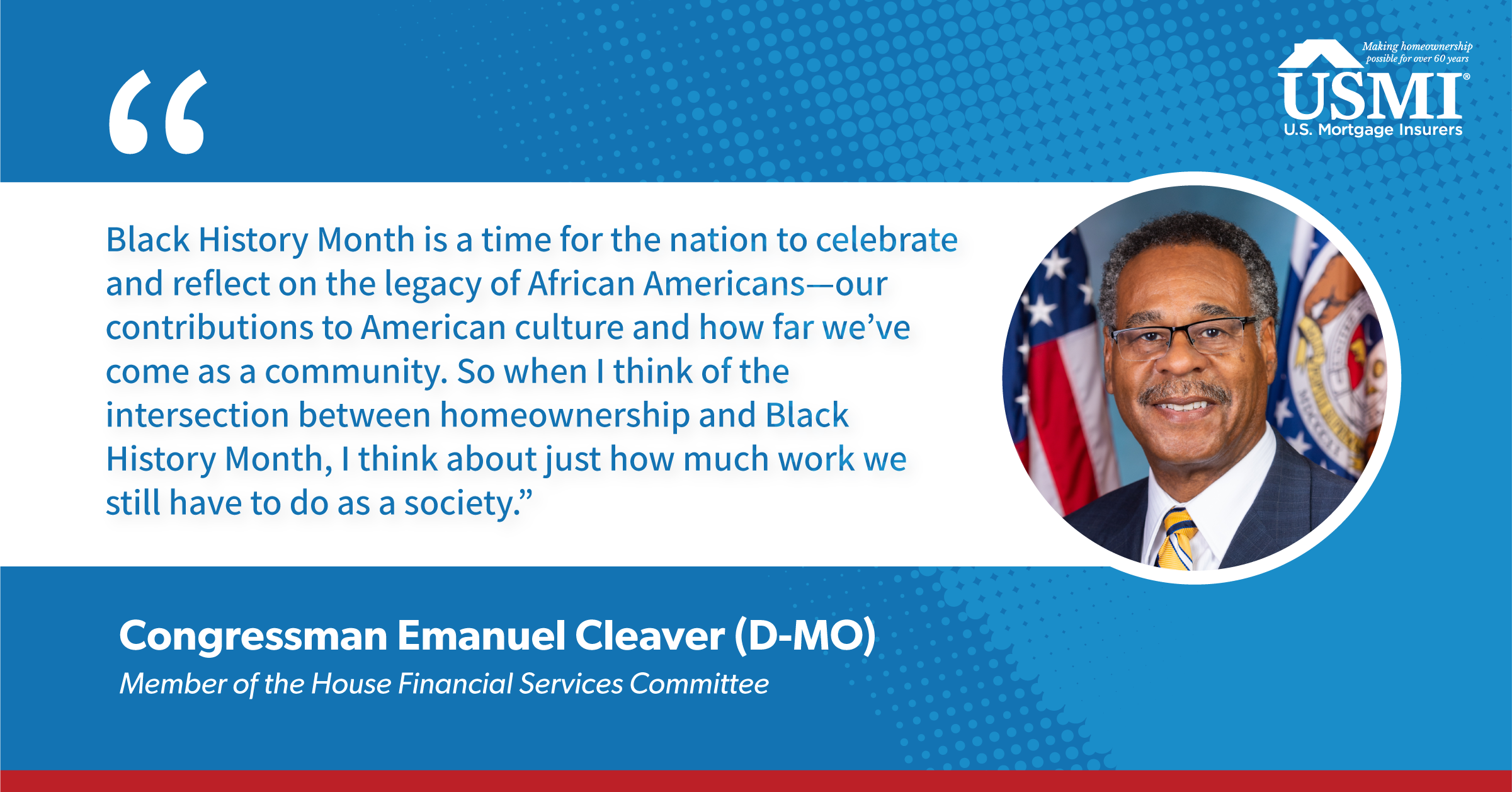

“American Housing and Economic Mobility Act of 2021”: Introduced on April 22 by Rep. Emanuel Cleaver (D-MO) and Sen. Elizabeth Warren (D-MA), the American Housing and Mobility Act aims to increase housing supply and mitigate the historical effects of discriminatory lending. It provides for DPA grants for first-time homebuyers with incomes <120 percent of AMI and who have resided at least four years in a geographic area that was historically denied access to mortgage finance due to official government policy. The bill also proposes investing $445 billion over 10 years in the Housing Trust Fund, and $25 billion over 10 years in the Capital Magnet Fund.

“First-Time Homebuyer Act”: Introduced on April 26 by Reps. Earl Blumenauer (D-OR) and Jimmy Panetta (D-CA), the First-Time Homebuyer Act would provide a tax credit for first-time homebuyers for the lesser of 10 percent of the purchase price of the property acquired or $15,000 for joint tax filers.Assistance would be restricted to homebuyers with incomes ≤160 percent of AMI purchasing homes for ≤110 percent of their area’s median purchase price. This legislation is similar to President Biden’s campaign proposal to provide $15,000 tax credits to homebuyers.

Comparison of DPA Legislation

| Down Payment Toward Equity Act | American Housing and Economic Mobility Act | First-Time Homebuyer Act | |

| Lead Sponsor | Rep. Waters (D-CA) | Rep. Cleaver (D-MO) & Sen. Warren (D-MA) | Rep. Blumenauer (D-OR) |

| Structure | Grant with 5-year occupancy requirement (5-year repayment schedule in the event homeowner sells the property) | Grant | Tax credit with a 4-year recapture period |

| Maximum Assistance | $20k and $25k for homebuyers who are socially and economically disadvantaged individuals | ≤3.5% of the appraised value of the property (or ≤3.5% of maximum principal obligation if the appraised value exceeds the principal obligation amount) | Lower of 10% of the purchase price or $15k (for married tax filers) subject to inflation |

| Targeting | |||

| First-time Homebuyer requirement | Yes and first-generation | Yes and have lived for 4 years prior to enactment in a geographic area historically subject to discrimination or official segregation | Yes |

| Income Restriction | ≤120% of AMI and ≤180% of AMI for properties located in high-cost areas | <120% of AMI | Modified AGI ≤160% of AMI |

| Purchase Price Restriction | N/A | N/A | ≤110% of area median purchase price for full tax credit amount |

| Housing Counselling Required | Yes | Not required | Not required |

Tax Incentives to Support Homeownership:

“American Dream Down Payment Act”: Introduced in February by Reps. Gregory Meeks (D-NY), Joyce Beatty (D-OH), and Al Green (D-TX), the American Dream Down Payment Act would establish qualified down payment savings programs to open tax-advantaged accounts (similar to 529 accounts for educational expenses) to save for a down payment, including closing costs, for the purchase of a principal residence. There is no “first-time homebuyer” requirement for the use of the funds in the account, and the maximum account balance would be $102,080 subject to annual increase based on inflation.

Building Home Equity Among Underserved Borrowers:

In an effort to enable first-generation homeowners to build home equity more rapidly, Sen. Mark Warner (D-VA) has also proposed subsidized 20-year mortgages for first-generation homebuyers. Using a one-time federal subsidy to lower the interest rate, the monthly payments on such a mortgage would be comparable in gross terms to 30-year mortgages for the same property.

More details about these proposals and efforts to increase the housing supply are expected to emerge as Congressional negotiations over infrastructure continue this Summer and Fall.